📌 Key Highlights

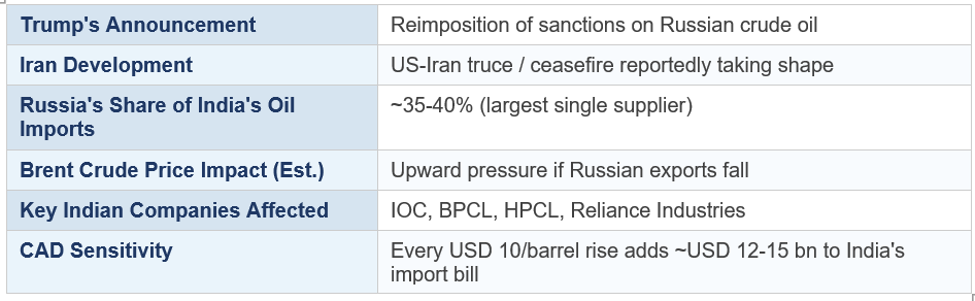

- US President Trump vows to reimpose sanctions on Russian crude oil exports

- Development coincides with emerging US-Iran ceasefire, reshaping global energy supply dynamics

- Russia is currently India's largest crude oil supplier, accounting for ~35-40% of India's oil imports

- Reimposition of Russian oil sanctions could tighten global supply and push Brent crude higher

- Iran deal could partially offset Russian supply reduction if Iranian exports normalise

- Indian refiners (IOC, BPCL, HPCL, Reliance) face supply chain recalibration pressure

- Rupee depreciation risk rises if India's oil import bill increases

📋 Quick Facts

📰 The Story

US President Donald Trump has vowed to reimpose sanctions on Russian crude oil exports, a move that — if implemented — would dramatically reshape global energy flows and pose significant challenges for India, which has emerged as the world's largest buyer of Russian crude since 2022. The announcement came as a separate US-Iran diplomatic channel appears to be yielding a truce framework, creating a complex geopolitical mosaic for oil markets.

Russia became India's dominant crude supplier following the Western sanctions imposed after the Ukraine invasion in 2022. Indian refiners, led by state-owned IOC, BPCL, and HPCL, aggressively scaled up Russian crude purchases — attracted by the steep discounts (initially as high as USD 20-25 per barrel versus Brent) that Russian sellers offered to willing non-Western buyers. By late 2025, Russia accounted for approximately 35-40% of India's total crude imports, displacing traditional suppliers like Saudi Arabia and Iraq.

A reimposition of robust US sanctions — particularly if coordinated with secondary sanction mechanisms targeting third-party banks, shipping companies, and insurers that facilitate Russian oil trade — would force Indian refiners to either curtail Russian crude purchases or risk losing access to US financial systems and dollar-clearing infrastructure. The previous G7 price cap mechanism had limited effectiveness, but direct secondary sanctions on Indian entities would present a far more difficult compliance calculus.

The Iran dimension adds complexity: a US-Iran nuclear deal or ceasefire could unlock approximately 1-2 million barrels per day of Iranian crude for global markets — potentially cushioning the supply reduction from Russian curtailment. Iran had previously supplied Indian refiners at competitive prices and Indian companies have the technical capability to process Iranian crude grades. However, re-establishing Iranian supply chains would take months and involve its own set of diplomatic sensitivities.

For India, the stakes are particularly high. The country imports approximately 85% of its crude oil needs, and the cheap Russian crude has been a significant deflationary input for the economy — suppressing fuel prices, reducing inflation pressure, and protecting the Current Account Deficit (CAD). Any disruption to Russian supply that forces a return to more expensive Middle Eastern or West African grades would have direct macro-economic consequences.

📊 Financial Analysis

The oil market impact of Trump's announcement hinges on the specifics of implementation — particularly whether secondary sanctions are applied to non-US entities trading in Russian crude. A price-cap-only approach (as seen in the G7 USD 60/barrel mechanism) would have limited efficacy given India and China's demonstrated willingness to trade outside Western financial infrastructure. However, secondary sanctions targeting Indian banks and shipping companies would be a different order of magnitude.

For Brent crude prices, the initial announcement creates upward pressure, likely pushing prices toward USD 85-90 per barrel if Russian exports are materially curtailed. The Iran offset could temper this to USD 75-80 per barrel if a deal materialises quickly. Indian energy companies face a transitional period of supply chain recalibration — IOC, BPCL, and HPCL have significant refinery configurations optimised for Russian crude grades, which would require expensive modifications to process alternative crude types.

Reliance Industries, with its more flexible Jamnagar refinery and sophisticated crude procurement operations, is better positioned than PSU refiners to adapt to supply source changes.

💹 Investor Insights

Indian oil marketing companies (OMCs) — IOC (NSE: IOC), BPCL (NSE: BPCL), HPCL (NSE: HINDPETRO) — face near-term headwinds if Russian crude discounts narrow or supply is disrupted. Their marketing margins could compress if retail fuel prices are not raised to offset higher crude costs. Reliance Industries (NSE: RELIANCE) is better insulated given its crude flexibility and downstream petrochemical integration.

At a macro level, higher crude prices widen India's CAD, weaken the rupee, and create inflationary pressure — a combination that historically results in RBI rate hikes or delay in rate cuts. This is negative for rate-sensitive sectors (banking, real estate, NBFCs) and positive for energy sector equities and inflation-linked instruments.

Frequently Asked Questions (FAQs)

- How much of India's crude oil comes from Russia?

- Russia currently accounts for approximately 35-40% of India's total crude oil imports — making it India's single largest supplier, a position it achieved post-2022 as Indian refiners capitalised on discounted Russian crude.

- What are secondary sanctions and why do they matter for India?

- Secondary sanctions penalise non-US entities (companies, banks, countries) that continue to do business with a sanctioned entity. If the US imposes secondary sanctions on Russian crude trade, Indian banks and companies facilitating payments and logistics for Russian oil could be barred from the US financial system — a far more powerful deterrent than the price cap.

- Could Iran replace Russian crude for India?

- Potentially, but not immediately. Re-establishing Iranian supply chains requires diplomatic frameworks, insurance arrangements, and shipping logistics that would take months to operationalise. Iran's maximum additional supply capacity of 1-2 mbpd also cannot fully replace Russia's 1.5-2 mbpd share in India's import basket.

- How does higher oil impact India's economy?

- Every USD 10 per barrel increase in crude prices adds approximately USD 12-15 billion to India's annual import bill, widening the CAD, putting downward pressure on the rupee, and adding inflationary pressure through higher fuel and transportation costs.