India’s bond market witnessed a sharp decline in FY26, breaking a two-year gaining streak as global headwinds outweighed domestic policy support. According to Reuters, Rising geopolitical tensions in the Middle East triggered a surge in crude oil prices, which significantly impacted investor sentiment and led to heavy selling in government bonds.

The yield on the 10-year benchmark bond climbed to around 7.03%, marking its steepest monthly increase in nearly nine years. This rise reflects falling bond prices and growing concerns over inflation and fiscal stability. As oil prices increase, India—being a major crude importer—faces higher import bills, which can widen the current account deficit and push inflation upward.

Macroeconomic Pressure and Currency Weakness

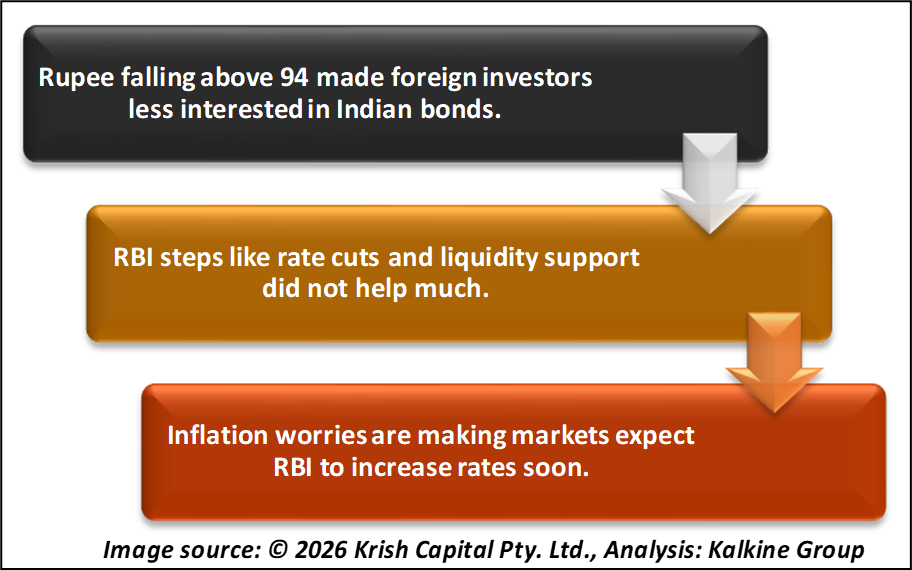

The Indian rupee also came under significant pressure, depreciating past the ₹95 per dollar mark, its worst performance in over a decade. As highlighted by Reuters, This currency weakness has reduced the attractiveness of Indian bonds for foreign investors, leading to a sharp drop in foreign inflows compared to previous years.

At the same time, markets are increasingly worried that inflationary pressures could force the Reserve Bank of India to shift toward a tighter monetary policy stance sooner than expected. This expectation has further pushed bond yields higher.

Despite the RBI’s aggressive measures—including a 100 basis point rate cut, liquidity injections, and open market operations—the impact on bond markets has been limited. The central bank’s shift in stance from “accommodative” to “neutral” has also signaled caution, reducing optimism among investors.

Policy Outlook and Market Sentiment

The Reuters report also noted that the RBI infused massive liquidity into the system during FY26, but bond markets remained under pressure due to persistent external risks. Investors are now closely watching upcoming policy decisions, with expectations that the rate-cut cycle may have ended.

Market participants believe that if global uncertainties continue and oil prices remain elevated, inflation risks could intensify, limiting the RBI’s ability to support growth through further easing.

Technical summary

India’s 10-year government bond yield is trading near 6.96%, maintaining a clear upward trend above the 51-day moving average at 6.70%. Price action shows higher highs and higher lows, indicating sustained bearishness in bonds (rising yields). The recent breakout above the 6.85–6.90% zone signals continuation momentum toward the 7.00% mark.

RSI at 76.67 suggests overbought conditions, indicating a potential short-term pause or mild pullback. Immediate support is seen near 6.85% and 6.70%, while resistance is positioned around 7.00%. The overall structure remains upward biased unless yields fall below the moving average.

Conclusion

As per Reuters, India’s bond market is currently facing a challenging phase driven by global geopolitical tensions, rising oil prices, and currency weakness. While the Reserve Bank of India has taken strong steps to support liquidity and growth, external factors are dominating market direction. The decline in foreign investment and rising inflation concerns suggest a cautious outlook. If geopolitical risks persist, bond yields may remain elevated, keeping pressure on prices in the near term.