📌 Key Highlights

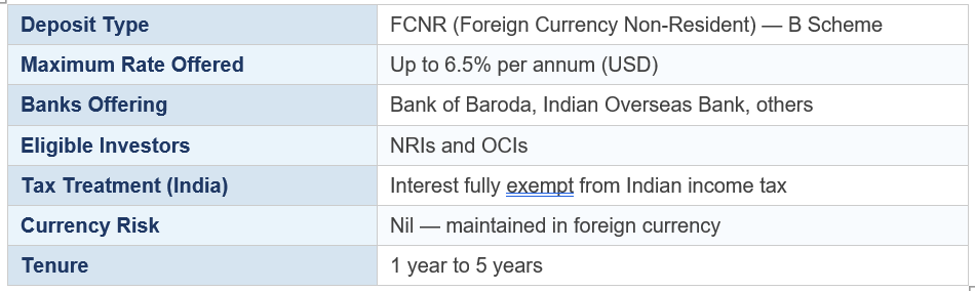

- Multiple Indian banks launching new FCNR (B) USD deposit schemes offering up to 6.5% interest

- Bank of Baroda and Indian Overseas Bank among the banks offering these enhanced rates

- FCNR(B) deposits are maintained in foreign currency — fully exempt from currency risk for depositors

- Interest income and principal in FCNR(B) deposits are fully exempt from Indian income tax

- Designed to attract NRI and OCI remittances into India amid global interest rate environment

- Minimum tenure: 1 year; maximum: 5 years

- Currency options: USD, GBP, EUR, CAD, AUD, JPY

📋 Quick Facts

📰 The Story

In a coordinated effort to attract foreign remittances and shore up India's foreign exchange reserves, multiple Indian banks — including Bank of Baroda and Indian Overseas Bank — have launched enhanced Foreign Currency Non-Resident (FCNR-B) deposit schemes for NRIs and OCIs, offering interest rates of up to 6.5% per annum on US dollar deposits.

The FCNR(B) scheme allows non-resident Indians and Overseas Citizens of India to maintain fixed deposits in foreign currencies with Indian banks. Unlike NRE accounts (which are rupee-denominated), FCNR(B) deposits carry no currency conversion risk for the depositor — funds are accepted in foreign currency and repaid in the same currency at maturity. Both principal and interest are fully repatriable.

The timing of these new offerings is strategic. Global interest rates have been elevated through 2025-26 as Western central banks maintained restrictive monetary policy to control post-pandemic inflation. With the US Federal Reserve's federal funds rate in the 4.5-5% range, Indian banks offering 6.5% on USD FCNR deposits are providing a meaningful spread over US money market rates — while offering the security of deposits with regulated Indian public sector banks.

For the Reserve Bank of India and the government, higher FCNR deposit inflows serve multiple macroeconomic objectives: they replenish forex reserves, provide dollar liquidity to the banking system, and help stabilise the rupee against the dollar. India's forex reserves have been well-maintained at over USD 680 billion, but increased FCNR inflows add another layer of external sector resilience.

The FCNR(B) scheme has historically been used as a policy tool during periods of rupee stress — the RBI and government have previously offered interest rate concessions to banks specifically to attract FCNR deposits (notably in 2013 and 2018). The current rate enhancement is a market-driven response to the global rate environment rather than a crisis measure, reflecting the healthy state of India's external balance sheet.

For eligible NRIs and OCIs, the combination of 6.5% USD returns, zero Indian income tax, full repatriability, and the security of deposits with regulated Indian banks makes FCNR(B) deposits a compelling fixed income option — particularly for those with future INR obligations (property purchases, family remittances, or retirement plans in India).

📊 Financial Analysis

The 6.5% USD FCNR rate compares favourably with US Treasury yields (5-year UST at approximately 4.5-4.8%) and even some US bank CD rates. The Indian tax exemption adds approximately 30-35% effective yield enhancement for NRIs in high-tax jurisdictions, making the after-tax comparison even more attractive.

For Indian banks, FCNR deposits provide relatively stable, tenure-matched foreign currency funding — useful for banks with dollar loan books (project finance, ECBs) or those seeking to diversify their funding base. The cost of these deposits is slightly higher than inter-bank rates but comes with less rollover risk and no margin call exposure.

One consideration for investors: FCNR deposits are subject to swap costs if banks choose to convert the foreign currency funding into rupees. Banks with genuine dollar lending needs benefit most from FCNR inflows; those converting to INR incur hedging costs that compress the net benefit.

💹 Investor Insights

For NRI investors evaluating FCNR deposits, the key comparison benchmarks are: US Treasuries (4.5-4.8% for 5-year), US high-grade corporate bonds (5.5-6.0%), and US bank CDs (4.8-5.5%). At 6.5%, Indian FCNR deposits offer a competitive spread with the added benefit of Indian income tax exemption.

Risk considerations: Indian bank credit risk (mitigated by government ownership for PSU banks), regulatory risk (RBI policy changes on FCNR rates), and geopolitical/country risk. For most conservative NRI fixed-income investors, FCNR deposits at leading PSU banks represent an attractive risk-reward at current rates.

Frequently Asked Questions (FAQs)

- What is the difference between FCNR and NRE deposits?

- NRE deposits are maintained in Indian rupees — the foreign currency remitted by the NRI is converted to INR. FCNR(B) deposits are maintained in the original foreign currency (USD, GBP, etc.), eliminating currency risk for the depositor. Both are tax-free in India; FCNR is preferable for those who want to avoid INR depreciation risk.

- Is 6.5% on USD FCNR deposits guaranteed?

- The rate is fixed at the time of deposit for the chosen tenure — so it is guaranteed for the period you commit to. However, rates offered for new deposits may change. The 6.5% is the top-of-range currently being offered; actual rates depend on the specific bank, tenure, and currency.

- Can resident Indians invest in FCNR deposits?

- No. FCNR(B) deposits are exclusively for Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs). Resident Indians cannot open or maintain FCNR accounts.

- What happens to FCNR deposits if the investor returns to India?

- Upon returning to India and changing residential status to 'Resident', FCNR deposits continue until maturity but can no longer be renewed as FCNR. At maturity, funds can be converted to Resident Foreign Currency (RFC) accounts, which also offer some tax benefits.