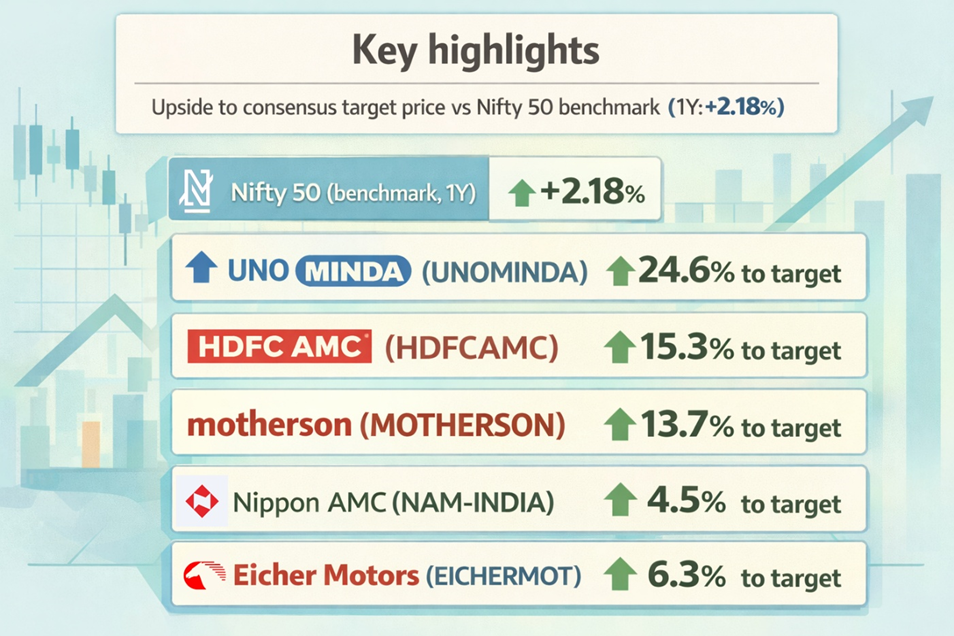

Eicher Motors, Samvardhana Motherson, UNO Minda, Nippon Life India AMC and HDFC Asset Management Company have each attracted unanimous Buy consensus from a combined 108 covering analysts — and each carries upside to target prices that makes the Nifty 50's 2.18 per cent past-year return look like a rounding error.

There is a version of the India growth story that gets told through the headline index. It is a story of 2.18 per cent annual returns, a 52-week range between 22,182 and 26,373, and the slow compression of premium valuations under global macro pressure. For the Nifty 50 investor, the past year has been a lesson in patience — necessary, perhaps, but unrewarding.

Then there is the version that plays out beneath the headline — in niche industrial businesses, premium consumer franchises, and financial services companies that have quietly compounded their revenues, expanded their margins, and rewarded the analysts who maintained conviction through a difficult year for the broader market. Five such companies sit at the centre of this piece: Eicher Motors, Samvardhana Motherson International, UNO Minda, Nippon Life India Asset Management, and HDFC Asset Management Company.

They operate in sectors as different as motorcycle manufacturing, global auto components, wealth management and mutual fund distribution. What they share is this: a unanimous Buy consensus from 108 covering analysts, upside to consensus target prices ranging from 4.5 per cent to 24.5 per cent, and financial metrics — revenue growth, return on equity, return on assets — that the headline index cannot replicate. The data is the argument. It does not require embellishment.

Source: REFINITIV, Analysis by Kalkine Group

Setting the scene — a benchmark that rewards patience but punishes ambition

The Nifty 50's 2.18 per cent return is the return of diversification at its most blunt. It aggregates fifty of India's largest companies, weights them by market capitalisation, and delivers a number that reflects the central tendency of large-cap India. In a year when macro headwinds — a tight global rate environment, rupee pressure, and a sharp selloff in early 2026 that took the index to 22,182 — dominated the sentiment backdrop, that 2.18 per cent is a defensible outcome. It is not, however, a growth outcome.

The five companies examined here have, individually and collectively, delivered a different kind of outcome. Each sits in a structural growth lane: India's premium two-wheeler market, global auto components supply chains, domestic vehicle electrification, and — in what is perhaps the most compelling story in Indian financial services — the asset management industry that is absorbing a generational shift in Indian household savings from physical assets to financial ones. The 108 analysts who cover these five names have reached the same conclusion: Buy.

The average upside to consensus target price across the group is 12.9 per cent — nearly six times the Nifty 50's past-year return. Three of the five have upside above 13 per cent. That is not a statistical artefact of optimistic target-setting; it is the aggregate judgement of institutional research teams who have modelled earnings, discounted cash flows, and compared multiples across global peer groups.

"The five names span motorcycles, auto components, vehicle electrification and mutual fund management — but the data that binds them is identical: unanimous Buy consensus, double-digit revenue growth, and returns on capital that the broader index cannot match."

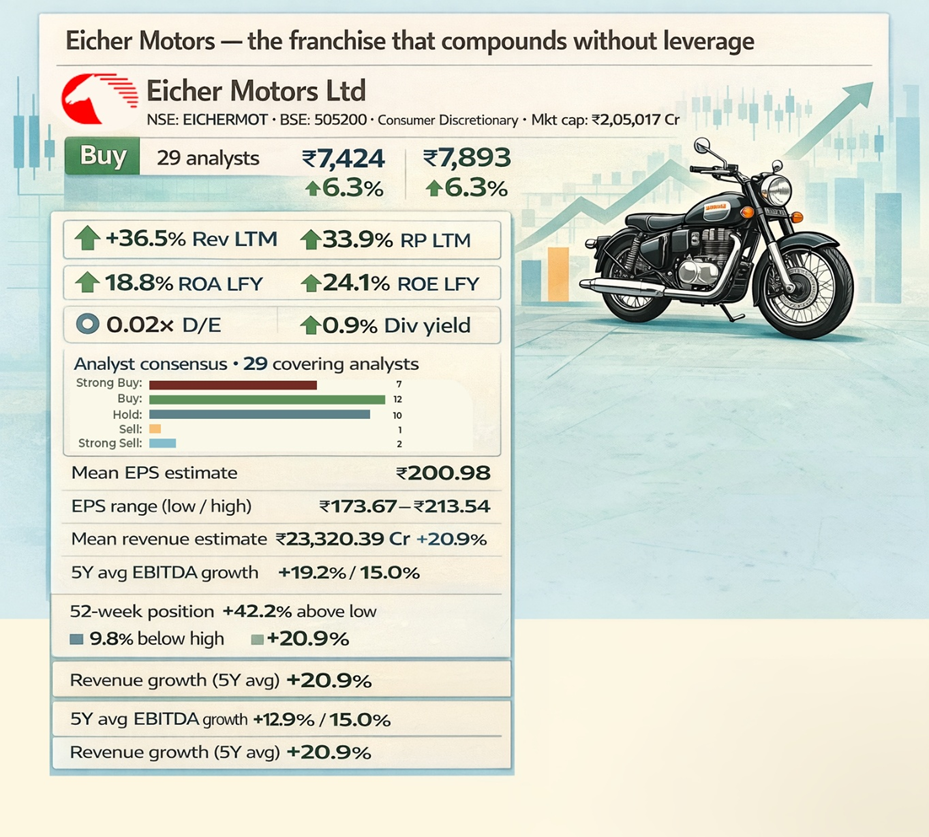

Eicher Motors — the franchise that compounds without leverage

Source: REFINITIV, Analysis by Kalkine Group

Eicher Motors — the parent of Royal Enfield — has constructed one of the most durable consumer franchises in Indian manufacturing: a premium motorcycle brand that commands aspirational pricing in a country where two-wheelers remain the primary personal transport for hundreds of millions. Its financials reflect that franchise strength with unusual clarity.

A debt-to-equity ratio of 0.02× is, for all practical purposes, a debt-free company. The five-year average ROA of 15 per cent means Eicher has been generating fifteen rupees of annual profit for every hundred rupees of assets deployed — a consistency of asset productivity that most Indian manufacturers cannot sustain for a single year, let alone five. The most recent twelve months saw revenue grow 36.5 per cent and net profit expand 33.9 per cent. The five-year average EBITDA growth of 22.9 per cent provides the longer-term anchor: this is not a company having a good year. It is a company with a structural growth engine that has been running consistently.

The analyst distribution is instructive. Ten of the 29 covering analysts rate Eicher a Hold — the highest Hold count in this group — but this should not be read as scepticism about the business. It is scepticism about near-term entry. The consensus target of ₹7,893 against a current price of ₹7,424 implies just 6.3 per cent upside, and the EPS estimate range of ₹173.67 to ₹213.54 is the tightest in proportional terms across the five, reflecting extraordinary analyst confidence in earnings visibility. Quality is not in question. Valuation — at the current level — leaves less room for error than it once did. At 42.2 per cent above its 52-week low and only 9.8 per cent below its 52-week high, the stock is in the later stages of a recovery that has already done most of its work.

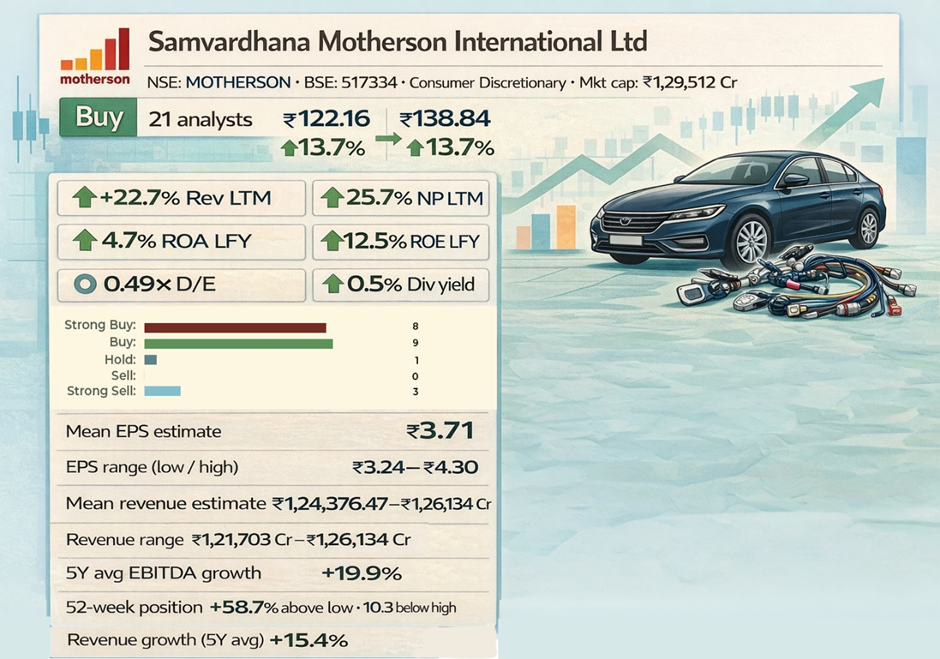

Samvardhana Motherson — global scale, margin recovery, and a debt story in transition

Source: REFINITIV, Analysis by Kalkine Group

Samvardhana Motherson International is the most globally dispersed business in this group — a sprawling auto components conglomerate with manufacturing operations across multiple continents, supplying wiring harnesses, vision systems, polymer components, and interior modules to the world's major vehicle manufacturers. Every car on every road in every developed market almost certainly contains a Motherson component somewhere in its architecture. The forward revenue base of ₹1.24 lakh crore places it among the largest Indian-listed manufacturers by turnover.

The 0.49× debt-to-equity ratio is the highest in this group and the one number that separates Motherson from the capital fortresses that Eicher and the two asset managers have constructed. That leverage is the legacy of an acquisition-driven expansion strategy that transformed the company from a single-customer supplier in the 1990s into a global Tier-1 conglomerate. The strategic logic was sound; the execution has been uneven at times, and the three Strong Sell ratings among 21 analysts — the only material Strong Sell count in this group — reflect residual concerns about currency exposure from global operations and the margin pressure that follows automotive production cycles.

Yet the recovery data is compelling. At 58.7 per cent above its 52-week low — the largest proportional recovery move of all five stocks — the market has clearly begun repricing. Revenue growth of 22.7 per cent and net profit growth of 25.7 per cent last twelve months — profit growing faster than revenue, which is the operating leverage signature of a business improving its cost structure — validate the bull thesis. The forward revenue estimate range of ₹1,21,703 crore to ₹1,26,134 crore is exceptionally tight for a company of this size and geographic complexity, indicating analysts have high confidence in the top-line visibility. The 13.7 per cent upside to consensus target is the second-highest in the group after UNO Minda.

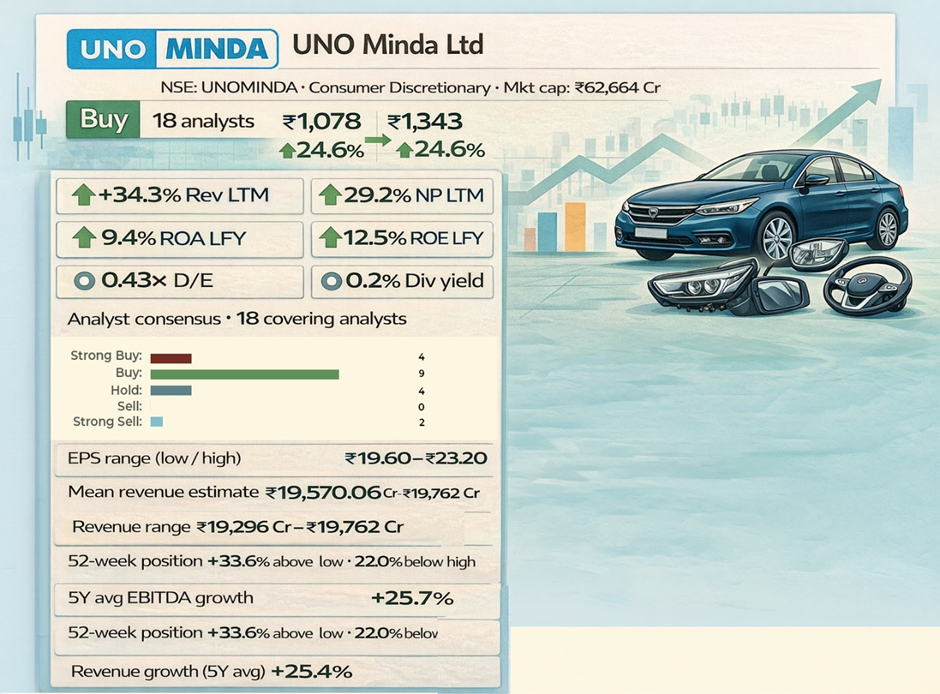

UNO Minda — the auto components company with the clearest upside

UNO Minda presents the most compelling near-term upside case in this group. The consensus target of ₹1,343.32 against a current price of ₹1,078 implies 24.6 per cent appreciation — the highest of the five — and it comes from a coverage base of 18 analysts with zero Sell ratings. The stock sits 33.6 per cent above its 52-week low but still 22 per cent below its 52-week high, suggesting a recovery in progress that the market has not yet completed pricing.

UNO Minda is a leading Indian auto components manufacturer, supplying switches, lighting systems, acoustic products, and increasingly, electrification-related components for two and four-wheelers. Its positioning at the intersection of conventional auto components and EV-enabling technology makes it a dual beneficiary: it continues to earn from the existing internal combustion vehicle fleet while growing its EV-specific component portfolio as India's automotive transition accelerates.

Revenue growth of 34.3 per cent last twelve months — the second highest in this group after Nippon AMC — and net profit growth of 29.2 per cent demonstrate that top-line expansion is translating to the bottom line with reasonable efficiency. The five-year average EBITDA growth of 25.7 per cent and revenue CAGR of 25.4 per cent confirm this is not a one-year phenomenon. ROE of 17.7 per cent and ROA of 9.4 per cent are respectable for a capital-intensive auto components business, and the 0.43× D/E — while elevated relative to Eicher or the two AMCs — reflects investment in capacity to support the EV transition rather than financial engineering. The EPS estimate range of ₹19.60 to ₹23.20 is narrow and the forward revenue range of ₹19,296 crore to ₹19,762 crore is among the tightest in the group, pointing to high analyst confidence in near-term earnings delivery.

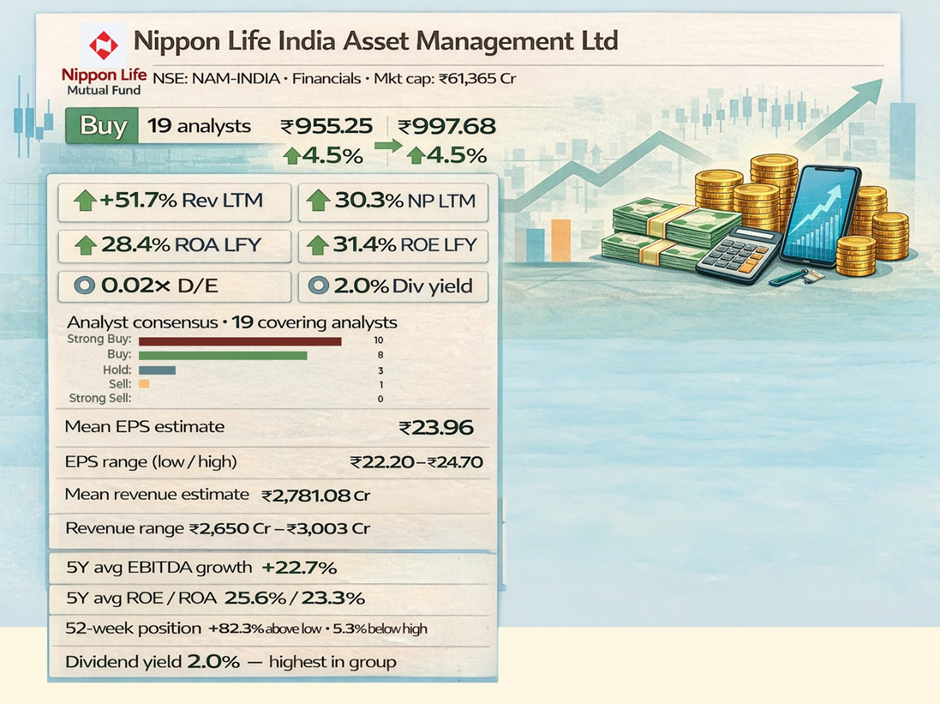

Nippon Life India AMC — the pure-play on India's mutual fund revolution

Source: REFINITIV, Analysis by Kalkine Group

Nippon Life India Asset Management holds a distinction that no other stock in this group can claim: it is 82.3 per cent above its 52-week low — the most dramatic price recovery of the five — and yet it sits only 5.3 per cent below its 52-week high. In practical terms, the stock has almost fully recovered to its peak while the Nifty 50 remains mired 10 per cent below its own high-water mark. That divergence is the mutual fund industry in microcosm.

India's asset management industry is undergoing a structural transformation that has few parallels in emerging market financial history. Systematic Investment Plan contributions — monthly instalments into equity mutual funds, drawn directly from bank accounts — have become the savings vehicle of choice for India's expanding middle class. Monthly SIP flows into Indian mutual funds have grown from negligible levels a decade ago to consistent monthly records. Nippon Life AMC, as one of India's largest and most recognised fund managers, is a direct beneficiary of every new SIP account opened.

The numbers reflect this structural tailwind with striking clarity. Revenue growth of 51.7 per cent last twelve months — the highest in this group — is not the output of a cyclical upturn. It is fee income expanding proportionally with AUM, which expands as markets rise and as net inflows compound. ROE of 31.4 per cent and ROA of 28.4 per cent are exceptional for any financial services business and reflect the asset-light, fee-based nature of fund management: Nippon manages money, earns a percentage of AUM as fee income, and deploys minimal capital of its own in the process. The 0.02× D/E confirms the capital structure is pristine. The 2.0 per cent dividend yield — the highest in this group — signals that the business generates more cash than it needs to reinvest, and management is returning it to shareholders. Ten of 19 covering analysts rate it a Strong Buy.

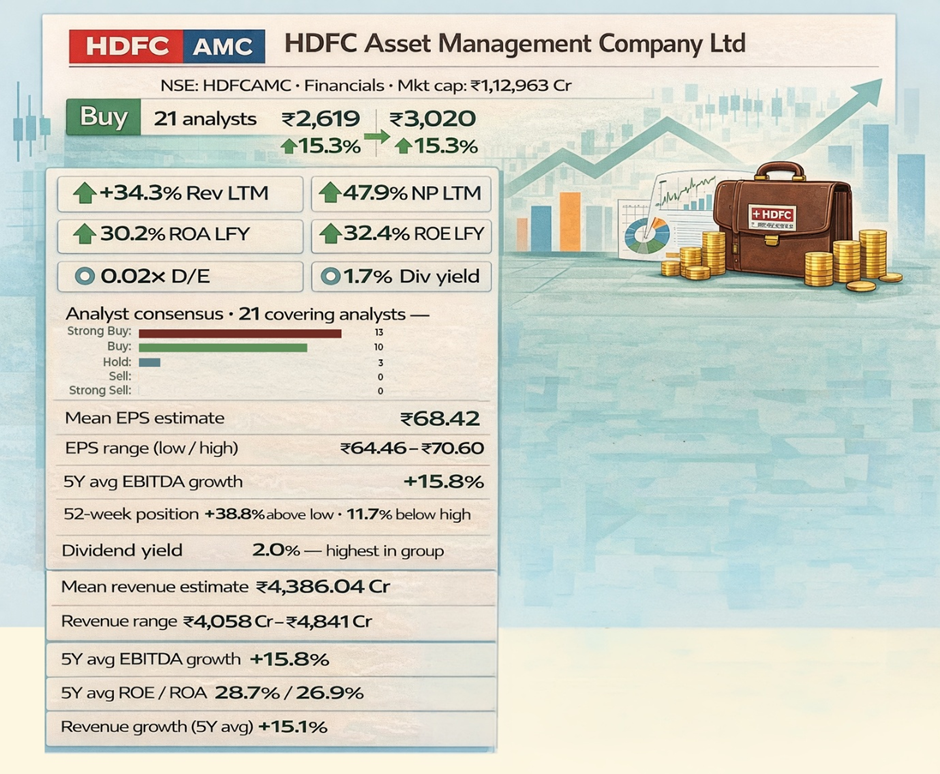

HDFC AMC — the industry leader with the most explosive profit growth

Source: REFINITIV, Analysis by Kalkine Group

HDFC Asset Management Company is the undisputed market leader of India's mutual fund industry by AUM and among the most recognised financial brands in the country. Its analyst rating distribution is the cleanest in this entire group: 13 Strong Buy and 10 Buy ratings among 21 covering analysts, with zero Sell and zero Strong Sell recommendations. Not a single analyst who covers HDFC AMC thinks investors should exit. That kind of unanimity — at a market capitalisation of ₹1.13 lakh crore — is remarkable.

The financial case is equally compelling. Net profit growth of 47.9 per cent last twelve months — the highest NP growth rate in this group — accompanied revenue growth of 26.8 per cent, which means margins are expanding. When profit grows faster than revenue, it signals operating leverage: fixed cost bases being spread across growing AUM and fee income. ROE of 32.4 per cent and ROA of 30.2 per cent are exceptional figures for any company in any sector, and the five-year averages — ROE 28.7 per cent, ROA 26.9 per cent — confirm this is not a one-year aberration. The D/E of 0.02× mirrors Eicher and Nippon AMC: a business that has chosen not to lever its balance sheet because it does not need to.

The consensus target of ₹3,020.40 against the current ₹2,619.30 implies 15.3 per cent upside — the second-highest in the group. The EPS estimate range of ₹64.46 to ₹70.60 is tight, reflecting high analyst certainty about forward earnings. The 1.7 per cent dividend yield adds an income component to what is primarily a growth story. At 38.8 per cent above its 52-week low and 11.7 per cent below its 52-week high, HDFC AMC has recovered meaningfully but has not yet closed the gap to its peak — creating the kind of entry dynamic that its 21 covering analysts are evidently still backing with conviction.

"The two AMCs in this group — HDFC AMC and Nippon Life AMC — carry the highest returns on equity and assets of all five stocks, zero meaningful debt, growing dividends, and the structural tailwind of a generational shift in Indian household savings. They are not financials stocks. They are toll roads on India's wealth creation."

What the data tells us — and what it does not

Five companies, two sectors, 108 analysts, and a unanimous Buy. Taken together, these names represent ₹5.72 lakh crore of combined market capitalisation — a significant slice of India's institutional equity universe — and they paint a coherent picture of where the country's structural growth is currently concentrated.

The auto components cluster — Eicher, Motherson, UNO Minda — reflects India's position as both the world's largest two-wheeler market and a growing global supplier of automotive parts. The EV transition adds a layer of complexity: Motherson and UNO Minda are both building out EV-related product lines while continuing to serve the enormous installed base of internal combustion vehicles. The transition is neither fast enough to disrupt existing revenue streams in the near term nor slow enough to be ignored in five-year planning. The financial metrics — particularly UNO Minda's 25.4 per cent five-year revenue CAGR — suggest the market has been pricing in a successful navigation of that transition.

The asset management pair — HDFC AMC and Nippon Life AMC — represent a different kind of structural argument. India's mutual fund industry AUM has grown from approximately ₹10 lakh crore a decade ago to multiples of that figure today, driven by rising financial literacy, the proliferation of direct investment platforms, and the normalisation of SIP investing as the savings default for India's professional class. Both AMCs carry ROE above 28 per cent, near-zero debt, and dividend yields above 1.5 per cent — the profile of mature, cash-generative businesses in a market that is still in early-to-mid innings of its growth arc.

The common risk across all five is valuation. None of these stocks is cheap in absolute terms; all trade at premiums to historical averages that embed meaningful growth expectations. The analyst consensus is uniformly positive, but consensus can be wrong — particularly when macro shocks (a sharp rupee depreciation, a global slowdown in auto demand, a correction in Indian equity markets that compresses AUM) arrive with the speed and force that the last twelve months have demonstrated is always possible. The 4.5 per cent upside to target in Nippon AMC — the narrowest of the five — suggests at least some of the AMC story is already well-recognised. The 24.6 per cent upside in UNO Minda suggests it is not.