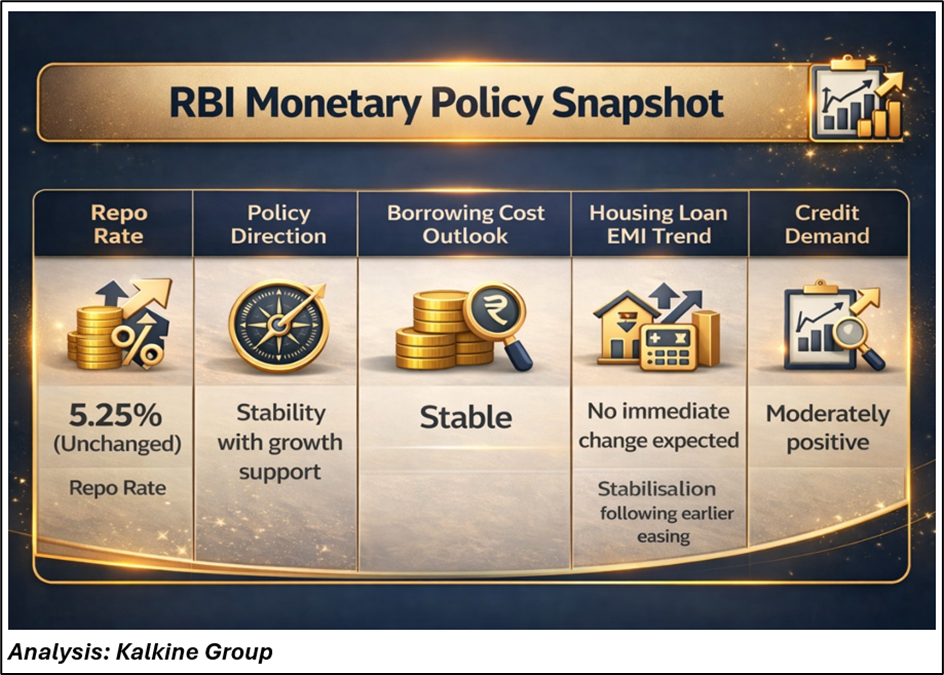

The Reserve Bank of India (RBI) has maintained the repo rate at 5.25% in its April 2026 Monetary Policy Committee (MPC) review, signalling a calibrated pause following earlier rate reductions. The decision underscores the central bank’s intent to balance inflation management with sustained economic growth.

For home loan borrowers, the policy continuity implies stable equated monthly instalments (EMIs), enabling them to retain the benefits of prior rate cuts. From an investment perspective, the rate hold strengthens visibility across banks, housing finance companies (HFCs), and real estate-linked sectors, which remain sensitive to interest rate movements.

Policy Overview: Key Highlights

The RBI’s decision suggests confidence in the evolving inflation trajectory while maintaining sufficient policy flexibility to respond to global uncertainties.

Implications for Home Loan Borrowers

- Stable EMIs Preserve Financial Planning Certainty- Borrowers with floating-rate home loans linked to repo-based benchmarks are unlikely to witness any change in lending rates in the near term. The absence of rate hikes preserves affordability metrics and supports household financial planning.

- Affordability Metrics Remain Supportive- Stable interest rates improve affordability thresholds across urban housing markets, particularly in mid-income and affordable housing segments. This environment supports both first-time homebuyers and borrowers seeking loan refinancing or tenure optimisation.

- Strategic Borrower Considerations

- Partial loan prepayments to reduce outstanding principal

- Tenure optimisation to lower lifetime interest burden

- Balance transfer opportunities where differential rates exist

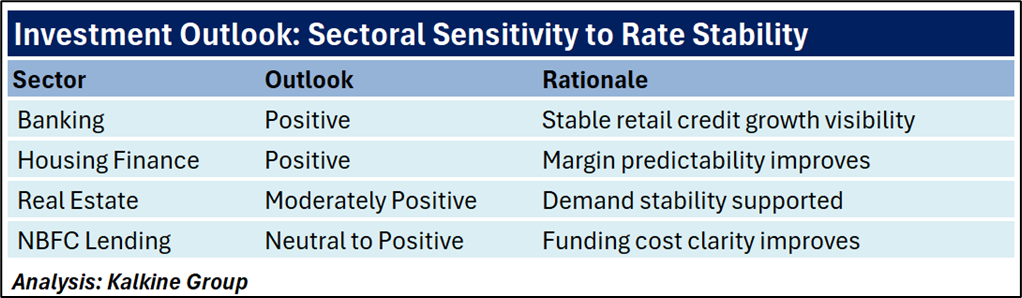

Transmission to Banking and Housing Finance Sector

Interest rate stability provides operational clarity for lenders by reducing volatility in borrowing costs and improving asset-liability management efficiency.

Stable lending conditions typically translate into:

- Improved loan book predictability

- Sustained retail credit growth

- Stable net interest margins

- Reduced borrower stress levels

Mortgage lending continues to represent a substantial portion of retail credit portfolios, making policy direction a critical determinant of sector profitability.

Listed Banking Stocks with Mortgage Exposure

- HDFC Bank Ltd. (NSE:HDFCBANK)

- State Bank of India (NSE:SBIN)

- ICICI Bank Ltd. (NSE:ICICIBANK)

- Axis Bank Ltd. (NSE:AXISBANK)

Housing Finance Companies: Margin Visibility Improves

Housing finance companies are inherently sensitive to interest rate cycles due to their concentrated exposure to mortgage lending.

Key Housing Finance Stocks in Focus

- LIC Housing Finance Ltd. (NSE:ICHSGFIN)

- PNB Housing Finance Ltd. (NSE:PNBHOUSING)

- Aavas Financiers Ltd. (NSE:AAVAS)

- Can Fin Homes Ltd. (NSE:CANFINHOME)

The current policy stability enhances funding cost predictability, supporting margin stability and enabling consistent credit growth strategies.

Real Estate Sector: Demand Outlook Remains Supportive

Housing demand remains closely aligned with interest rate cycles. Stable borrowing costs typically strengthen buyer confidence and support booking momentum across residential projects.

Real Estate Stocks Likely to Benefit

- DLF Ltd. (NSE:DLF)

- Godrej Properties Ltd. (NSE:GODREJPROP)

- Oberoi Realty Ltd. (NSE:OBEROIRLTY)

- Lodha Developers Ltd. (NSE:LODHA)

Stable mortgage affordability enhances residential demand visibility, particularly in urban housing markets where financing availability is a key demand driver.

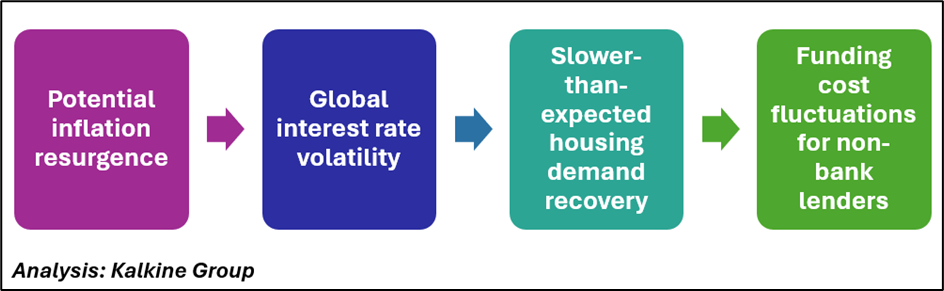

Macroeconomic Outlook

The RBI’s decision to hold rates indicates a cautious yet supportive policy stance amid evolving global and domestic conditions.

Key macroeconomic variables influencing future policy direction include:

- Inflation trajectory across food and fuel components

- Global monetary policy trends

- Domestic growth momentum

- Liquidity dynamics within the financial system

Current signals indicate a transition into a policy stabilisation phase, with gradual adjustments likely rather than abrupt tightening cycles.

Key Risks to Monitor

Strategic Takeaways

Conclusion

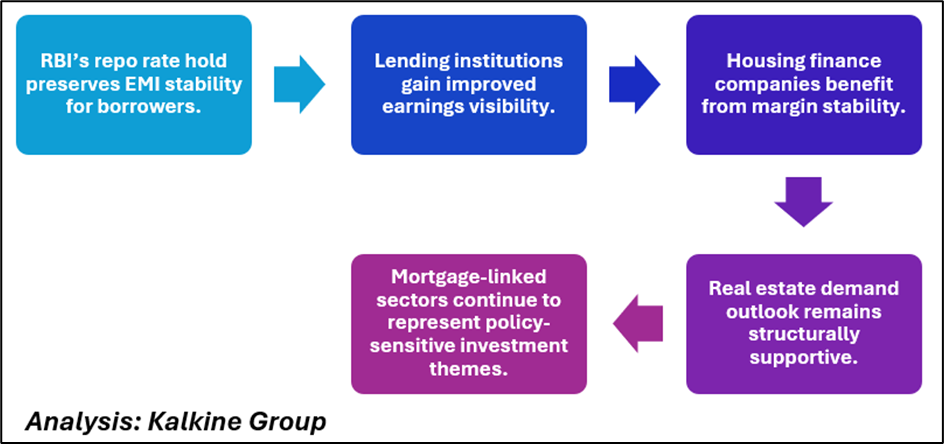

The RBI’s decision to maintain the repo rate at 5.25% marks a continuation of its calibrated policy approach aimed at sustaining growth while managing inflation risks. Stable borrowing costs reinforce affordability conditions across the housing ecosystem and provide operational clarity for lenders.

From an investment standpoint, the stabilisation phase supports earnings visibility across banks, housing finance companies, and real estate developers, positioning mortgage-linked sectors as important beneficiaries of India’s evolving monetary policy cycle.