Why Institutional Holdings Matter

Before examining the five companies, it is worth establishing why the convergence of high FII and DII ownership in the same stock is analytically meaningful.

Foreign institutional investors — global asset managers, sovereign wealth funds, hedge funds, and pension pools — conduct rigorous cross-country capital allocation analysis. Their decision to hold meaningful positions in an Indian stock reflects a conviction that this company, priced at current levels, offers superior risk-adjusted returns relative to competing opportunities across emerging and developed markets worldwide.

Domestic institutional investors — Indian mutual funds, insurance companies, and provident fund managers — bring deep knowledge of local regulatory environments, management quality, and sector dynamics. Their accumulation of a stock reflects a long-duration view on the company's fundamental trajectory within the Indian economic context.

When both cohorts — with different mandates, different analytical frameworks, and different information advantages — arrive at the same company simultaneously, the overlap is not coincidental. It is a signal worth examining carefully.

The five stocks below each carry combined FII and DII holdings that place them in the top tier of institutionally owned Indian equities. What follows is an analysis of why.

- Delhivery Ltd (NSE:DELHIVERY)

Data Source: REFINITIV, Analysis: Kalkine Group

Why Institutions Own This Stock

Delhivery carries the highest combined institutional ownership of any stock in this screen — 83.55% of the company is held by foreign and domestic institutions combined. This is an extraordinary concentration and requires explanation, because on conventional metrics, Delhivery does not immediately present as a compelling buy: ROCE of 2.47% is negligible, P/E of 173x reflects almost no near-term earnings power, and the company has only recently begun generating positive quarterly profits.

The institutional thesis for Delhivery is not a value argument. It is an infrastructure argument.

India's logistics sector is structurally fragmented, chronically under-invested, and sitting at the intersection of the country's two most powerful long-duration tailwinds: e-commerce penetration growth and the formalisation of supply chains driven by GST compliance requirements. Delhivery, as the country's largest fully-integrated logistics network — spanning express parcel delivery, freight, cross-border logistics, and supply chain management — is positioned to be the default infrastructure provider for India's commercial economy as it digitises.

The quarterly profit growth of +167.51% is the number that institutions are watching most carefully. Delhivery's path to value is through operating leverage: as volumes grow across a fixed (or slowly growing) network infrastructure, incremental revenue drops to the bottom line at dramatically higher margins than the blended average. The direction of travel on profitability — from significant losses to positive territory — is what the 48.57% FII holding and 34.98% DII holding are pricing in.

Key monitoring metric: ROCE recovery trajectory. For the institutional thesis to be validated, ROCE must demonstrate consistent improvement from its current 2.47% base as volume growth drives operating leverage across the network.

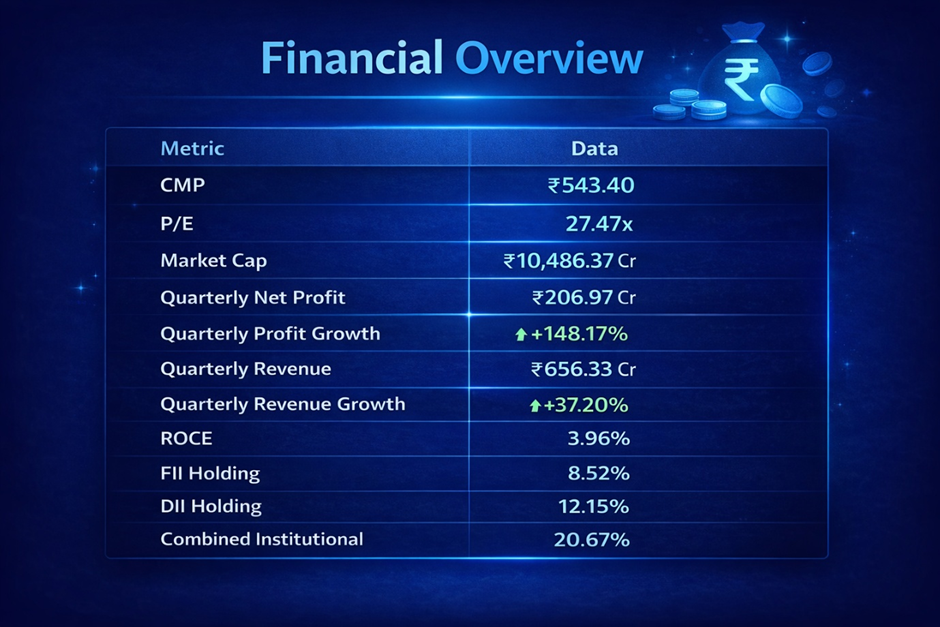

- HEG Ltd (NSE:HEG)

Data Source: REFINITIV, Analysis: Kalkine Group

Why Institutions Own This Stock

HEG is one of the world's largest manufacturers of graphite electrodes — a product that sounds unglamorous until you understand what it does and why its demand dynamics are among the most structurally interesting in the industrial materials space.

Graphite electrodes are the critical consumable in electric arc furnace (EAF) steelmaking — the process by which steel scrap is melted and refined into usable steel. EAF steelmaking is the most energy-efficient and lowest-emission method of producing steel, and its global adoption is accelerating as steelmakers in Europe, North America, and increasingly India invest in decarbonisation of their production processes. Every percentage point of market share that EAF gains over blast furnace steelmaking translates directly into incremental graphite electrode demand.

HEG operates at the premium end of this market — ultra-high power (UHP) graphite electrodes for large EAF furnaces — and holds one of the largest single-site manufacturing capacities globally at its Mandideep facility in Madhya Pradesh. It also benefits from integration into needle coke supply, the primary raw material for electrode production, through its relationship with the Bhilwara Group.

The quarterly metrics tell a compelling near-term story: profit growth of +148.17% and revenue growth of +37.20% reflect the cyclical upswing in graphite electrode pricing that follows periods of supply rationalisation. The ROCE of 3.96% appears low but is a cyclical trough figure — HEG's ROCE has historically reached 40%+ at peak cycle pricing.

The combined 20.67% institutional holding reflects confidence in both the near-term earnings recovery and the long-duration EAF steelmaking thesis.

Key monitoring metric: Global graphite electrode pricing and EAF steel capacity announcements in Europe and the US. These are the primary drivers of HEG's earnings cycle and the variables that will most directly influence institutional position sizing.

- Tata Chemicals Ltd (NSE: TATACHEM)

Data Source: REFINITIV, Analysis: Kalkine Group

Why Institutions Own This Stock

Tata Chemicals presents the most analytically nuanced case in this screen. On current reported metrics — a quarterly net loss of ₹69 Cr, ROCE of 3.96%, and declining revenue — the company does not fit the conventional institutional quality template. Yet 34.66% of the company is held by sophisticated FII and DII investors. Understanding why requires looking past the near-term P&L.

Tata Chemicals operates across three distinct business verticals that carry fundamentally different margin and growth profiles. The legacy basic chemistry business — soda ash production in India, Kenya, and the United Kingdom — is a mature, cyclically sensitive operation whose current weakness largely explains the earnings softness. Soda ash prices have normalised from post-COVID highs, and the UK operations in particular have faced energy cost and demand headwinds.

The second vertical is specialty chemicals — including silica for tyres and other industrial applications — which carries higher margins and is growing, though not yet large enough to offset the basic chemistry pressure.

The third — and the one that most directly explains the institutional ownership — is the emerging battery chemicals and sodium ion battery materials business. Tata Chemicals has identified lithium-ion battery materials and next-generation sodium-ion battery precursors as a strategic growth vector, investing in R&D and production capability that aligns with both India’s EV adoption curve and the group’s broader Tata Motors EV strategy. The potential for Tata Chemicals to become an internal supplier of battery-critical materials to Tata’s automotive and energy storage businesses is a vertical integration story that institutional investors with long investment horizons are willing to hold through near-term P&L weakness to access.

The Tata Group parentage itself is a factor. The governance credibility, access to group capital, and strategic alignment that comes with Tata stewardship provides institutional investors with a risk floor that a standalone chemicals company of equivalent earnings quality would not offer.

Key monitoring metric: Battery materials revenue contribution and soda ash price cycle recovery. The former is the long-duration growth driver; the latter is the near-term earnings normalisation catalyst.

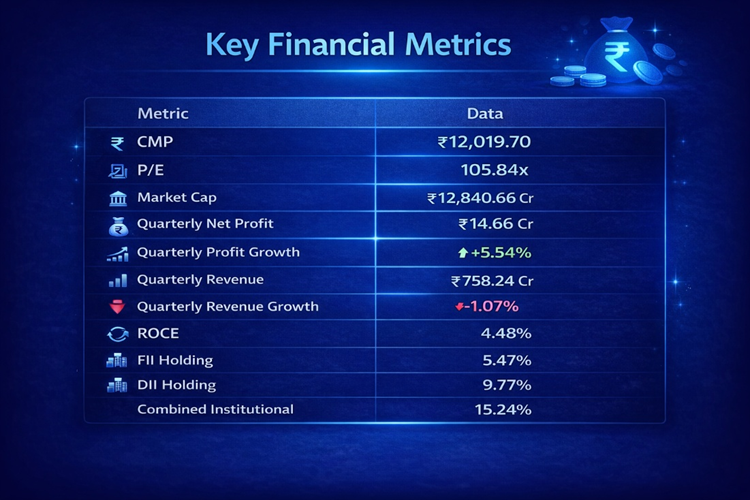

4.Lakshmi Machine Works (NSE: LMW)

Data Source: REFINITIV, Analysis: Kalkine Group

Why Institutions Own This Stock

LMW is one of India's’oldest and most respected capital goods manufacturers, producing textile machinery — spinning machines, ring frames, roving frames — that supply India's’cotton and man-made fibre textile industry. It also has a machine tools division and an aerospace components manufacturing business, the latter being of growing strategic significance.

At first glance, the current metrics are not compelling. A 105.84x P/E on modest quarterly earnings, declining revenue of -1.07%, and ROCE of 4.48% represent a stock whose current earnings power does not justify its valuation by conventional standards. Institutional investors holding 15.24% combined are clearly not buying the current P&L.

They are buying three things that the current P&L does not reflect.

First, the textile machinery replacement cycle. India's’textile industry is undergoing a capital expenditure upcycle as manufacturers modernise ageing spindle infrastructure to compete with Bangladesh and Vietnam on quality and productivity. LMW, as the dominant domestic textile machinery supplier, is the primary domestic beneficiary of that cycle whenever it fully activates.

Second, the aerospace components business. LMW has built an aerospace precision components manufacturing capability — supplying both domestic defence programmes and international aerospace OEMs — that is structurally different from the cyclical textile machinery business. This business carries higher margins, longer-duration contracts, and strategic importance that the market has not yet fully priced relative to its potential scale.

Third, the balance sheet. LMW has historically maintained a virtually debt-free balance sheet with significant cash reserves — a quality that institutions value as a risk buffer during the troughs of the textile machinery cycle and as optionality for strategic acquisitions or capacity expansion when the cycle turns.

The combined institutional holding of 15.24% reflects long-duration conviction in these structural factors rather than near-term earnings enthusiasm.

Key monitoring metric: Order book announcements from the textile machinery division and aerospace components revenue growth. The former signals cycle activation; the latter signals business mix improvement toward higher-margin work.

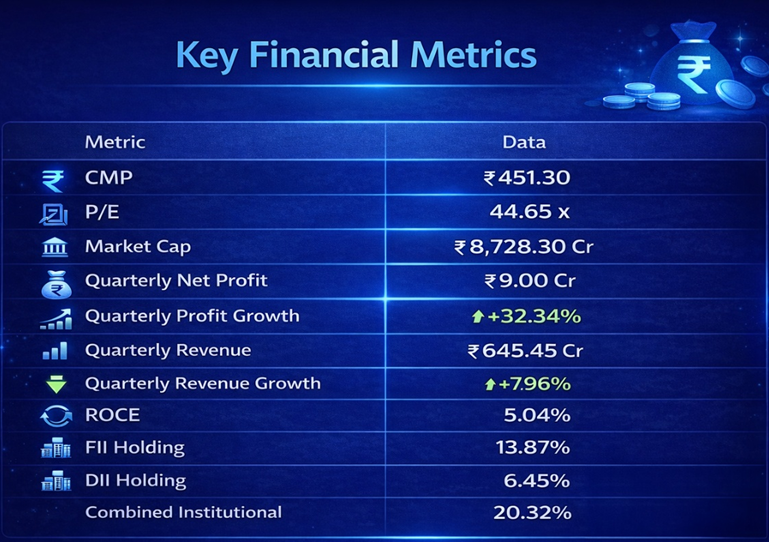

- Eureka Forbes Ltd (NSE: EUREKAFORBES)

Data Source: REFINITIV, Analysis: Kalkine Group

Why Institutions Own This Stock

Eureka Forbes is the company behind India's most recognised water purification brand — Aquaguard — and a leading player in the vacuum cleaner and home security segments. The brand has been a fixture in Indian middle-class homes for over four decades, generating the kind of deep consumer recognition that takes generations to build and is nearly impossible to purchase through advertising spend alone.

The institutional ownership of 20.32% is a bet on the intersection of three powerful forces in India's consumer economy.

The first is water quality. India's drinking water quality challenge is both chronic and worsening across urban and peri-urban geographies. Consumer awareness of waterborne health risks is rising, and the transition from unfiltered municipal supply to point-of-use purification is a one-way demographic journey — households that adopt water purifiers almost never revert. The total addressable market for residential water purification in India remains significantly underpenetrated relative to the installed base that income levels and health awareness would suggest it should be.

The second is the shift from product sales to service revenue. Eureka Forbes' Annual Maintenance Contract (AMC) business — recurring service contracts on installed Aquaguard units — generates revenue and margins that are structurally superior to one-time product sales. As the installed base grows, AMC revenue grows with it on a largely predictable, recurring basis. Institutions assign premium multiples to businesses with this kind of embedded revenue architecture.

The third is the post-Shapoorji Pallonji restructuring. Eureka Forbes was separated from the Shapoorji Pallonji Group and listed as a standalone entity, creating a cleaner corporate structure and the management focus that a previously diversified conglomerate context had historically obscured. The Advent International private equity backing prior to listing introduced operational discipline and strategic clarity that has positioned the company to execute on its market leadership more effectively than it had in prior decades.

Key monitoring metric: AMC revenue as a proportion of total revenue and net profit margin trajectory. These two metrics together determine whether Eureka Forbes is successfully monetising its installed base and translating revenue growth into earnings.

Comparative Summary

Data Source: REFINITIV, Analysis: Kalkine Group

The Common Thread

Across five companies in five completely different industries — logistics, industrial materials, chemicals, capital goods, and consumer products — the institutional ownership thesis converges on a single analytical principle: these are businesses where the current reported earnings understate the normalised or future earnings power by a wide margin, and where institutional investors with long investment horizons and genuine analytical resources have concluded that the gap between current price and intrinsic value is wide enough to justify patient accumulation.

None of these are cheap on trailing P/E. All of them are owned by the most sophisticated capital allocators in global and domestic markets. That combination — apparent expensiveness on surface metrics combined with deep institutional conviction — is frequently where the most durable long-term investment opportunities reside.