India’s banking sector continues to deliver strong growth, stable asset quality, and robust capital buffers. But beneath the surface, a more subtle shift is underway—the leadership hierarchy within the sector is changing.

A comparison across FY25 financials and current market valuations shows that while the sector remains fundamentally healthy, investor preference is moving away from traditional leaders toward more balanced performers.

The latest data on total income, net interest margins (NIM), and price-to-book (P/B) ratios highlights this transformation.

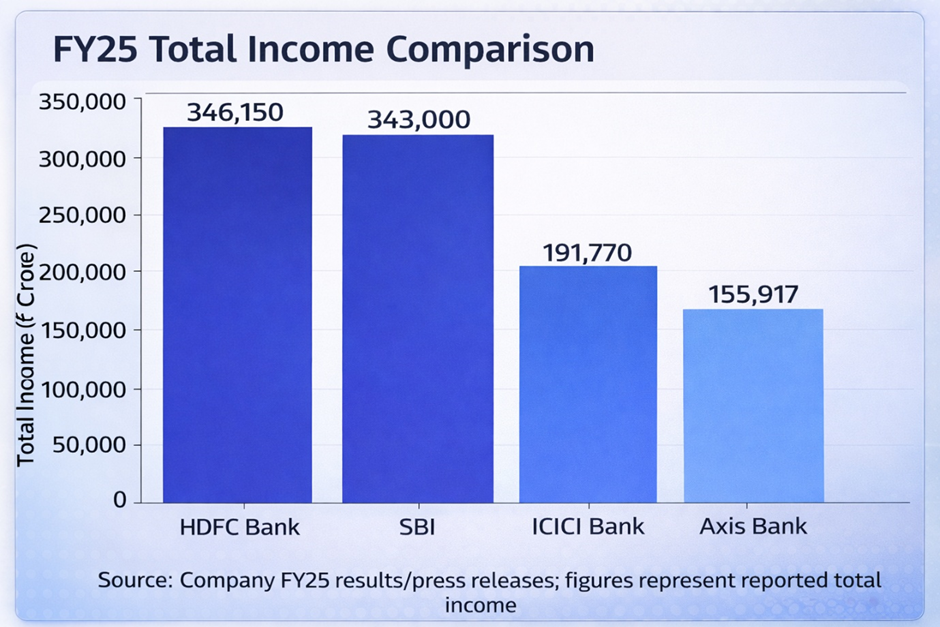

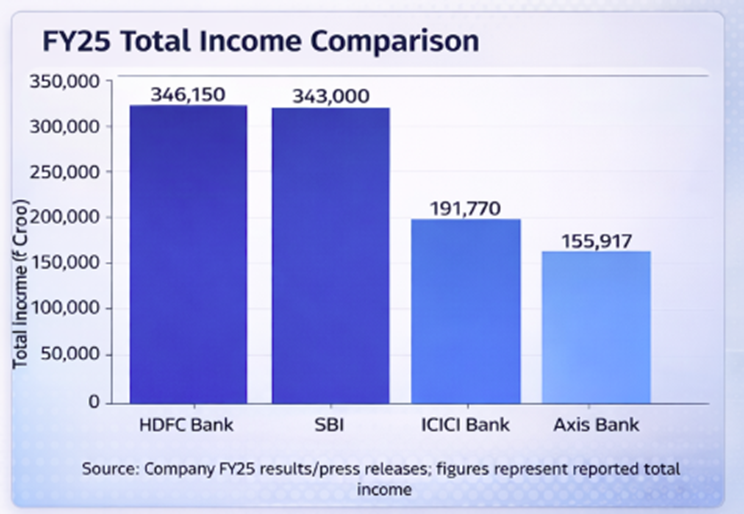

FY25 Total Income Comparison

The above chart captures the scale of India’s banking giants.

HDFC Bank (NSE:HDFC) and SBI (NSE:SBI) continue to dominate in terms of total income, reflecting their massive balance sheets and extensive lending franchises. ICICI Bank (NSE:ICICIBANK) and Axis Bank (NSE: AXISBANK) follow at a considerable distance, while Kotak Mahindra Bank (NSE:KOTAKBANK) remains relatively smaller but more focused.

Key insights

Scale remains a defining strength of the Indian banking system. However, size alone is no longer sufficient to command premium valuations.

HDFC Bank, despite being among the largest, is no longer viewed as the undisputed sector leader—a sharp departure from its historical positioning.

FY25 Net Interest Margin (NIM) Comparison

Margins provide a clearer view of operational efficiency and profitability.

Kotak Mahindra Bank leads the sector on NIM, followed by ICICI Bank. HDFC Bank now sits in the middle of the pack, while SBI trails due to structural constraints typical of PSU banks.

Key insight

The sector is now divided into:

- Efficiency leaders: Kotak, ICICI

- Scale leaders: HDFC, SBI

HDFC Bank’s decline in margin leadership is particularly notable. For years, it consistently delivered best-in-class profitability. Today, it is adjusting to:

- Post-merger balance sheet changes

- Higher cost of funds

- Deposit mix challenges

This shift has played a crucial role in its valuation correction.

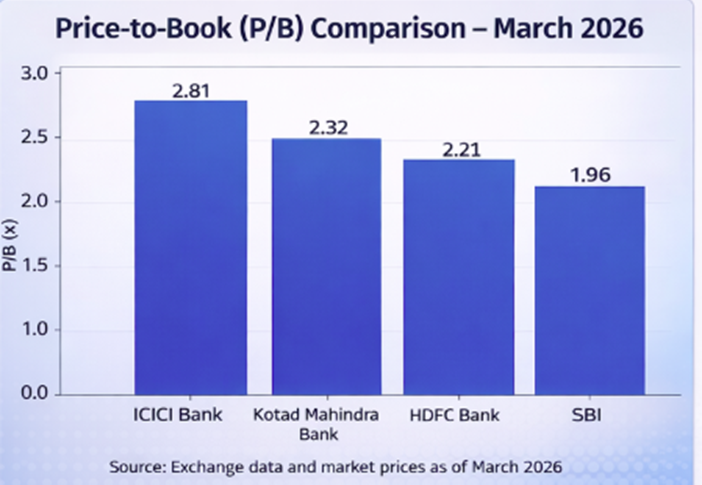

Price-to-Book (P/B) Comparison – March 2026

The valuation chart reveals the most significant change in market perception.

ICICI Bank now commands the highest P/B multiple among peers, followed by Kotak Mahindra Bank. HDFC Bank, once the sector’s premium stock, now trades below both.

PSU banks like SBI continue to trade at lower multiples, reflecting structural discounting despite improving fundamentals.

Key insights

This marks a structural re-rating within the sector.

For over a decade:

- HDFC Bank was the benchmark for quality

- It consistently traded at a significant premium

Today:

- That premium has narrowed sharply

- ICICI Bank has emerged as the new “balanced leader”

The big picture: A sector in transition, not distress

When the three charts are viewed together, a clear pattern emerges:

|

Metric |

Leader |

|

Scale |

HDFC Bank / SBI |

|

Profitability |

Kotak / ICICI |

|

Valuation |

ICICI |

No single bank dominates across all metrics anymore.

This is not a sign of weakness—it is a sign of maturity and diversification within the sector.

Why the sector remains fundamentally strong

Despite the shift in leadership, the Indian banking system remains on solid footing:

- Credit growth continues at a healthy pace

- Asset quality remains stable across banks

- Capital adequacy ratios are strong

- Retail and digital lending are driving expansion

There are no broad-based stress indicators. Instead, the sector is undergoing a reallocation of investor preference.

Winners and laggards: The new hierarchy

ICICI Bank: The new benchmark

ICICI Bank has emerged as the market favourite due to:

- Strong margins

- Consistent execution

- Balanced growth across segments

Its leadership in valuation reflects investor confidence in sustainability.

Kotak Mahindra Bank: Premium for quality

Kotak continues to command high margins and a conservative balance sheet.

While growth concerns persist, its profitability ensures it remains a premium franchise.

HDFC Bank: From dominance to transition

HDFC Bank remains a high-quality franchise, but the narrative has changed.

- Scale remains intact

- Margins have moderated

- Governance concerns have added uncertainty

The stock is now seen as a transition story rather than a pure compounder.

SBI and PSU banks: Value plays

PSU banks offer:

- Strong earnings momentum

- Lower valuations

They are increasingly seen as cyclical opportunities rather than structural compounders.

What investors should watch next

The next phase of sector performance will depend on:

- Margin trajectory across private banks

- Deposit growth and funding costs

- Execution consistency, especially for large banks

- Resolution of governance concerns (in specific cases like HDFC Bank)

Any improvement in these areas could trigger a re-rating cycle.

Bottom line

India’s banking sector is not weakening—it is evolving.

The data shows a decisive shift:

- From scale dominance to efficiency-driven valuation

- From single leader to multiple specialised leaders

For investors, the takeaway is clear:

The sector’s strength remains intact, but the playbook has changed.

Choosing the right bank now depends not just on size, but on profitability, execution, and market perception.