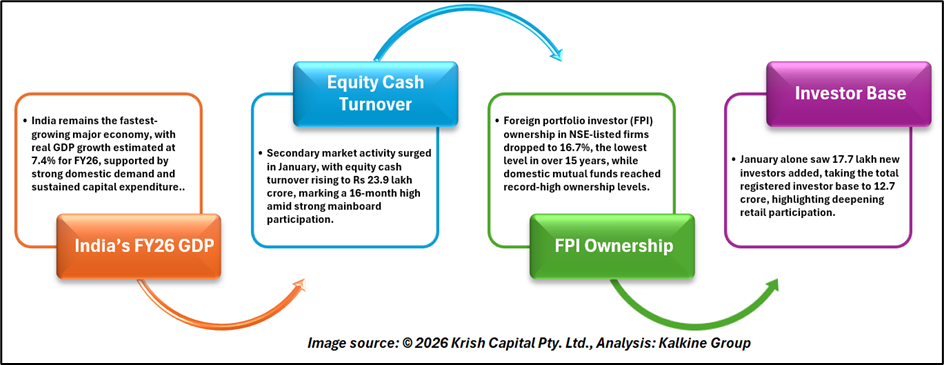

India has entered 2026 with strong macroeconomic stability, reinforcing its position as the fastest-growing major economy. According to the February edition of Market Pulse released by the National Stock Exchange of India Limited, real GDP growth for FY26 is projected at 7.4%, supported by resilient domestic consumption and sustained capital expenditure.

Industrial production has accelerated, while manufacturing and services PMIs remain firmly in expansion territory. GST collections have averaged around Rs 1.9 lakh crore so far in FY26, reflecting steady economic activity. Rural demand indicators, including tractor and two-wheeler sales, remain healthy, even as some urban consumption segments show moderation.

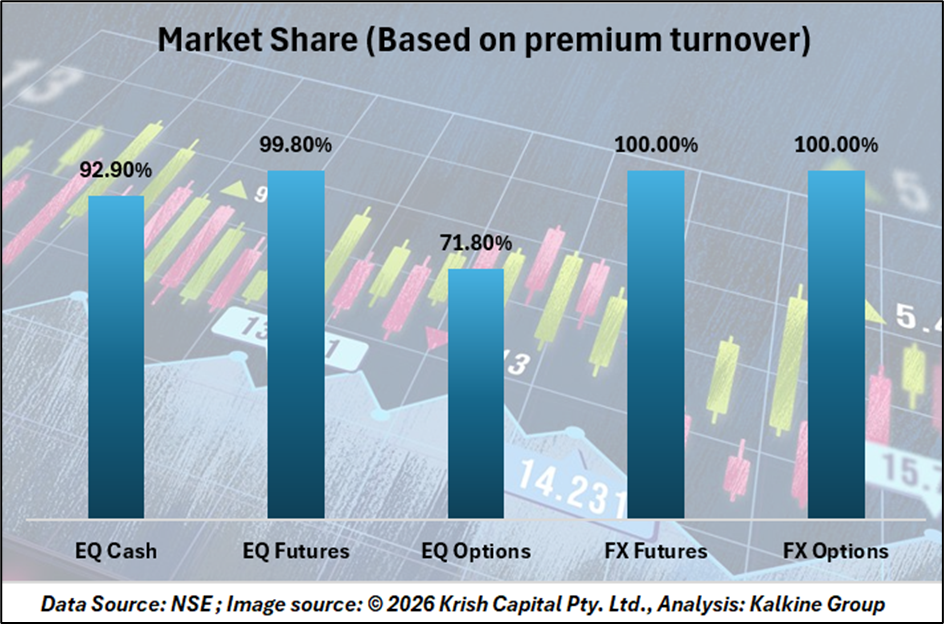

Domestic market share

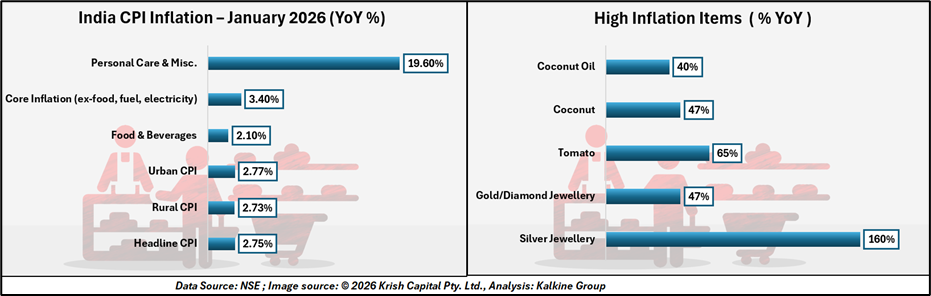

Inflation Comfort Allows Policy Stability

Retail inflation has eased under the revised CPI series, with January inflation at 2.75% year-on-year. Food inflation remains contained, providing additional comfort to policymakers. This has enabled the Reserve Bank of India to maintain the repo rate at 5.25% while retaining a neutral policy stance.

Liquidity conditions remain largely supportive. Although bond yields hardened temporarily following higher borrowing projections, fiscal consolidation remains on track. The fiscal deficit target has been set at 4.3% of GDP for FY27, with capital expenditure sustained at Rs 12.2 lakh crore — signaling consolidation without sacrificing growth investment.

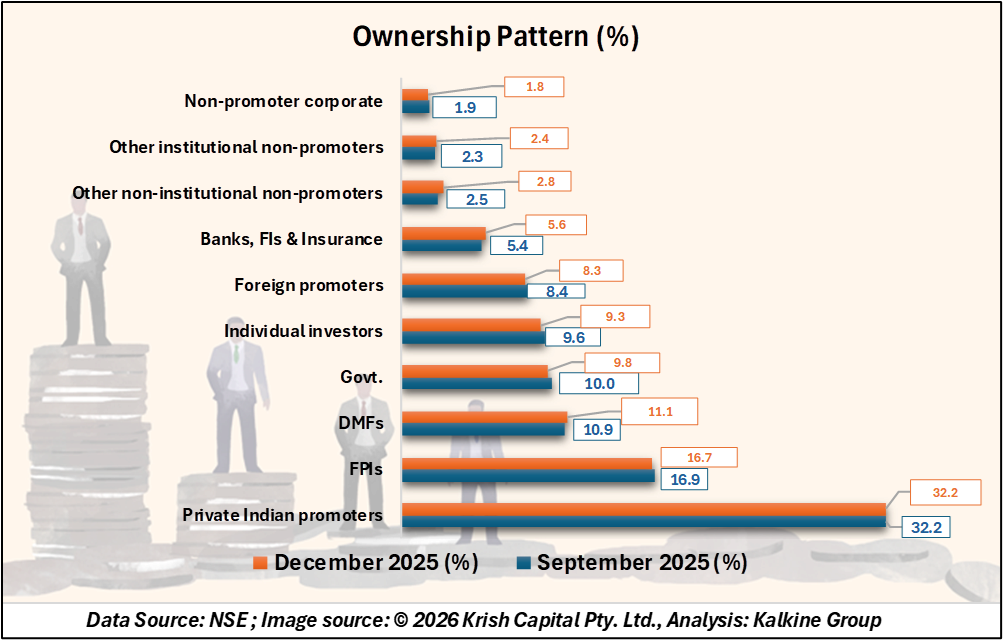

Ownership Shift Redefines Market Structure

FPI ownership in NSE-listed companies has dropped to 16.7%, a 15.5-year low, following record outflows in 2025. In contrast, domestic mutual funds have steadily increased their share, reaching record ownership levels. Direct and indirect household participation in equities continues to expand, with total household equity holdings rising sharply over recent years.

This shift suggests India’s markets are increasingly driven by domestic savings rather than foreign capital flows — a significant long-term stabilizing factor.

Secondary Market Activity Surges

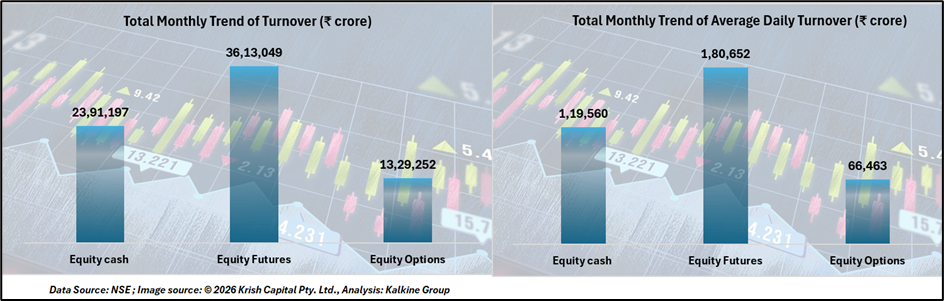

While primary market fundraising moderated in January, secondary market participation strengthened significantly. Equity cash turnover climbed to Rs 23.9 lakh crore, marking a 16-month high. Derivatives activity also intensified, particularly in index options, with Nifty contracts dominating turnover.

Technology-led execution is reshaping trading dynamics. Colocation-based trading continues to expand, while mobile participation remains elevated. Investor growth remains strong, with 17.7 lakh new investors added in January, taking the total registered base to 12.7 crore.

Global Backdrop: Risks Persist

Globally, trade tensions and geopolitical uncertainty remain key risks. The International Monetary Fund projects global growth at 3.3% in 2026, supported by investment in advanced technologies such as artificial intelligence. However, volatility in capital flows and currency movements could continue to influence emerging markets.

India’s foreign exchange reserves, standing at around US$724 billion, provide a solid external buffer amid these uncertainties.

Conclusion: Discipline, Depth and Domestic Strength

India’s 2026 economic narrative reflects consolidation rather than exuberance. Growth remains steady, inflation is contained, fiscal discipline is intact, and capital expenditure continues to drive long-term productivity.

More importantly, the evolving ownership pattern signals structural maturity. With domestic institutions and households playing a larger role, markets appear better positioned to absorb global shocks. While short-term volatility may persist, the underlying fundamentals point toward strengthening internal resilience.