Foreign Institutional Investors (FIIs) have accelerated their selling in India’s debt markets during April 2026, reflecting rising currency volatility, narrowing yield differentials, and evolving global macroeconomic conditions. The sustained outflows signal a cautious stance among global investors as relative returns from Indian fixed-income instruments become less attractive compared to developed markets.

Sharp Debt Outflows Signal Shift in Global Investor Sentiment

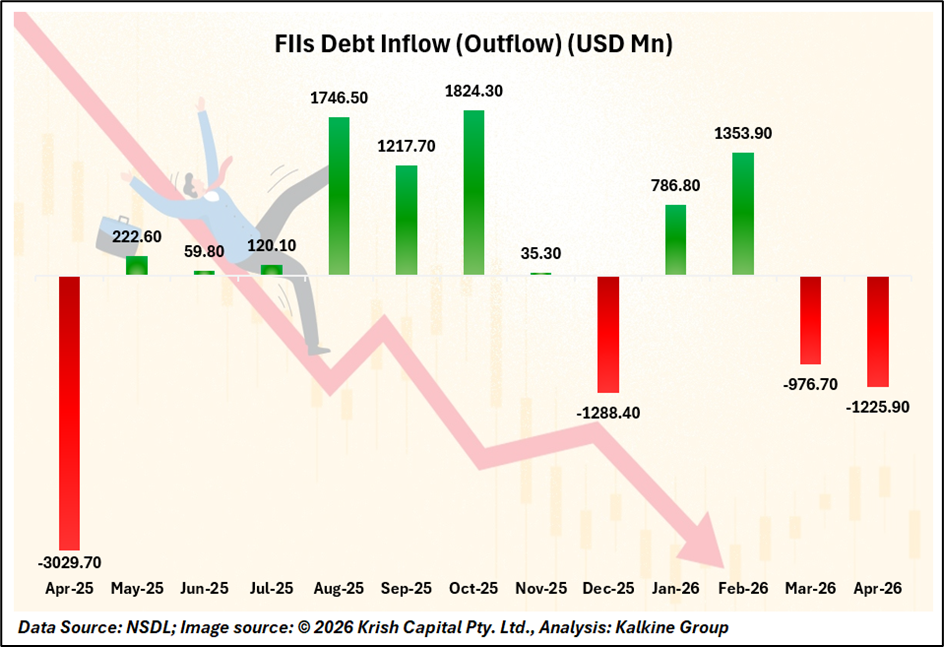

Since the beginning of April 2026, FIIs have offloaded more than USD 1.23 billion worth of Indian debt instruments, placing the month on track to record the steepest debt outflows since April 2025. This follows USD 977 million of debt sales recorded in March 2026, highlighting a continuation of risk-off positioning among foreign investors.

The selling trend reflects growing investor sensitivity toward macroeconomic risks and currency stability. Rising uncertainty surrounding global interest rate trajectories, coupled with currency depreciation concerns, has reduced the attractiveness of Indian debt relative to international alternatives.

Narrowing India–US Yield Differential Dampens Debt Appeal

One of the primary drivers behind the recent outflows is the narrowing yield differential between Indian and US government bonds. As US bond yields remain elevated, the relative premium offered by Indian government securities has diminished.

Historically, India’s higher interest rates have attracted foreign investors seeking yield enhancement. However, persistent global inflation and prolonged higher-for-longer interest rate expectations in advanced economies have altered this equation.

With US Treasury yields remaining firm, foreign investors may perceive limited incremental benefits from holding Indian bonds, particularly after adjusting for currency risks and hedging costs.

Currency Volatility Adds to Investor Caution

The performance outlook for the Indian rupee remains a key factor influencing foreign investment flows. Currency depreciation risks can erode returns for overseas investors, especially when investing in rupee-denominated assets.

Elevated global crude oil prices have contributed to pressure on India’s external balances, as the country remains a significant importer of energy commodities. Higher oil prices can widen the current account deficit and increase demand for foreign currency, potentially weakening the rupee.

In such an environment, FIIs often reduce exposure to debt markets to limit foreign exchange-related risks.

Macro Concerns and Inflation Dynamics Influence Strategy

Global macroeconomic developments continue to shape investor sentiment across emerging markets. Persistent inflation risks, uncertain growth trajectories, and monetary policy tightening cycles in developed economies have created a cautious investment landscape.

Additionally, geopolitical uncertainties and commodity price fluctuations have added another layer of complexity to global capital flows. Investors increasingly prioritize stability and liquidity, particularly in periods of heightened macro volatility.

Implications for Indian Bond Markets

Sustained foreign selling can influence domestic bond yields and liquidity conditions. When FIIs withdraw capital from debt markets, bond prices may experience downward pressure, potentially pushing yields higher.

However, India’s domestic institutional investor base—comprising banks, insurance companies, and mutual funds often plays a stabilizing role during periods of foreign outflows.

Outlook: Volatility Likely to Persist in Near Term

Looking ahead, global monetary policy signals and currency trends will remain critical determinants of foreign investment flows into Indian debt markets. If global yields remain elevated and currency volatility persists, FIIs may continue to adopt a cautious allocation strategy.

On the other hand, stabilization in crude prices, improved currency resilience, and supportive domestic macro fundamentals could help restore investor confidence over time.

Despite the current phase of outflows, India’s long-term debt market outlook remains supported by structural growth drivers, expanding financial markets, and improving integration with global capital flows.