Adani Power (NSE:ADANIPOWER) vs Adani Energy Solutions (NSE:ADANIENSOL) is one of the most debated stock comparisons among Indian energy sector investors in 2026. Both companies operate within the Adani Group's power cluster, yet they serve fundamentally different functions: Adani Power (NSE:ADANIPOWER) generates electricity from coal-fired thermal plants, while Adani Energy Solutions (NSE:ADANIENSOL) transmits, distributes, and meters electricity across India's grids.

Understanding the distinction is critical before investing. Thermal power generation (Adani Power (NSE:ADANIPOWER) ) is capital-intensive, cyclical, and exposed to fuel cost and merchant tariff volatility. Power transmission and smart metering (AESL) is a regulated-return, quasi-utility business with long-term contracted revenue — but it commands a significantly higher valuation premium. This article examines both stocks across business model, financials, growth, debt, valuation, risks, and long-term outlook to help Indian retail investors make an informed comparison.

Sector Overview: India's Power Ecosystem in 2026

India's electricity demand is growing at 7-8% annually, driven by industrial growth, urbanisation, air-conditioning penetration, and EV charging infrastructure. The country faces a dual challenge: meeting immediate baseload demand (thermal's domain) while transitioning to renewables over the next two decades. This creates a simultaneous need for new thermal capacity to bridge the gap and a massive upgrade of transmission and distribution infrastructure to carry renewable power from remote generation sites to consumers.

India's Ministry of Power has mandated 300+ million smart meters nationally to modernise the distribution system and reduce aggregate technical and commercial (AT&C) losses. Meanwhile, the power transmission sector requires an estimated Rs 9.15 lakh crore in investment by 2032 to keep pace with generation additions. Both Adani Power (NSE:ADANIPOWER) and AESL are positioned to capture large portions of these opportunities — in fundamentally different ways.

Why This Matters in 2026

- Adani Power (NSE:ADANIPOWER) hit a record high of Rs 254.15 on May 29, 2026; AESL surged 61% in six months to hit a three-year high.

- India's peak power demand continues to set records, keeping thermal plants running at high plant load factors.

- The smart metering rollout and renewable integration require a completely modernised transmission grid — a multi-trillion-rupee opportunity.

- The partial resolution of the US legal case (SEC settlement in May 2026) has improved investor sentiment across all Adani stocks.

Key Companies: At a Glance

Company-by-Company Analysis

Adani Power (NSE:ADANIPOWER) Limited: Business Model and Operations

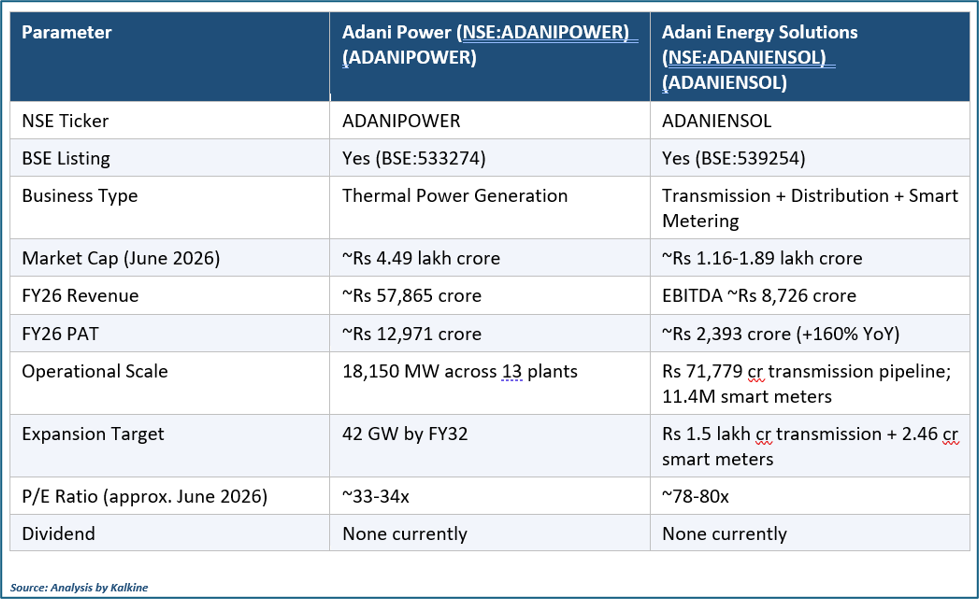

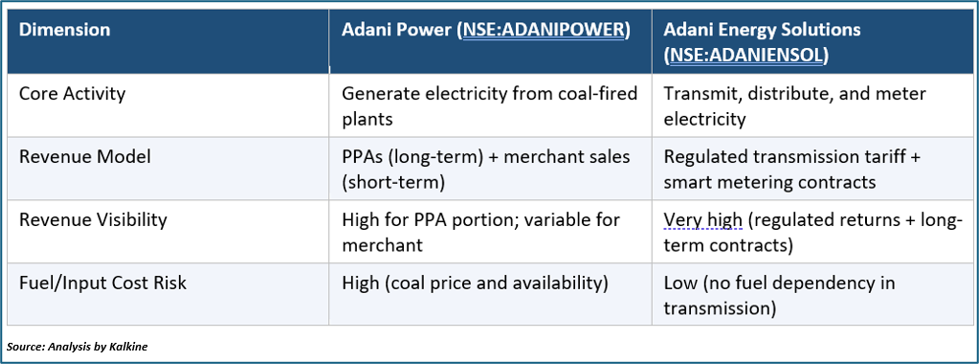

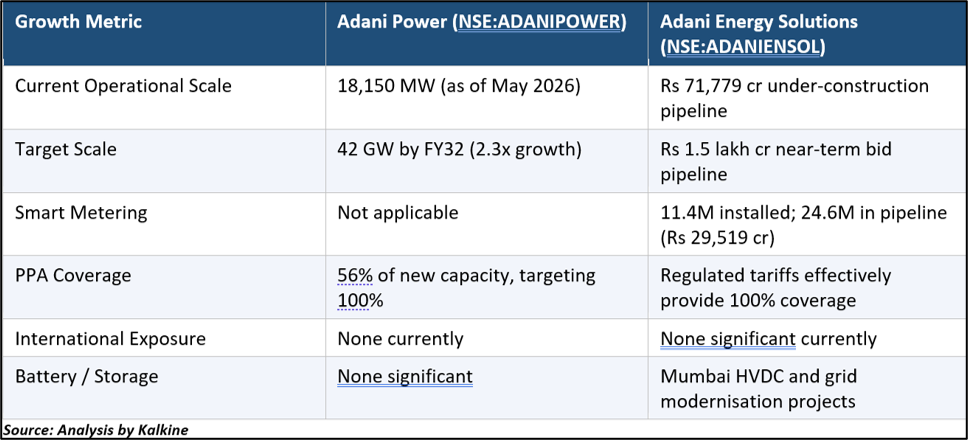

Adani Power (NSE:ADANIPOWER) Limited (APL) is India's largest private thermal power producer. As of May 2026, it operates 18,150 MW of installed capacity across 13 power plants in 8 states — representing approximately 3.82% of India's total installed power capacity. The plants predominantly run on coal (domestic and imported) and are connected to state distribution companies (DISCOMs) and large industrial consumers via long-term Power Purchase Agreements (PPAs).

The business model is straightforward: build large thermal plants, sign long-term PPAs to secure revenue visibility, and operate at high plant load factors (PLFs) to maximise profitability. A portion of capacity operates under shorter-term or merchant arrangements, which provides upside when spot power prices are high but adds revenue volatility. APL's power is critical for grid stability as renewable intermittency rises.

Adani Power (NSE:ADANIPOWER) : Financial Performance FY2026

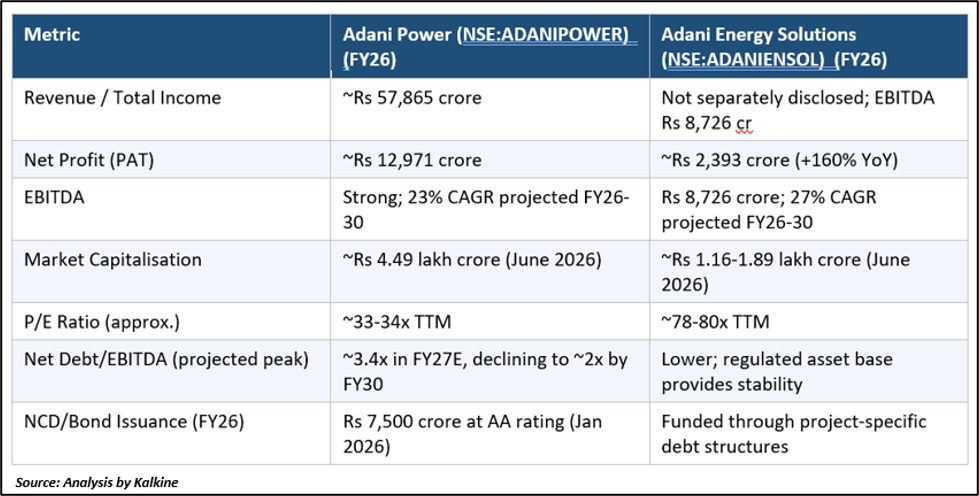

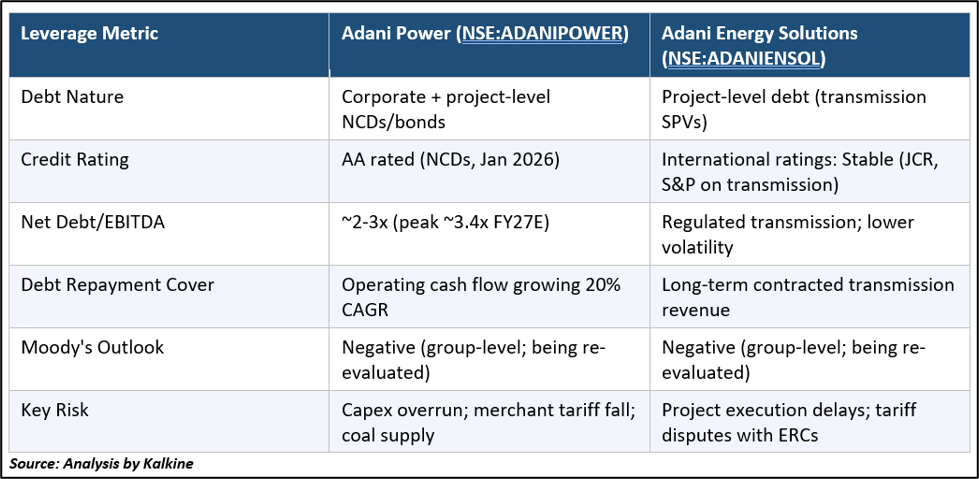

For FY2026, Adani Power (NSE:ADANIPOWER) reported revenue of approximately Rs 57,865 crore and net profit of approximately Rs 12,971 crore. In Q4 FY26, consolidated revenues grew 23% quarter-on-quarter and 10% year-on-year. The company raised Rs 7,500 crore through AA-rated Non-Convertible Debentures (NCDs) in four tranches in January 2026 to fund capacity expansion. Adani Power (NSE:ADANIPOWER) 's cash position and operating cash flow are improving as existing capacity generates steady EBITDA.

Adani Power (NSE:ADANIPOWER) : Expansion Plan to 42 GW by FY32

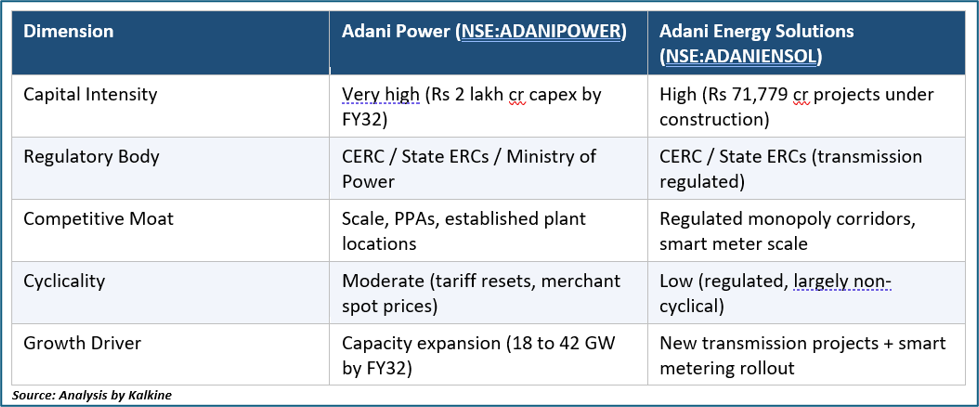

APL's most compelling long-term narrative is its 2.3x capacity expansion plan from 18.3 GW to 42 GW by FY32, backed by Rs 2 lakh crore of investment. Land acquisition and equipment contracts with L&T and BHEL have reportedly been secured for the full 42 GW target. Of the upcoming 23.7 GW addition, 56% is already tied to long-term PPAs, with management targeting 100% PPA coverage

Adani Energy Solutions (NSE:ADANIENSOL) : Business Model and Operations

Adani Energy Solutions (NSE:ADANIENSOL) Limited (AESL) operates India's largest private power transmission network and is diversifying rapidly into distribution infrastructure and smart metering. The company transmits high-voltage electricity across thousands of kilometres of transmission lines and substations, connecting generation plants to state grids. Unlike thermal power, transmission is a regulated business: returns are determined by the Central Electricity Regulatory Commission (CERC) or State ERCs, providing stable, predictable cash flows.

In addition to transmission, AESL has built a smart metering business that has emerged as one of its fastest-growing segments. Smart meters replace old electromechanical meters with digital, two-way communicating devices that reduce power theft, enable dynamic tariffs, and improve billing efficiency. The Indian government's RDSS (Revamped Distribution Sector Scheme) targets universal smart metering — an enormous addressable market.

Adani Energy Solutions (NSE:ADANIENSOL) : Financial Performance FY2026

AESL delivered a standout FY26 performance. Full-year PAT surged 160% YoY to Rs 2,393 crore, while operating EBITDA rose 12.7% to Rs 7,407 crore and total EBITDA reached Rs 8,726 crore. The company commissioned five major transmission projects during FY26: Mumbai HVDC, North Karanpura Transmission, Khavda Phase II Part-A, Khavda Pooling Station-1, and Sangod Transmission. Smart meter installations reached 11.4 million (vs 3.1 million a year prior), smashing its own 7 million target.

Adani Energy Solutions (NSE:ADANIENSOL) : Transmission and Smart Metering Pipeline

AESL's growth runway is visible and large. The aggregate transmission pipeline under construction stands at Rs 71,779 crore, representing a 20% YoY increase in project wins. The broader near-term tendering opportunity is approximately Rs 1.5 lakh crore versus only Rs 54,000 crore at end-FY25 — a near tripling of the addressable bid pipeline. The smart meter order book is 2.46 crore meters with revenue potential of Rs 29,519 crore. AESL became the first Indian company to install 1 crore smart meters, redefining execution benchmarks.

Head-to-Head Comparison: Business Model

Head-to-Head Comparison: Financials

Head-to-Head Comparison: Debt and Leverage

Head-to-Head Comparison: Growth and Expansion

Recent News and Market Triggers

- Adani Power (NSE:ADANIPOWER) record high (May 29, 2026): Stock reached Rs 254.15, recovering sharply from post-indictment lows.

- AESL 61% rally in six months: Stock hit a three-year high of Rs 1,591, driven by FY26 results and transmission wins.

- AESL Q4 FY26 dhamaka: PAT surged 160% YoY; five major transmission projects commissioned.

- Adani Power (NSE:ADANIPOWER) Rs 7,500 cr NCD (January 2026): AA-rated bond issue signals strong market access for capacity expansion.

- Smart meter milestone: AESL became the first Indian company to install 1 crore smart meters, ahead of targets.

- Adani Power (NSE:ADANIPOWER) Q4 FY26: Revenue grew 23% QoQ and 10% YoY; stock retreated slightly as investors booked profits after record rally.

Growth Drivers

Adani Power (NSE:ADANIPOWER) Growth Drivers

- India's rising electricity demand (7-8% annual growth) keeps plant load factors high for existing and new capacity.

- Thermal power remains essential for baseload stability as India's renewable share rises but intermittency increases.

- 3x capacity expansion to 42 GW by FY32, backed by Rs 2 lakh crore capex already in motion.

- 56% of new capacity covered by PPAs, providing revenue visibility; target is 100% PPA coverage.

- Strong operating cash flow growth (projected 20% CAGR) improves debt serviceability.

- India's manufacturing sector expansion and data centre growth are driving industrial electricity demand.

Adani Energy Solutions (NSE:ADANIENSOL) Growth Drivers

- India's national transmission grid requires Rs 9.15 lakh crore of investment by 2032; AESL's bid pipeline is Rs 1.5 lakh crore.

- Smart metering mandate: 300+ million meters to be installed nationally under RDSS, creating a decade-long order book.

- AESL's first-mover advantage in smart metering — only company to have installed 1 crore meters — creates strong execution credibility for future bids.

- Renewable energy integration requires high-voltage direct current (HVDC) corridors and new substations — AESL is executing Mumbai HVDC.

- Regulatory model provides high revenue predictability with tariff determined by CERC for each project.

Risks Investors Should Know

Adani Power (NSE:ADANIPOWER) : Key Risks

- Coal supply and price risk: Dependence on domestic and imported coal exposes the company to fuel cost volatility and supply disruptions.

- Merchant power risk: Capacity operating under short-term/spot arrangements faces electricity price cyclicality.

- Execution risk: Expanding from 18 GW to 42 GW is an enormous undertaking; delays or cost overruns could impair returns.

- PPA renegotiation risk: DISCOMs under financial stress may seek tariff revisions or delay payments.

- High capex peak leverage: Net debt/EBITDA expected to peak at ~3.4x in FY27 before declining — any revenue shortfall during this window increases financial risk.

- Regulatory and policy risk: Thermal power plant environmental norms are tightening; future regulations may impose additional compliance costs.

- Group governance risk: Group-level governance concerns (US SEC/DOJ case) cast a shadow, though the situation is moving towards resolution.

Adani Energy Solutions (NSE:ADANIENSOL) : Key Risks

- Project execution risk: Managing a Rs 71,779 crore under-construction pipeline simultaneously is operationally challenging; delays reduce returns.

- Tariff dispute risk: Revenue from regulated transmission assets depends on timely tariff determination by CERC/State ERCs; disputes can defer income.

- Valuation risk: Trading at ~78-80x P/E, AESL leaves limited margin of safety; any earnings miss or negative sentiment could trigger sharp correction.

- DISCOM payment delays: Smart metering revenue depends on state DISCOMs — many are financially weak. Payment delays are a structural risk.

- Competitive intensity: Power Grid Corporation and other private players (Sterlite, Kalpataru) compete for the same transmission bids.

- Group concentration risk: As an Adani Group entity, adverse group-level news impacts stock price regardless of standalone fundamentals.

- Leverage risk: Project-level debt at transmission SPVs is substantial; rising interest rates or refinancing risk could affect project economics.

Valuation Considerations

Adani Power (NSE:ADANIPOWER) at ~33-34x P/E trades at a notable discount to the broader utilities sector average of approximately 39x, and well below sector peers like NTPC (~18x) when accounting for its faster growth trajectory. The stock's Price-to-Book ratio is approximately 7.15x, reflecting the market's confidence in its return on equity going forward. No dividend is paid, with all earnings being reinvested into expansion.

Adani Energy Solutions (NSE:ADANIENSOL) at ~78-80x P/E commands a significant premium over Power Grid Corporation (~20x P/E) and Tata Power (~40x), but this premium has compressed substantially from its peak of 991% over PGCIL to approximately 133% as of June 2026 — suggesting that earnings have grown faster than the share price in recent quarters. For growth-oriented investors, the compression of this premium may represent an improving entry point, subject to one's own assessment.

Long-Term Outlook

Both Adani Power (NSE:ADANIPOWER) and Adani Energy Solutions (NSE:ADANIENSOL) are beneficiaries of India's multi-decade energy infrastructure supercycle. The comparison is less about which is 'better' and more about what investment profile an investor prefers.

Adani Power (NSE:ADANIPOWER) is a classic capacity expansion play — a pure-play thermal generator that is expanding aggressively into a market where baseload power demand is structurally rising. The investment thesis centres on whether India's electricity demand growth is sustained, whether the 42 GW expansion is executed on time and cost, and whether the PPA revenue base is protected. At ~33-34x P/E, the stock trades at a relative discount compared to the sectoral average, though leverage will rise near-term.

Adani Energy Solutions (NSE:ADANIENSOL) is a regulated-infrastructure growth compounder with the added kicker of a high-growth smart metering business. Its EBITDA CAGR projection of 27% through FY30 is the highest in the Adani energy cluster, and the regulated nature of transmission reduces earnings volatility. However, it trades at a significant valuation premium that requires sustained execution. AESL's 160% PAT growth in FY26 suggests the earnings power is real and growing.

Investors seeking value plus capacity-led growth may find Adani Power (NSE:ADANIPOWER) relatively more attractive given its lower P/E multiple. Those seeking quality-regulated infrastructure with smart metering optionality may prefer AESL despite the premium. Critically, both stocks carry group-level risk factors that investors must independently evaluate.

Frequently Asked Questions

Q: What is the fundamental difference between Adani Power and Adani Energy Solutions?

A: Adani Power (NSE:ADANIPOWER) generates electricity using coal-fired thermal power plants. Adani Energy Solutions (NSE:ADANIENSOL) transmits high-voltage electricity across the grid, distributes it to end consumers, and installs smart meters. In simple terms: Adani Power (NSE:ADANIPOWER) produces power; AESL moves and meters it. They complement each other in India's electricity value chain but have very different business risk profiles, revenue models, and growth trajectories.

Q: Is Adani Power (NSE:ADANIPOWER) or Adani Energy Solutions (NSE:ADANIENSOL) more expensively valued?

A: On a traditional P/E basis, Adani Energy Solutions (NSE:ADANIENSOL) at ~78-80x is significantly more expensive than Adani Power (NSE:ADANIPOWER) at ~33-34x. However, AESL's regulated business model and fast PAT growth may justify a part of the premium. Adani Power (NSE:ADANIPOWER) 's P/E is actually below the sector average of ~39x, suggesting it may be pricing in less growth than analysts project. Valuations change daily; always check current ratios on NSE or financial platforms before deciding.

Q: What are the key risks specific to each stock?

A: Adani Power (NSE:ADANIPOWER) 's key risks include coal supply volatility, merchant power price cyclicality, execution risk on its 42 GW expansion, and high peak leverage. AESL's key risks include project execution delays on its large pipeline, tariff disputes with regulators, DISCOM payment delays on smart metering, and its premium valuation leaving less room for error. Both share group-level governance and concentration risks.

Q: Does either company pay dividends?

A: As of June 2026, neither Adani Power (NSE:ADANIPOWER) nor Adani Energy Solutions (NSE:ADANIENSOL) pays dividends. Both are reinvesting profits and cash flows into large-scale expansion programmes. Income-seeking investors may prefer dividend-paying utilities like Power Grid Corporation or NTPC.

Q: How does the US SEC case affect these stocks?

A: In May 2026, Gautam Adani and Sagar Adani agreed to pay $18 million to settle SEC fraud allegations linked to solar power contracts. The US DOJ is reportedly unlikely to pursue related criminal charges. These developments reduced a major governance overhang across all Adani stocks. However, the court's formal approval of the settlement is still pending as of June 2026. Investors should monitor official regulatory announcements.

Q: Can I hold both Adani Power (NSE:ADANIPOWER) and Adani Energy Solutions (NSE:ADANIENSOL) together?

A: Holding both means exposure to two different parts of India's power value chain — generation and transmission/metering. This offers some business-model diversification within the sector. However, both are Adani Group entities, so group-level risks — governance, leverage, promoter concentration, regulatory scrutiny — remain common to both. Broader portfolio diversification beyond the Adani Group is generally advisable. Consult a SEBI-registered investment adviser for personalised guidance.

Conclusion

The Adani Power (NSE:ADANIPOWER) vs Adani Energy Solutions (NSE:ADANIENSOL) comparison reveals two compelling but structurally different investment propositions. Adani Power (NSE:ADANIPOWER) is a high-capacity, lower-P/E, fuel-dependent thermal generator with massive expansion ambitions — offering growth at a relatively moderate valuation if execution holds. Adani Energy Solutions (NSE:ADANIENSOL) is a regulated, higher-quality infrastructure compounder with the added optionality of India's largest smart metering business — commanding a premium valuation that is increasingly backed by demonstrated earnings power.

Neither stock is inherently superior. Adani Power (NSE:ADANIPOWER) may suit investors who believe thermal power remains essential to India's grid through the 2030s and who are comfortable with execution and fuel risk at a lower P/E entry point. AESL may suit investors willing to pay a premium for regulated returns, visible pipeline, and a transformative smart metering opportunity. Both carry group-level concentration and governance risks that require ongoing monitoring. All figures should be independently verified on NSE/BSE before any investment decision.