Highlights

- India has sustained robust GDP growth of 6.5–7% while keeping inflation at ~3.34%, within the RBI’s target band.

- Fiscal consolidation from 9% to ~5.5% of GDP has been achieved without compromising growth-oriented spending.

- Policy credibility, demographic advantage, and structural reforms position India as a benchmark emerging market.

- Foreign direct investment is rising, aided by supply chain diversification and initiatives like Production Linked Incentives (PLI).

- Key sectors benefiting from India’s macro strength include infrastructure, manufacturing, consumption, and financials.

India’s macroeconomic trajectory in the post-pandemic era represents one of the most compelling structural growth stories in the global economy. At a time when advanced economies are grappling with the twin challenges of slowing growth and persistent inflation, India has managed to sustain robust economic expansion while maintaining price stability within its policy tolerance band. This rare alignment of growth and stability has positioned India as a benchmark emerging market, attracting increasing attention from global investors seeking resilience in an uncertain macroeconomic environment.

The foundation of India’s macro strength lies in the interplay between growth, inflation, fiscal discipline, and monetary credibility. Unlike many economies where inflation control has come at the expense of growth, India has achieved a balance that reflects both structural advantages and policy effectiveness.

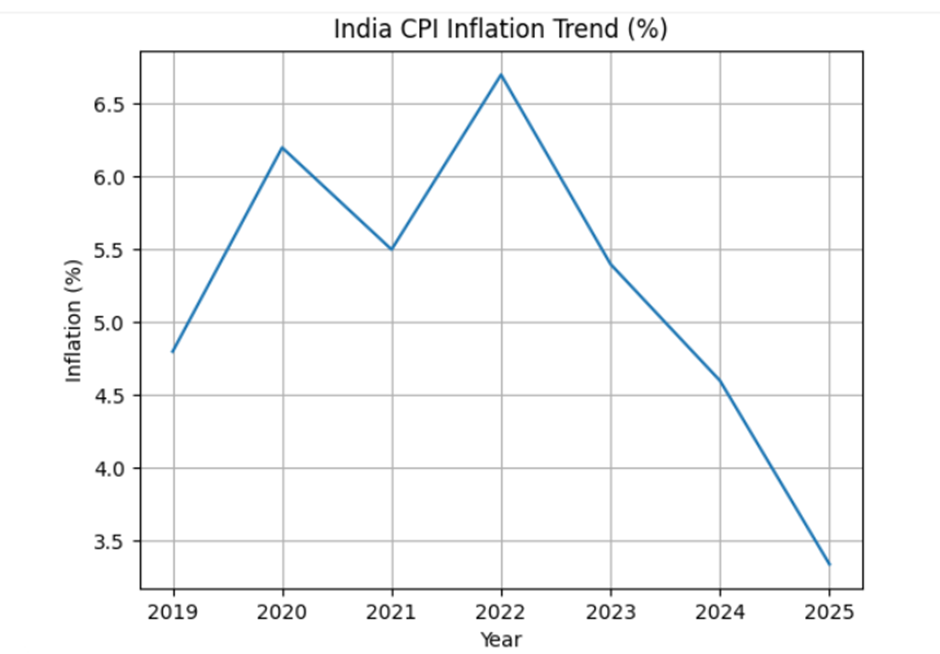

A key starting point is inflation dynamics. India’s consumer price inflation has moderated significantly, declining to approximately 3.34% year-on-year in March 2025. This places inflation comfortably within the Reserve Bank of India’s target band of 2–6%, with a medium-term target of 4%. The trajectory of inflation over recent years highlights both the volatility induced by global shocks and the subsequent stabilisation driven by domestic policy.

The chart demonstrates that while inflation spiked during the pandemic and subsequent commodity shocks, the decline has been relatively smooth compared to global peers. This reflects effective supply-side interventions, particularly in food markets, which constitute a significant portion of India’s consumption basket. Government measures such as buffer stock management, export restrictions on key commodities, and targeted subsidies have played a crucial role in moderating price pressures.

However, the composition of inflation reveals important nuances. Food inflation, while currently subdued, remains highly sensitive to climatic conditions, particularly monsoon variability. Energy prices, driven by global crude oil markets, continue to pose risks through imported inflation. Indeed, imported inflation has emerged as a significant contributor, accounting for over 30% of headline inflation in recent periods. This underscores the importance of external sector stability in maintaining domestic price control.

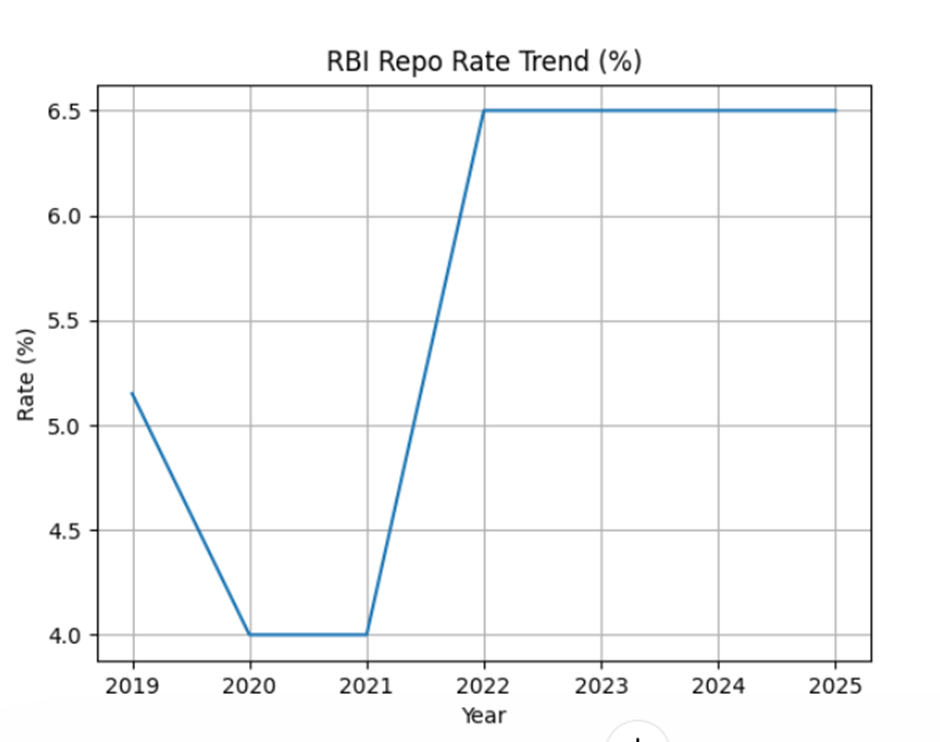

Monetary policy has been central to anchoring inflation expectations. The Reserve Bank of India has adopted a calibrated approach, raising the repo rate from pandemic lows of 4% to approximately 6.5%, where it has remained stable.

This stability reflects a deliberate strategy to balance inflation control with growth support. Unlike more aggressive tightening cycles in advanced economies, the RBI’s approach has been measured, allowing economic activity to recover while ensuring that inflation remains within acceptable bounds. The credibility of this policy framework has been instrumental in maintaining investor confidence and reducing macroeconomic volatility.

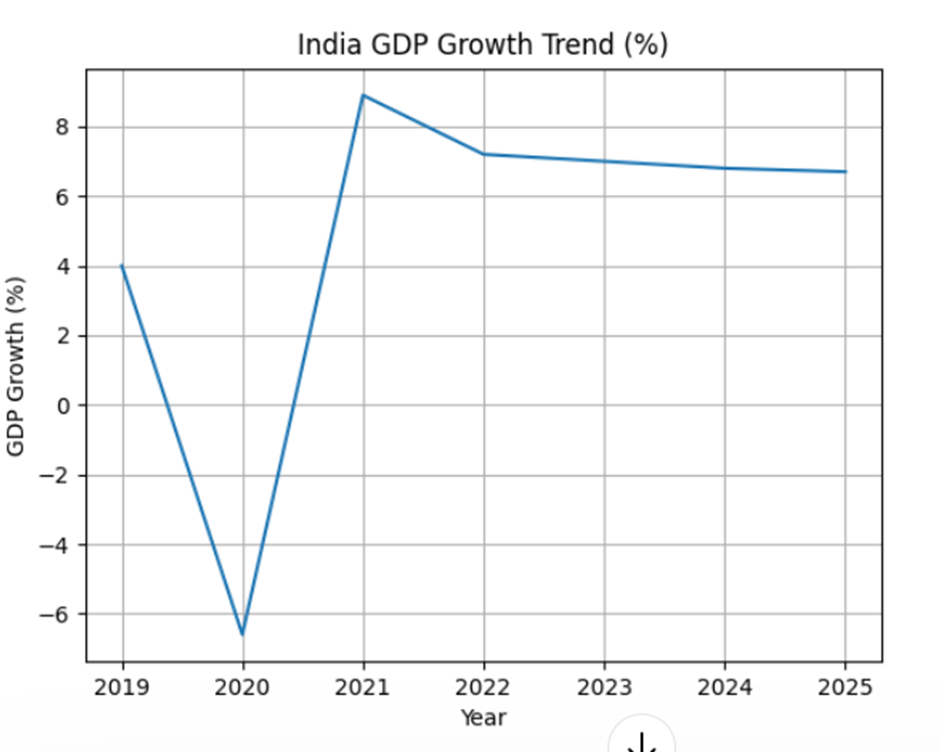

Growth dynamics further reinforce India’s macro positioning. GDP growth has stabilised in the range of 6.5–7%, making India one of the fastest-growing major economies globally.

This growth is broad-based, driven by a combination of domestic consumption, government expenditure, and structural reforms. Private consumption remains the largest contributor to GDP, supported by rising incomes, urbanisation, and improved consumer sentiment. Government capital expenditure, particularly in infrastructure, has provided a strong impetus to growth. Investments in roads, railways, and digital infrastructure have not only created employment but also enhanced productivity, creating a multiplier effect across the economy.

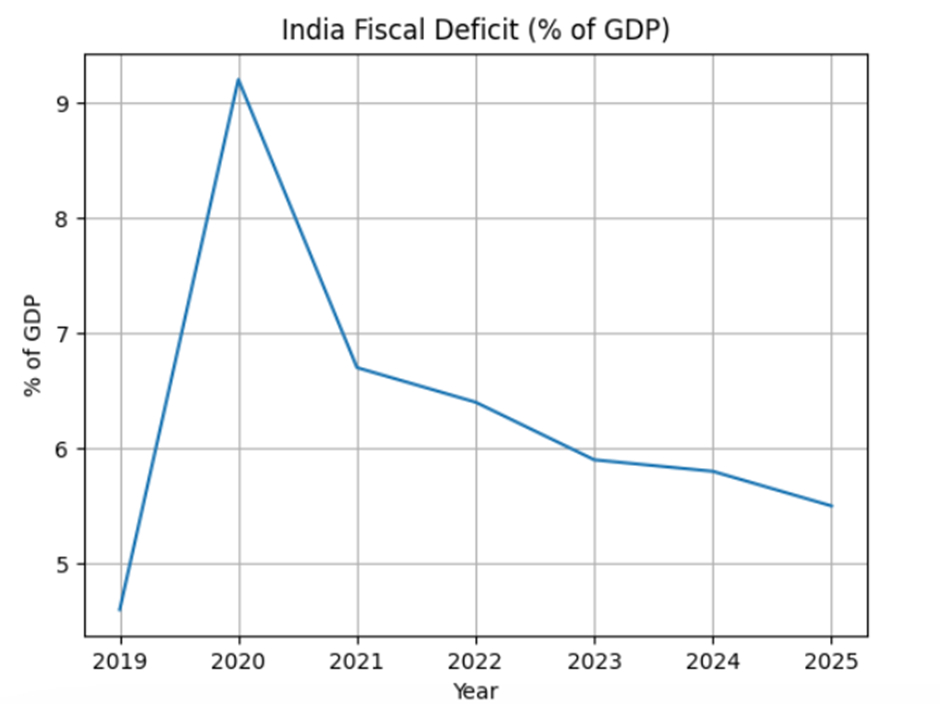

Fiscal policy has played a critical role in sustaining this growth trajectory while maintaining macro stability. India’s fiscal deficit, which expanded significantly during the pandemic, has been gradually consolidated.

The decline in the fiscal deficit from over 9% of GDP in 2020 to approximately 5.5% in 2025 reflects a commitment to fiscal discipline. This consolidation has been achieved without compromising on growth-oriented spending, particularly in infrastructure. The government’s ability to balance fiscal prudence with capital expenditure is a key factor underpinning India’s macro stability.

The external sector adds another dimension to India’s macro narrative. While India remains a net importer of commodities, particularly crude oil, it has benefited from structural shifts in global trade patterns. The reconfiguration of supply chains, driven by geopolitical considerations and the “China+1” strategy, has led to increased foreign direct investment in India’s manufacturing sector. Policy initiatives such as the Production Linked Incentive (PLI) schemes have further strengthened India’s position as a manufacturing hub.

However, external vulnerabilities remain. Currency volatility, driven by global capital flows and interest rate differentials, can impact inflation through imported price pressures. The current account deficit, while manageable, requires continuous monitoring, particularly in the context of fluctuating commodity prices. Nevertheless, India’s foreign exchange reserves provide a buffer against external shocks, enhancing macro resilience.

From a structural perspective, India’s demographic advantage is a key driver of long-term growth. With a young and expanding workforce, India is well-positioned to capitalise on its demographic dividend, in contrast to aging populations in many advanced economies. This demographic profile supports both consumption and labour supply, contributing to sustained economic expansion.

The rapid expansion of the digital economy further enhances productivity and growth potential. Initiatives such as digital payments, financial inclusion programs, and the development of digital infrastructure have transformed the economic landscape, enabling greater efficiency and access to financial services. These developments are not only supporting growth but also enhancing the resilience of the economy to external shocks.

The interaction between macroeconomic fundamentals and financial markets is particularly important in the current environment. India’s combination of strong growth and controlled inflation has significant implications for asset valuations. Sustained GDP growth supports corporate earnings expansion, with consensus estimates suggesting earnings growth in the range of 12–15% annually. This provides a fundamental basis for equity valuations, reducing reliance on liquidity-driven expansion.

At the same time, moderate inflation reduces the risk of aggressive monetary tightening, thereby limiting downside risks to valuation multiples. This creates a favourable environment for equities, particularly in sectors aligned with domestic demand and structural growth drivers.

Sectoral dynamics reflect these macro linkages. Financials benefit from stable interest rates and credit growth, while consumption sectors gain from rising incomes and urbanisation. Infrastructure and capital goods sectors are supported by government expenditure, while manufacturing benefits from supply chain diversification and policy incentives. Conversely, export-oriented sectors may face challenges in the event of a global slowdown, highlighting the importance of sector selection.

Valuation premiums in India’s equity markets are often a point of debate. Compared to other emerging markets, India trades at higher price-to-earnings multiples. However, these premiums are increasingly justified by structural factors, including stronger growth, policy stability, and earnings visibility. Unlike markets driven by speculative capital flows, India’s valuations are supported by fundamentals, making them more sustainable over the long term.

Capital flows further reinforce this dynamic. India has consistently attracted foreign institutional investment, supported by its macro stability and growth prospects. Strong inflows contribute to currency stability and support equity markets, creating a positive feedback loop. Domestic institutional participation has also increased, reducing reliance on foreign capital and enhancing market resilience.

Despite these strengths, risks remain. Global economic slowdown, commodity price volatility, and tightening global financial conditions could impact India’s growth trajectory. Domestic challenges, including infrastructure bottlenecks and regulatory complexities, also need to be addressed to sustain high growth rates. However, the overall macro framework provides a strong foundation for navigating these risks.

In conclusion, India’s macroeconomic environment represents a unique combination of growth, stability, and structural transformation. The ability to maintain inflation within target while sustaining high growth distinguishes India in the global landscape. As structural reforms continue and global supply chains evolve, India is well-positioned to enhance its role as a key driver of global economic growth.

Analyst Insights:

India’s macroeconomic framework reflects a rare convergence of policy credibility, demographic strength, and structural reform momentum. While short-term risks such as commodity volatility and global financial tightening persist, the medium-term outlook remains robust. Equity valuations, while elevated relative to peers, are increasingly supported by earnings growth and macro stability. Investors should focus on sectors aligned with domestic demand, infrastructure expansion, and manufacturing growth, as India continues to transition into a structurally driven, fundamentals-led market.

FAQs

Q1: How has India balanced growth and inflation post-pandemic?

A: Through calibrated monetary policy, targeted supply-side interventions, fiscal prudence, and structural reforms, India has maintained high growth while keeping inflation within 2–6%.

Q2: What structural factors underpin India’s macro resilience?

A: India’s young workforce, digital economy expansion, policy credibility, and supply chain diversification provide long-term growth and stability advantages.

Q3: Which sectors are most poised to benefit from India’s macro trajectory?

A: Infrastructure, manufacturing, consumption-driven industries, and financials are set to benefit from government spending, rising incomes, and policy incentives, while export-dependent sectors face global risks.