The BEL vs HAL vs BDL comparison is the most debated question in India's defence investment community. All three are Navratna public-sector enterprises under the Ministry of Defence, all are listed on the NSE and BSE, and all are direct beneficiaries of India's Atmanirbhar Bharat defence manufacturing push. Yet they differ fundamentally in their business models, revenue drivers, growth trajectories, margin profiles, valuations, and risk characteristics.

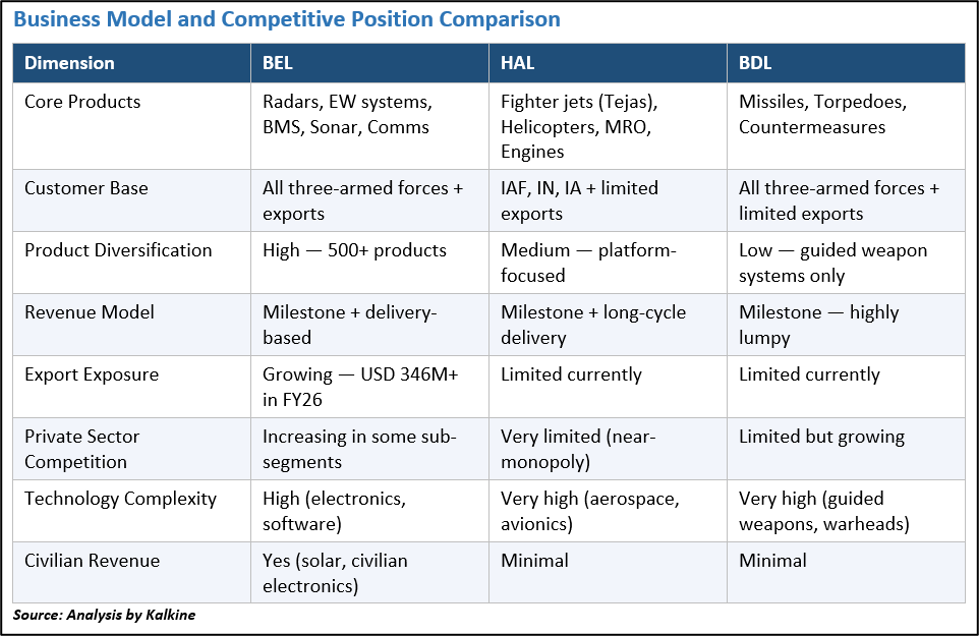

BEL (Bharat Electronics Limited) is the diversified defence electronics giant — radars, electronic warfare, communication systems. HAL (Hindustan Aeronautics Limited) is the aerospace behemoth — fighter jets, helicopters, engines, maintenance repair and overhaul. BDL (Bharat Dynamics Limited) is the specialist missile and guided weapon systems maker. Each occupies a distinct and critical role in India's defence ecosystem.

This article provides a comprehensive, data-driven comparison of these three companies across ten dimensions: business model, market position, financial performance, order book, profitability and margins, valuation, dividends, key risks, and long-term potential. All figures are based on publicly available FY26 data; verify current prices and fresh data on NSE/BSE before acting.

Sector Overview

India's Union Budget FY27 allocated Rs 7.85 lakh crore to defence — the highest-ever allocation. Capital spending rose to approximately Rs 2.19 lakh crore, with 75% earmarked for domestic procurement. Defence exports hit a record Rs 38,424 crore in FY26, up 62.66% YoY. Five Positive Indigenisation Lists covering 5,500+ items restrict imports, channelling orders to domestic manufacturers including BEL, HAL, and BDL.

All three companies are Navratna PSUs — a status that grants them greater financial and operational autonomy. They are zero-debt or near-zero-debt entities with strong balance sheets, captive government customers (the Indian Armed Forces), and long-order-book visibility. The Nifty India Defence index reflects their collective importance to India's listed defence universe.

Why Defence Stocks Matter in 2026

India's defence modernisation is a multi-decade structural programme. The Tejas Mk-1A programme alone has a cumulative contracted value of approximately Rs 1.13 lakh crore across 180 aircraft. Project 75 submarines, P17 Alpha frigates, Akash Next Generation missile systems, next-generation radars, and the Advanced Medium Combat Aircraft (AMCA) programme will sustain demand for BEL, HAL, and BDL products well into the 2030s.

Geopolitical pressures — ongoing border sensitivities and a push for strategic autonomy — have added urgency to defence modernisation. Emergency and fast-track procurement mechanisms have accelerated order conversion. HAL is targeting Tejas Mk-1A deliveries from August-September 2026. BEL is scaling up radar, electronic warfare, and communication system production. BDL is positioned for Akash, Konkurs, and Man-Portable Air Defence System (MANPADS) production ramp-ups.

Company-by-Company Analysis

BEL — Bharat Electronics Limited (NSE:BEL): Diversified Defence Electronics Leader

Business Model: BEL designs, develops, and manufactures a vast portfolio of defence electronics — radars (air defence, battlefield surveillance, fire control), electronic warfare systems, communication equipment, sonar systems, battlefield management systems, night-vision devices, solar photovoltaics, and civilian electronics. This diversification is a key strength: no single programme dominates revenues, reducing lumpy execution risk.

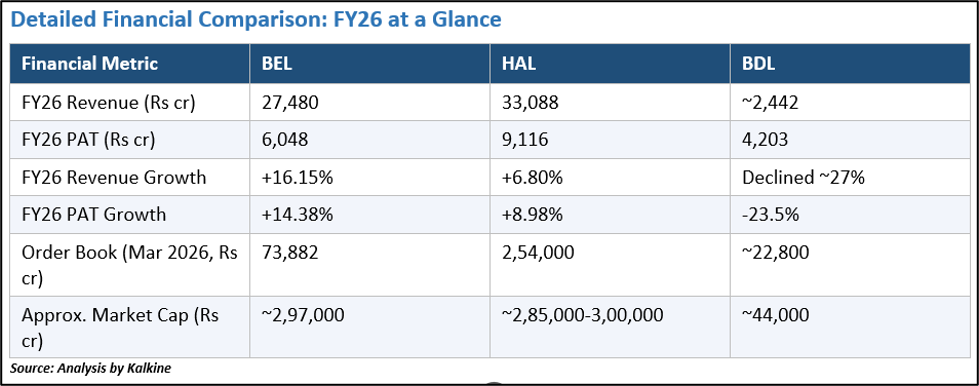

FY26 Performance: BEL delivered record revenue of Rs 27,480 crore (up 16.15% YoY) and PAT of Rs 6,048 crore (up 14.38%). The company secured fresh orders of approximately Rs 30,000 crore during FY26, including USD 346 million in export orders. As of April 1, 2026, the order book stood at Rs 73,882 crore — approximately 2.5-3 years of revenue coverage. Q4 FY26 standalone net profit rose 5% YoY. The PAT margin is approximately 14.67% based on trailing twelve months.

Strengths: Broad product portfolio reduces single-programme risk; strong export order momentum; consistent 15-20% revenue growth guidance; Navratna status provides operational flexibility. Weaknesses/Risks: Premium valuation at ~49-54x P/E; limited non-defence revenue diversification; faces some competition from private sector in new electronics tenders.

HAL — Hindustan Aeronautics Limited (NSE:HAL): Aerospace Giant with Unprecedented Order Book

Business Model: HAL designs, manufactures, and maintains military aircraft, helicopters, jet engines, and aero-structures. It is India's only manufacturer of fighter aircraft (Tejas LCA) and advanced helicopters (Dhruv ALH, LCH Prachand, LUH). The MRO (maintenance, repair and overhaul) business provides recurring, high-margin revenue from servicing the existing fleet. HAL also has a growing aerospace manufacturing role under programmes like AMCA and the HLFT-42 advanced jet trainer.

FY26 Performance: HAL reported consolidated revenue of Rs 33,088 crore (up ~6.8% YoY) and PAT of Rs 9,116 crore (up ~8.98%). While revenue growth was below the prior year's pace, the company's order book reached a record Rs 2.54 lakh crore by March 2026 — up from Rs 1.89 lakh crore at the start of FY26. This 7.7x order-book-to-revenue ratio provides extraordinary long-term visibility. HAL targets 10-12% revenue growth and 30-31% EBITDA margins in FY27. Tejas Mk-1A deliveries are expected to begin August-September 2026.

Strengths: Unmatched order book depth (Rs 2.54 lakh crore); near-monopoly in Indian fighter aircraft manufacturing; strong MRO revenue; high EBITDA margins (30-31% guided); zero debt. Weaknesses/Risks: Revenue growth in FY26 was moderate (6.8%) despite record order book — execution and delivery delays are a chronic risk; high dependence on a single customer (Indian Air Force/Navy/Army); Tejas Mk-1A delivery timeline has shifted multiple times.

BDL — Bharat Dynamics Limited (NSE:BDL): Strategic Missile Maker with Near-Term Headwinds

Business Model: BDL is India's only public-sector manufacturer of guided missile systems, underwater weapons (torpedoes), and countermeasures. Its products include the Akash surface-to-air missile, Milan anti-tank guided missile, Konkurs anti-tank system, and MANPADS. BDL also manufactures allied products like launchers and test equipment. Its strategic importance is irreplaceable — no private-sector entity replicates its role — but this also means limited competitive agility.

FY26 Performance: FY26 was a difficult year for BDL. Full-year profit declined 23.5% to Rs 4,203 crore (from Rs 5,496 crore in FY25) and revenue fell from approximately Rs 3,345 crore to approximately Rs 2,442 crore, driven by order execution timing, supply chain constraints, and programme delays. Q4 FY26 PAT fell 58.5% YoY. The order book stands at approximately Rs 22,800 crore, with additional orders of Rs 15,000 crore envisaged for FY27. The board recommended a final dividend of Rs 0.40 per share for FY26, with an interim of Rs 4.50 per share already paid.

Strengths: Sole public-sector missile systems manufacturer — strategically irreplaceable; Rs 22,800 crore+ order book provides future revenue visibility; new programmes (Akash-NG, MPATGM) in pipeline. Weaknesses/Risks: FY26 earnings contraction is significant; stock trades at ~105x trailing P/E — very expensive relative to current earnings; FII holdings declining; revenue is highly lumpy due to milestone-based recognition; single-product-category concentration risk.

Recent News & Market Triggers

- BEL secured fresh orders of ~Rs 30,000 crore in FY26, including USD 346 million in export orders; order book reached Rs 73,882 crore.

- HAL's order book hit a record Rs 2.54 lakh crore by March 2026, up from Rs 1.89 lakh crore at the start of FY26.

- Tejas Mk-1A deliveries targeted for August-September 2026; approximately 20 aircraft planned for FY27.

- BDL FY26 full-year profit fell 23.5% to Rs 4,203 crore; Q4 PAT declined 58.5% YoY — a significant negative surprise.

- FII holding in BDL fell from 3.77% (June 2025) to 2.02% (March 2026), signalling institutional caution.

- FY27 defence budget of Rs 7.85 lakh crore with capital outlay of Rs 2.19 lakh crore — direct order flow trigger for all three.

- Defence exports hit Rs 38,424 crore in FY26 (up 62.66%), adding to BEL's export order momentum.

- BusinessToday Q3 preview and target price analysis (Jan 2026) highlighted budget triggers and re-rating potential.

- Nifty India Defence corrected ~11% from its peak post-Budget 2026 before recovering.

Growth Drivers

- HAL — Tejas Mk-1A programme: 180 aircraft contracted (83+97 tranches) worth ~Rs 1.13 lakh crore; FY27 guidance of 20 deliveries.

- BEL — Electronic warfare scale-up: Growing share of radar, EW, and BMS contracts driven by India's border security modernisation.

- BDL — Akash-NG and new missiles: Akash Next Generation, MPATGM (Man-Portable Anti-Tank Guided Missile), and export opportunities.

- All three — PILs and indigenisation: Import bans on 5,500+ items force domestic procurement, protecting order pipelines.

- All three — Defence exports: Rs 50,000 crore export target by 2029; BEL already exporting USD 346M+/year.

- HAL — AMCA and future platforms: Advanced Medium Combat Aircraft and other next-generation programmes ensure multi-decade relevance.

- BEL — Civilian electronics diversification: Growing presence in solar photovoltaics and civilian electronics provides revenue diversification.

- All three — Zero-debt balance sheets: Capital-light growth model; strong FCF generation supports dividends and capex self-funding.

Risks Investors Should Know

- BDL — Earnings risk: FY26 profit fell 23.5%; if execution delays persist in FY27, the stock's ~105x P/E leaves little margin for error.

- HAL — Revenue conversion risk: Rs 2.54 lakh crore order book is impressive but delivery delays on Tejas have happened before; revenue recognition is milestone-based.

- BEL — Valuation risk: 49-54x P/E is premium; any earnings miss or macro-market correction could cause sharp de-rating.

- All three — Single-customer dependency: Ministry of Defence is the dominant or sole customer; policy changes, coalition politics, or fiscal compression are risks.

- HAL — Technology risk: Developing next-generation platforms (AMCA, HLFT-42) involves significant technical and timeline risk.

- BDL — Competition from private sector: Private missile and weapons makers are gaining ground in certain sub-segments.

Valuation Considerations

The three companies present very different valuation profiles in June 2026. HAL, at approximately 36x trailing P/E with the largest order book in Indian defence, may appear relatively more attractively valued than BDL at ~105x — especially given BDL's FY26 earnings contraction. BEL at ~49-54x offers a mid-ground: premium valuation but supported by consistent 15-16% revenue growth and strong order inflows.

Investors should look beyond headline P/E to order-book-to-market-cap ratios, revenue CAGR trends, EBITDA margins, return on equity (ROE), and earnings quality. HAL's order book of Rs 2.54 lakh crore at a market cap of approximately Rs 2.85-3.0 lakh crore implies the order book is roughly 0.85-0.90x market cap — suggesting substantial embedded value if delivery timelines hold. BEL's order book of Rs 73,882 crore at ~Rs 2.97 lakh crore market cap implies ~0.25x — typical for a company with faster revenue conversion.

Dividend History and Shareholder Returns

All three companies are zero-debt PSUs with strong cash generation, enabling consistent dividend payments. HAL paid a total dividend of approximately Rs 40 per share in the past 12 months, with a dividend yield of approximately 0.82% — the highest of the three on an absolute yield basis. BEL recommended a final dividend of Rs 0.55 per share for FY26 plus an interim of Rs 1.95 per share (ex-date March 2026), yielding approximately 0.61-0.64%. BDL paid an interim dividend of Rs 4.50 per share in February 2026 plus a final dividend of Rs 0.40 per share. Verify current dividend announcements on NSE/BSE.

Long-Term Outlook

Over the long term, all three companies are positioned to benefit from India's multi-decade defence modernisation programme. HAL's Rs 2.54 lakh crore order book — if executed on time — implies significant revenue and earnings growth over FY27-FY35, driven by Tejas Mk-1A deliveries, helicopter programmes, AMCA, and MRO growth. BEL's consistent revenue growth trajectory (15-20% guided) and diversified order book make it a relatively lower-risk compounder within the defence space. BDL's strategic importance in missile systems will sustain its relevance, but near-term earnings normalisation from FY26 lows will be critical to justify its current premium valuation.

For long-term investors, a combination of BEL (for earnings consistency and export growth) and HAL (for order book depth and aerospace market position) may offer a balanced approach — subject to individual risk tolerance and portfolio allocation. BDL may be watched for FY27 earnings recovery before re-entry at current valuations. This is not investment advice; please do your own research and consult a SEBI-registered adviser.

Frequently Asked Questions

Q: Which is better — BEL, HAL, or BDL for long-term investment in 2026?

A: Each company suits different investor profiles. BEL offers earnings consistency, portfolio diversification, and export growth. HAL offers unmatched order book depth and aerospace dominance, with moderate near-term growth but exceptional long-term visibility. BDL offers strategic irreplaceability in missile systems but carries FY26 earnings headwinds and a very high P/E of ~105x. The 'best' choice depends on your valuation comfort, investment horizon, and risk appetite. Consult a SEBI-registered adviser.

Q: What is BEL's current order book and what does it mean for investors?

A: BEL's order book stood at Rs 73,882 crore as of April 1, 2026 — approximately 2.5-3 years of revenue coverage at FY26 revenue levels. The company secured fresh orders of approximately Rs 30,000 crore in FY26 alone, indicating strong inflow momentum. This provides meaningful near-term revenue visibility, though order book conversion timelines can vary.

Q: Why did BDL's profit fall so sharply in FY26?

A: BDL's FY26 profit fell 23.5% to Rs 4,203 crore, and Q4 PAT dropped 58.5% YoY. This was attributed to order execution timing (milestone-based revenue recognition), supply chain constraints, and programme delays. BDL's revenue is inherently lumpy — large missile orders are recognised at delivery/milestone milestones rather than smoothly over time. The order book of ~Rs 22,800 crore provides recovery potential in FY27-FY28 if execution resumes. Always verify the latest quarterly results on BSE/NSE.

Q: What is HAL's Tejas Mk-1A programme and why does it matter?

A: The LCA Tejas Mk-1A is India's frontline light combat aircraft, manufactured exclusively by HAL. The Indian Air Force contracted 83 aircraft in 2021 (approximately Rs 48,000 crore) and ordered an additional 97 aircraft subsequently, bringing cumulative contracted value to approximately Rs 1.13 lakh crore across 180 aircraft. Deliveries are targeted to begin August-September 2026. This single programme represents a large portion of HAL's order book and will be a primary revenue and earnings driver for the next 10-12 years.

Q: Do BEL, HAL, and BDL pay dividends?

A: Yes, all three pay dividends regularly. HAL paid approximately Rs 40 per share (yield ~0.82%) in the past 12 months. BEL paid an interim of Rs 1.95 plus a final dividend of Rs 0.55 per share in FY26 (yield ~0.61-0.64%). BDL paid an interim of Rs 4.50 per share in February 2026 plus a final of Rs 0.40 per share. Dividend yields are modest given the high share prices; the primary return driver for these stocks has been capital appreciation. Verify latest dividend data on NSE/BSE.

Q: Are these stocks suitable for a retail investor's long-term portfolio?

A: BEL, HAL, and BDL are among India's most credible long-term investment themes in the industrial and capital-goods space, backed by government ownership, captive order flows, zero debt, and India's multi-decade defence modernisation drive. However, they all trade at premium valuations, and earnings can be lumpy. Retail investors should invest within their risk tolerance, avoid over-concentration, and not invest money they cannot afford to keep invested for 5+ years. Consult a SEBI-registered investment adviser.

Q: What is the NSE symbol and listing status for BEL, HAL, and BDL?

A: All three are listed on both NSE and BSE. NSE symbols: BEL (Bharat Electronics), HAL (Hindustan Aeronautics), BDL (Bharat Dynamics). BSE codes can be found at bseindia.com by searching company names. All are part of the Nifty India Defence index. Live price data is available on NSE India (nseindia.com), BSE India (bseindia.com), and financial platforms like Screener.in and Tickertape.

Conclusion

The BEL vs HAL vs BDL comparison reveals three outstanding but distinctly different defence PSU investment propositions in 2026. BEL stands out for its consistent earnings growth, diversified product base, and accelerating export momentum. HAL commands the investment narrative with its Rs 2.54 lakh crore order book and aerospace monopoly, though near-term revenue growth was modest and execution timelines must be monitored.

BDL holds an irreplaceable strategic position in India's missile systems, but FY26 earnings contraction and a ~105x P/E are genuine concerns that investors should weigh carefully. All three are zero-debt, Navratna PSUs with captive government customers and multi-year order visibility — the building blocks of a strong long-term investment case. Disciplined entry pricing, position sizing, and ongoing monitoring remain essential.