A government-scheme-driven EPC company with a near-monopoly position in solar agricultural pumps, 340% three-year profit CAGR, and 74% ROCE trades at less than 10x earnings while its construction sector peers command 18–46x. The case for undervaluation is compelling — but the risks are real and specific.

In the universe of Indian small-cap stocks, genuine undervaluation — the condition where a business of demonstrable quality trades at a significant discount to its intrinsic worth — is rare. Most cheap stocks are cheap for reasons that justify their price: cyclical earnings, poor governance, structural competitive disadvantage, or balance sheet fragility. Finding a business that is cheap despite strong fundamentals, accelerating earnings, and a structural demand tailwind requires looking in places the market has not yet fully examined.

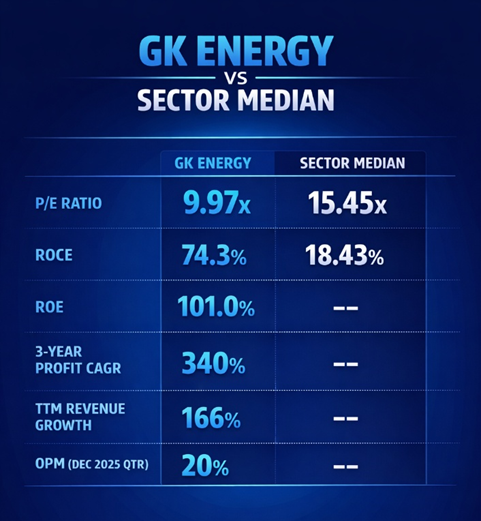

GK Energy Limited (NSE: GKENERGY) may be precisely such a stock. On 2 April 2026, it trades at ₹91.40 — barely off its 52-week low of ₹87.70 and 62% below its 52-week high of ₹240 — at a price-to-earnings ratio of just 9.97x. Against a backdrop of 101% return on equity, 74.3% return on capital employed, a 3-year profit CAGR of 340%, and TTM revenue of ₹1,466 Cr growing at 166%, this valuation demands serious examination.

The central question this article addresses is direct: why is GK Energy trading at less than 10x earnings, and does the answer reveal undervaluation opportunity or a fundamentally justified discount?

What GK Energy Does: The PM-KUSUM Monopoly Position

Incorporated in 2008 and headquartered in Maharashtra, GK Energy Limited is among India's leading EPC (Engineering, Procurement and Construction) players for solar-powered agricultural water pump systems under Component B of the PM-KUSUM scheme — the Government of India's flagship programme to solarise agricultural pumps across the country. The company has installed over 1,00,000 solar pumps across India to date — a milestone that establishes it as a genuine scaled operator in its niche.

The strategic positioning is remarkable in its specificity. GK Energy is empanelled with the Ministry of New and Renewable Energy (MNRE) in Maharashtra, Haryana, Rajasthan, Uttar Pradesh, and Madhya Pradesh — five states that together account for approximately 82% of the total sanctioned pump volume under PM-KUSUM. This is not merely market presence — it is a regulatory moat. Empanelment with MNRE is a qualification-based process that creates a meaningful barrier to entry for new competitors. Companies not on the empanelled list cannot bid for PM-KUSUM work in these states.

Beyond the central PM-KUSUM scheme, GK Energy participates in state-level programmes: Maharashtra's MTSKPY, Madhya Pradesh's PMKMSY, and Chhattisgarh's SSY — further diversifying its government scheme exposure and reducing dependence on any single programme.

The business model is straightforward: GK Energy receives government-backed contracts to supply and install solar pump systems for farmers. The government subsidises 60–70% of the pump cost, with farmers contributing the balance. GK Energy earns EPC margins on the full project value — a model that combines government-backed revenue certainty with the execution risk of a construction business.

The Valuation Anomaly: 9.97x P/E Against 101% ROE

The starting point for any undervaluation analysis is the relationship between the price being paid and the returns the business generates. In GK Energy's case, this relationship is extraordinary — and extraordinarily anomalous.

Chart 1: The Core Valuation Paradox

Data Source: REFINITIV, Analysis: Kalkine Group

──────────────────────────────────────────────────────

The paradox is stark. GK Energy trades at a 35% discount to the sector median P/E of 15.45x — despite delivering ROCE of 74.3% against a sector median of 18.43%, and ROE of 101% that is simply without peer in its comparison group. A business generating four times the sector median return on capital is being valued at a 35% discount to that median. This is the definition of a valuation anomaly that demands explanation.

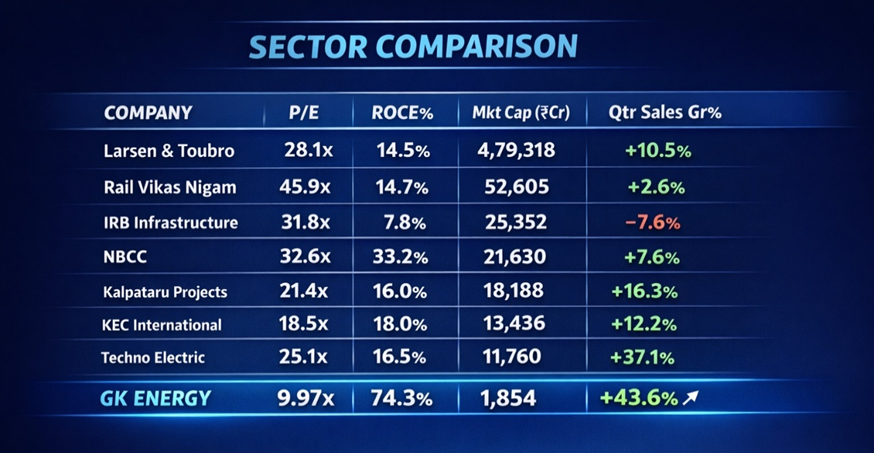

Chart 2: Peer Valuation Comparison

Data Source: REFINITIV, Analysis: Kalkine Group

The peer table makes the undervaluation case visually undeniable. Every peer in the construction and EPC sector trades between 18x and 46x earnings. Rail Vikas Nigam — a government construction company with 14.7% ROCE and just 2.6% quarterly revenue growth — trades at 45.9x. IRB Infrastructure — delivering negative quarterly revenue growth of 7.6% and ROCE of just 7.8% — trades at 31.8x. GK Energy, with the highest ROCE in the group at 74.3%, the strongest quarterly revenue growth at 43.6%, and a 3-year profit CAGR of 340%, trades at 9.97x. The market is awarding the worst-performing companies in the sector the highest multiples, and the best-performing company the lowest.

The Financial Performance: Numbers That Justify Re-Rating

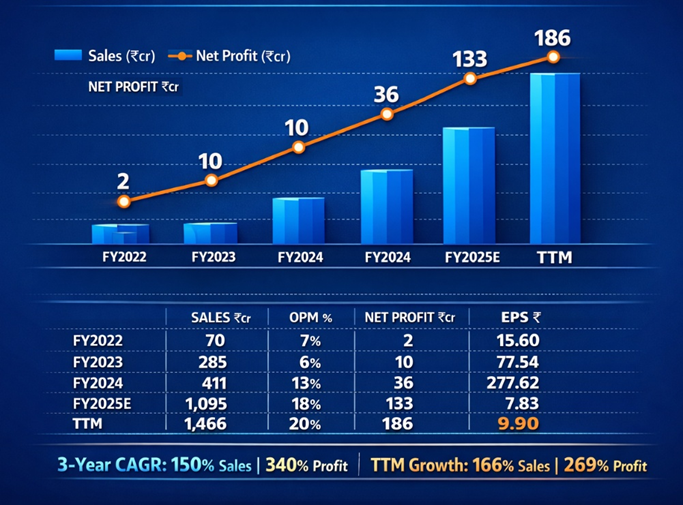

Annual Revenue and Profit Trajectory

Data Source: REFINITIV, Analysis: Kalkine Group

──────────────────────────────────────────────────────────

*Pre-IPO EPS figures reflect different share capital base

The revenue trajectory from ₹70 Cr (FY2022) to ₹1,466 Cr TTM — a 21-fold increase in three years — is one of the most dramatic growth curves in Indian small-cap history. This is not financial engineering or acquisition-driven growth. It is organic volume expansion driven by government scheme execution: more empanelled states, more pump installations, larger order book.

Critically, this growth has been accompanied by expanding margins — not the margin compression that typically accompanies rapid scaling in EPC businesses. Operating profit margin has expanded from 7% (FY2022) to 20% (Q3 FY2026) — a 1,300 basis point improvement as operating leverage and procurement efficiencies have amplified revenue growth into profit growth.

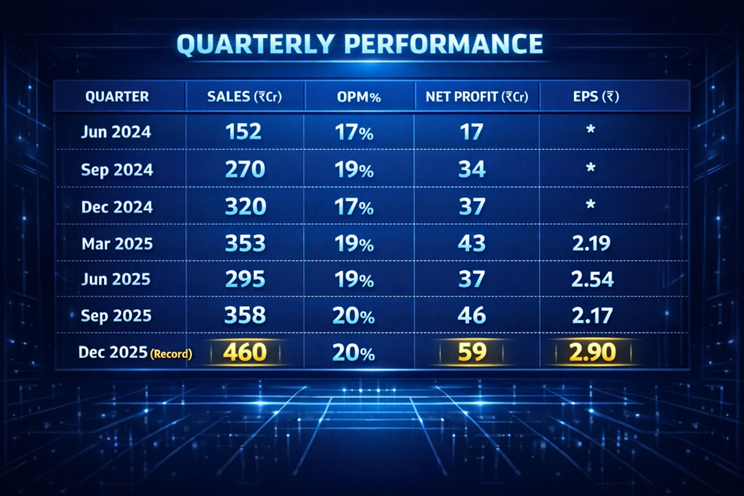

Quarterly Performance — Consistent Acceleration

Data Source: REFINITIV, Analysis: Kalkine Group

────────────────────────────────────────────────────────────

*Pre-IPO periods — share capital different

The December 2025 quarter — revenue ₹460 Cr, net profit ₹59 Cr, OPM 20% — is a record on every metric. Year-on-year quarterly profit growth of 57.72% and revenue growth of 43.64% confirm the business is not merely large but still accelerating. The margin consistency at 19–20% across the last four quarters confirms this is not a one-quarter phenomenon — it is a structural margin level.

At TTM EPS of ₹9.90 and a share price of ₹91.40, the stock trades at 9.23x TTM earnings. For a business growing profits at 269% TTM and 340% over three years, this is a PEG ratio of approximately 0.03 — one of the lowest PEG ratios available anywhere in Indian small-cap equities.

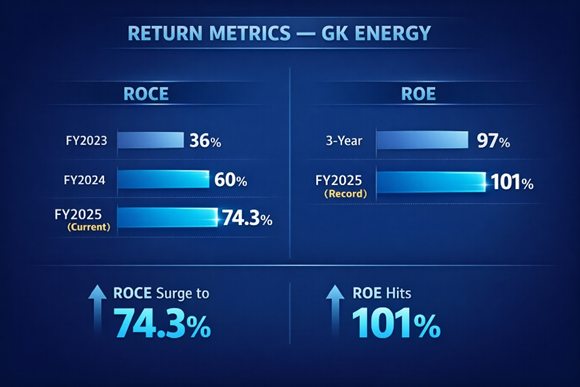

Return on Capital: Best in Sector by a Wide Margin

Data Source: REFINITIV, Analysis: Kalkine Group

A ROCE of 74.3% means GK Energy generates ₹74.30 of operating profit for every ₹100 of capital employed in the business. This is exceptional by any standard — globally, businesses sustaining ROCE above 30% for multiple years are considered elite capital allocators. GK Energy's 74.3% reflects a business model with very low fixed asset intensity (fixed assets of just ₹85 Cr against total assets of ₹1,423 Cr as of September 2025 — just 6% of the asset base) and rapid receivables conversion as government scheme payments are processed.

ROE of 101% — earning more in annual profit than the entire equity book value — is a figure associated with India's highest-quality consumer franchises and financial businesses. In an EPC construction company, it is almost without precedent and reflects the extraordinary returns available from a government-backed scheme business with low fixed capital requirements and expanding margins.

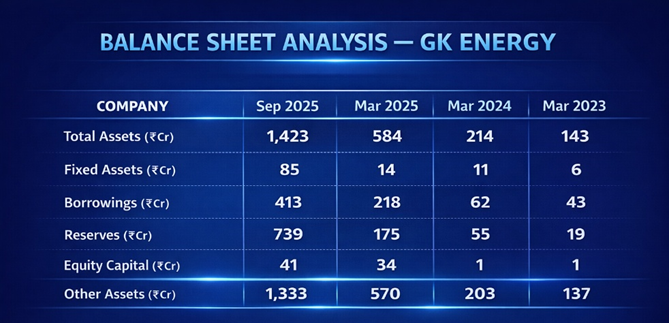

Balance Sheet: Rapid Expansion, Manageable Risk

Data Source: REFINITIV, Analysis: Kalkine Group

The balance sheet tells the story of a business in rapid, capital-hungry expansion. Total assets have grown from ₹143 Cr (FY2023) to ₹1,423 Cr (September 2025) — a tenfold increase in two and a half years. This expansion has been funded by a combination of equity (IPO proceeds reflected in the equity capital jump from ₹1 Cr to ₹34 Cr in FY2025 and ₹41 Cr by September 2025) and debt (borrowings rising from ₹43 Cr to ₹413 Cr).

The borrowings of ₹413 Cr warrant contextualisation. Against reserves of ₹739 Cr — themselves largely the product of retained earnings from the IPO and profit accumulation — the net equity position is strong. The debt is funding working capital for government contracts rather than fixed asset acquisition, which is appropriate for an asset-light EPC model. However, the pace of debt growth — from ₹62 Cr to ₹413 Cr in 18 months — is the primary balance sheet risk and the most likely reason institutional investors have been cautious.

The Cash Flow Reality: The Key Bear Case

This is the most important aspect in the entire GK Energy financial profile — and the most honest explanation for why the stock trades at 9.97x despite exceptional profitability metrics.

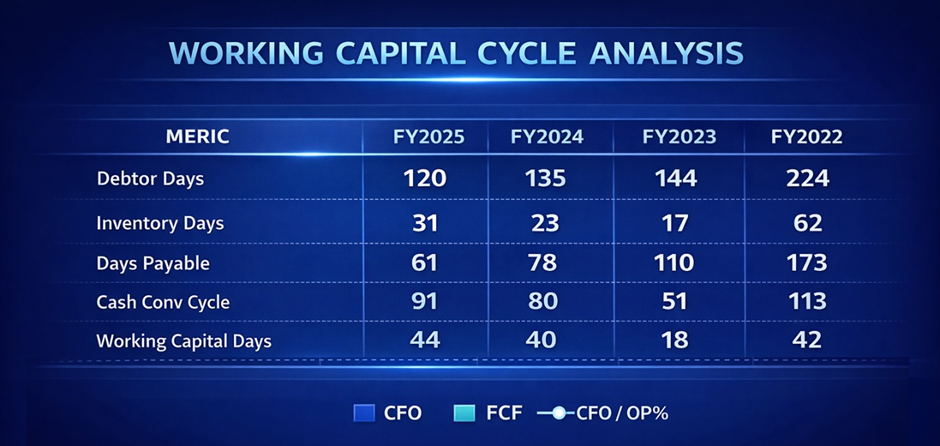

Operating cash flow has been consistently negative across three of four reported years. In FY2025, the company generated ₹200 Cr of operating profit but only ₹-99 Cr of operating cash flow — a CFO/OP ratio of –24%. Free cash flow was –₹103 Cr. The business is consuming cash, not generating it, despite reporting substantial accounting profits.

The explanation lies in the working capital dynamics of government EPC contracts. Debtor days stand at 120 days (FY2025) — meaning GK Energy waits an average of four months to collect payment after completing work. On ₹1,095 Cr of FY2025 revenue, 120 debtor days represents approximately ₹360 Cr of receivables tied up in the working capital cycle at any point. As revenue grows rapidly, this working capital requirement scales proportionally — requiring continuous capital injection to fund the gap between project completion and government payment.

This is the central risk that sophisticated investors are pricing into the 9.97x multiple: the business is highly profitable on paper but cash-consumptive in practice, requiring ongoing debt funding to sustain growth. If government payments slow, debtor days lengthen, or credit markets tighten, the model faces liquidity stress.

Working Capital Trends: Improvement Is Occurring

Data Source: REFINITIV, Analysis: Kalkine Group

The positive trend is debtor days improving from 224 (FY2022) to 120 (FY2025) — a 46% improvement in collection efficiency as the company scales and government payment processes mature. This directional improvement is encouraging but the absolute level of 120 days remains high for a business growing at 166% annually. Every 10-day improvement in debtor days at current revenue scale would release approximately ₹40 Cr of working capital — a meaningful cash flow improvement.

Latest Announcements: Management Building

Source: NSE/BSE filings

27 March 2026 — Insider Purchase Disclosure: A designated person disclosed the purchase of GK Energy shares under SEBI Insider Trading Regulations — a Form C disclosure under Regulation 7(2). Insider buying — particularly by designated persons with access to material non-public information — is one of the most powerful signals of management confidence in near-term business performance. When company insiders buy shares at current prices, they are putting personal capital behind their conviction that the stock is undervalued.

14 March 2026 — Committee Reconstitution: GK Energy reconstituted its Stakeholders, CSR, and Executive Committees effective 14 March 2026 — a governance strengthening signal as the company matures from a small private business into a regulated, listed entity with expanding institutional ownership responsibilities.

14 March 2026 — New Management Appointments: Two significant appointments: Ramawatar Suresh Laddad as Assistant General Manager–Accounts (effective 1 April 2026) and Shubham Suresh Jain as Company Secretary and Compliance Officer (effective 16 March 2026). For a recently listed company, the appointment of a dedicated Company Secretary and AGM–Accounts signals investment in the governance and financial reporting infrastructure appropriate for a listed entity — a positive maturation signal.

25 March 2026 — Trading Window Closure: Trading window closed ahead of Q4 FY2026 results — confirming full-year audited results are imminent. Given the December 2025 quarter delivered net profit of ₹59 Cr on ₹460 Cr revenue, Q4 FY2026 results will be the first full-year FY2026 picture available to the market.

Shareholding: Promoter-Dominated, Institutions Arriving

Data Source: REFINITIV, Analysis: Kalkine Group

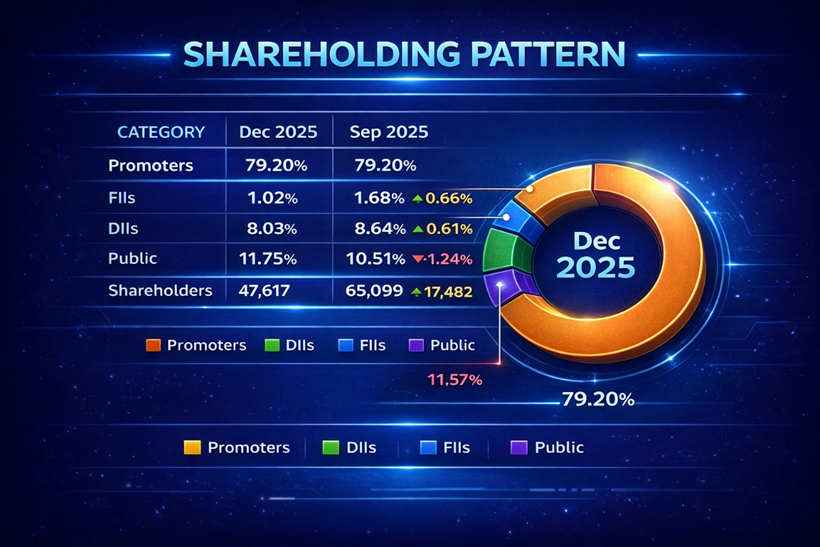

Promoter holding of 79.20% — stable and high — reflects a business still firmly in founder control. This is a double-edged characteristic: strong promoter alignment with minority shareholders but a thin free float of approximately 20.8%, or roughly ₹385 Cr at current prices. Thin free floats amplify both upside and downside price moves.

DII ownership of 8.03% — while modest — confirms that domestic mutual funds and institutions have begun to establish positions. This is significant: institutional presence provides a valuation anchor and creates liquidity for larger investors who need to build meaningful positions. The FII holding of 1.02% represents nascent international investor interest at a very early stage.

The drop in shareholder count from 65,099 (September 2025) to 47,617 (December 2025) — a 27% decline in registered shareholders — is an unusual development worth noting. This suggests retail investors have been selling, potentially into the stock's price decline from its 52-week high of ₹240. If retail is exiting and institutions are holding or adding, this sets up a potential re-rating as the shareholder base concentrates in stronger, more patient hands.

The Undervaluation Case: Five Specific Arguments

Argument 1 — P/E Discount Is Unjustified by Fundamentals At 9.97x, GK Energy trades at a 35% discount to the sector median P/E of 15.45x. The sector median ROCE is 18.43%. GK Energy's ROCE is 74.3% — four times the median. There is no rational basis for a ROCE-superior business to trade at a P/E discount to ROCE-inferior peers. Simple sector mean reversion to 15x P/E would imply a price of ₹148 — 62% above current levels. Reversion to the EPC sector average of 25x would imply ₹247 — 170% upside.

Argument 2 — Government Scheme Demand Is Structural and Unexecuted PM-KUSUM's target of 20 lakh (2 million) solar pumps across India is a government commitment backed by central budget allocation. As of the company's founding narrative, GK Energy has installed over 1,00,000 pumps — just 5% of the total scheme target. The remaining 95% of the addressable market has yet to be served. This is not a business approaching market saturation — it is a business in the early innings of a decade-long government mandate.

Argument 3 — Insider Buying at Current Prices The 27 March 2026 disclosure of designated person share purchases is a direct signal that management believes the current price is significantly below fair value. Insiders with full visibility into order book, payment timelines, and Q4 FY2026 financials are buying at ₹91.40 — the strongest possible vote of confidence available.

Argument 4 — TTM EPS of ₹9.90 Growing Rapidly TTM EPS of ₹9.90 at a price of ₹91.40 represents a trailing earnings yield of 10.8% — comparable to fixed income instruments for a business growing profits at 269% annually. The implicit assumption in a 9.97x P/E for a 269% profit growth business is either that profits will collapse imminently or that the business carries existential risk. Neither is supported by the available data.

Argument 5 — Margin Expansion Trend Is Intact OPM has expanded from 7% (FY2022) to 20% (Q3 FY2026) — a structural improvement driven by procurement scale, operational efficiency, and revenue mix. If margins sustain at 20% on TTM revenue of ₹1,466 Cr, operating profit of approximately ₹293 Cr implies earnings power significantly above current reported figures as interest costs are serviced from growing cash flows.

The Bear Case: Why the Discount May Be Partially Justified

Risk 1 — Persistent Negative Operating Cash Flow Four consecutive years of negative or near-zero operating cash flow despite strong accounting profits is a serious concern. Cash is fact; profit is opinion. Until GK Energy demonstrates sustained positive operating cash flow, the quality of its reported earnings is legitimately questioned.

Risk 2 — Rapidly Rising Debt Borrowings have grown from ₹43 Cr (FY2023) to ₹413 Cr (September 2025) in 30 months — a tenfold increase. If revenue growth slows or government payments are delayed, this debt level could become a constraint on operations and a risk to the equity holders.

Risk 3 — Single Scheme Concentration The business is overwhelmingly dependent on PM-KUSUM Component B. Any policy change, scheme modification, budget reallocation, or government programme slowdown directly and immediately impacts revenue. This is scheme risk that is difficult to diversify and impossible to hedge.

Risk 4 — High Debtor Days 120 debtor days — even after improvement from 224 — means GK Energy is effectively providing four months of interest-free financing to government entities on every project. At scale, this requires substantial working capital funding that either consumes equity returns or increases financial leverage.

Risk 5 — IPO-Stage Company GK Energy is a recently listed company with no annual report data available, limited concall history, and a governance infrastructure still being built (new Company Secretary appointed March 2026). The information asymmetry between insiders and external investors is higher than for established listed companies.

Verdict: Undervalued — But with Conditions

The undervaluation case for GK Energy is the strongest available from the data provided. A 9.97x P/E against 101% ROE, 74.3% ROCE, 340% 3-year profit CAGR, and a structural government mandate covering 95% of its served market is a combination that — in any rational market — should command a significantly higher multiple.

The market's discount reflects three legitimate concerns: negative operating cash flow, rapidly rising debt, and scheme concentration risk. These are real risks, not imaginary ones. But they are known risks, already visible in public data, and arguably already more than fully priced at 9.97x earnings.