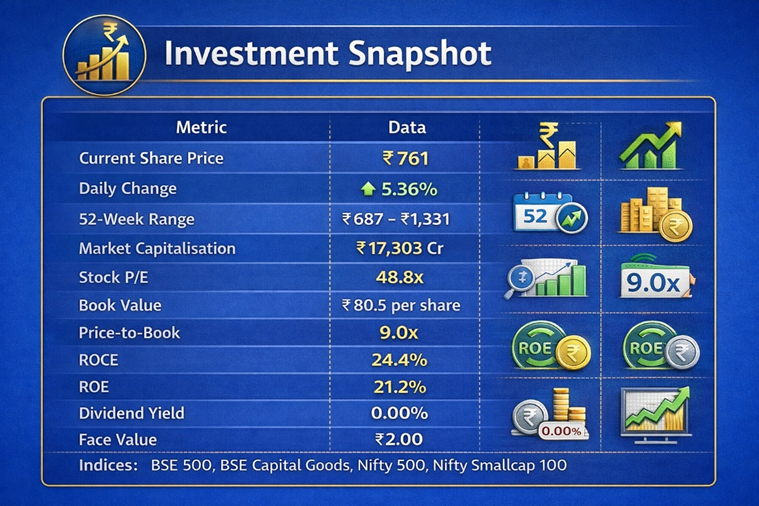

- Investment Snapshot

Data Source: REFINITIV, Analysis: Kalkine Group

- Company Overview

Jyoti CNC Automation Ltd is India's leading manufacturer of simultaneous 5-axis CNC (Computer Numerical Control) machine tools, commanding a domestic market share of approximately 10–12%. The company designs and manufactures precision metal-cutting machines for a diverse set of high-value end markets including Aerospace, Defence, Automotive Components, and General Engineering.

Jyoti CNC's manufacturing operations span both India and Europe, with the company having acquired Huron Graffenstaden, a French CNC machine tool manufacturer, giving it a foothold in the technically demanding European industrial market. This dual geographic presence differentiates Jyoti from purely domestic Indian capital goods peers and underpins its claim to global-standard manufacturing capability.

The company's strategic relevance has increased materially in recent years, driven by India's push for defence indigenisation, expansion of the aerospace supply chain, and broader capital goods capacity creation aligned with the "Make in India" initiative. CNC machine tools are a foundational input for precision manufacturing, and Jyoti's 5-axis capability — which enables complex, multi-plane machining in a single setup — positions it at the high-value end of the market.

- Financial Performance Analysis

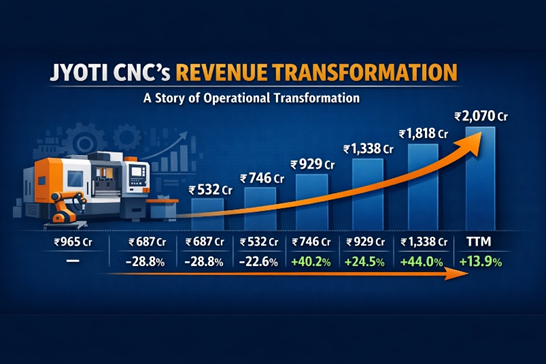

3.1 Revenue Growth — Sustained and Accelerating

Jyoti CNC's revenue trajectory over the past several years tells the story of a company that has undergone a genuine operational transformation.

Data Source: REFINITIV, Analysis: Kalkine Group

The COVID-period contraction in FY2020–FY2021 was sharp but cyclical. The recovery from FY2022 onward has been exceptional — a 3-year revenue CAGR of 35% and a 5-year CAGR of 21% reflect both market share consolidation and the structural tailwind from India's defence and aerospace capacity buildout. Trailing twelve-month revenue of ₹2,070 Cr annualises the company at a scale that is beginning to warrant more serious institutional attention.

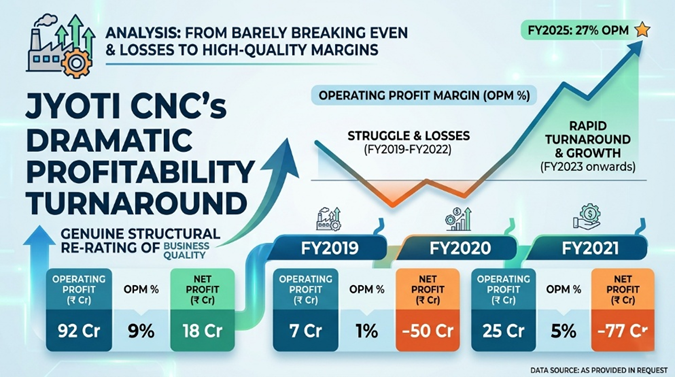

3.2 Profitability Transformation — The Margin Story

The most analytically compelling aspect of Jyoti CNC's recent history is the dramatic improvement in operating profitability. The company went from barely breaking even in FY2019 (OPM of 9%) and suffering losses through FY2022, to delivering an operating profit margin of 27% in FY2025 — a genuine structural re-rating of the business quality.

Data Source: REFINITIV, Analysis: Kalkine Group

The inflection occurred decisively in FY2024, when the company reported its first meaningful net profit following five consecutive years of losses or near-breakeven performance. The improvement is attributable to a combination of operating leverage on higher revenue, improved product mix toward higher-value 5-axis machines, and a significant reduction in interest costs following debt repayment (borrowings fell from ₹835 Cr in FY2023 to ₹304 Cr in FY2024 before re-expanding to ₹497 Cr in FY2025).

The quarterly trend confirms the margin improvement is structural rather than one-off: OPM has remained in the 24–31% range across every quarter from Dec 2023 through Dec 2025, suggesting a durable shift in the business's earning power.

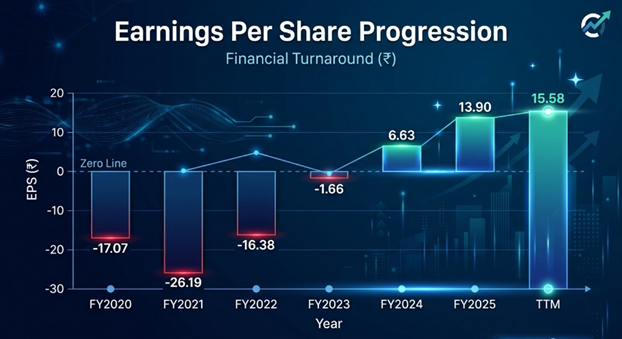

3.3 Earnings Per Share Progression

Data Source: REFINITIV, Analysis: Kalkine Group

The EPS trajectory from deeply negative through FY2021 to ₹15.58 TTM is a textbook earnings recovery story. The 5-year net profit CAGR of 42.8% (which includes the loss years in the base) reflects the magnitude of the turnaround. The 3-year profit CAGR of 105% is even more striking, capturing the acceleration phase of the recovery.

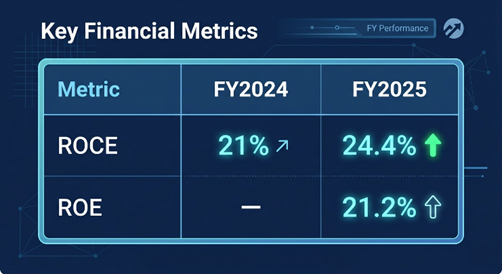

3.4 Return Metrics

Data Source: REFINITIV, Analysis: Kalkine Group

Both ROCE and ROE have improved substantially and now sit at levels that indicate efficient capital deployment. A ROCE of 24.4% — substantially above the cost of capital — is the hallmark of a business with genuine competitive advantages and pricing power. The trend direction (improving) is as important as the absolute level.

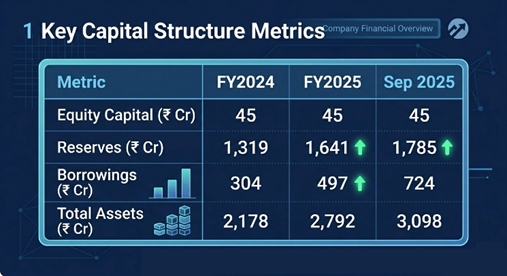

- Balance Sheet & Working Capital Analysis

Data Source: REFINITIV, Analysis: Kalkine Group

The balance sheet has strengthened materially through FY2024–FY2025, primarily due to the large equity raise completed in FY2024 that replenished reserves and enabled significant debt reduction. However, borrowings have since re-expanded from ₹304 Cr in FY2024 to ₹724 Cr by September 2025 — a trend that warrants monitoring. This increase likely reflects working capital requirements associated with a significantly larger order book and revenue run-rate, but the pace of debt re-accumulation should be tracked against cash generation.

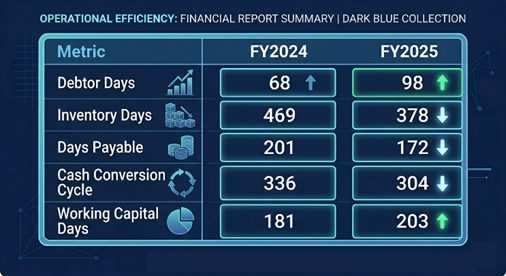

4.2 Working Capital — A Key Risk Area

The working capital dynamics represent the most significant analytical concern in Jyoti CNC's’financial profile.

Data Source: REFINITIV, Analysis: Kalkine Group

Working capital days have increased from 112 days (earlier period) to 203 days in FY2025 — a substantial deterioration. Debtor days have risen from 74 to 98 days, indicating slower collections from customers. While inventory days have improved from 469 to 378 days (reflecting better operational efficiency), the net working capital position has worsened considerably.

This is a critical metric for a manufacturing business. Long-dated receivables and high working capital requirements consume cash even as the business grows profitably — which explains why cash from operating activity has turned negative (-₹105 Cr in FY2025) despite reported net profits of ₹316 Cr.

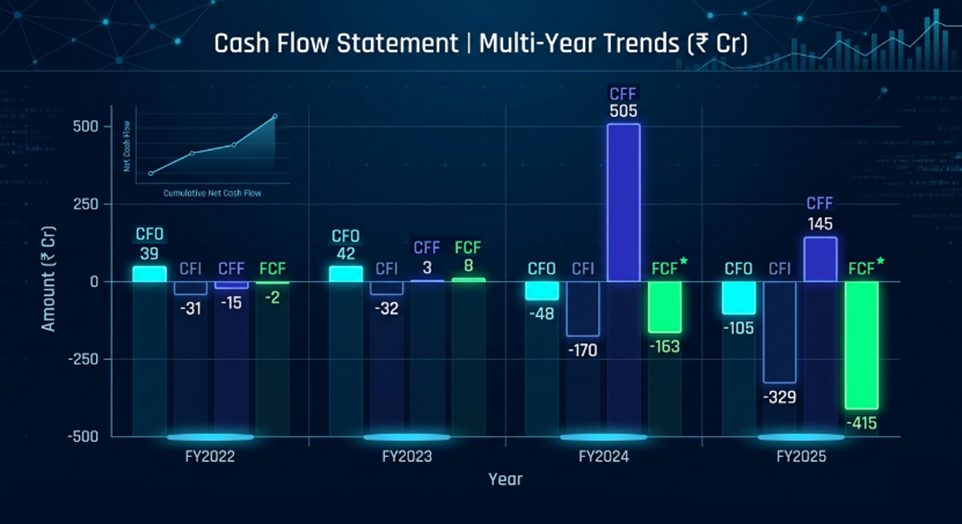

4.3 Cash Flow Analysis

Data Source: REFINITIV, Analysis: Kalkine Group

The divergence between reported net profit and operating cash flow is the most important risk flag in the entire financial analysis. In FY2025, the company reported net profit of ₹316 Cr but generated negative operating cash flow of -₹105 Cr and deeply negative free cash flow of -₹415 Cr. This gap is attributable to working capital absorption — as the business scales rapidly, it is tying up increasing amounts of capital in receivables and inventory.

This is not necessarily indicative of underlying business weakness — rapidly growing manufacturing businesses with long order execution cycles commonly exhibit this pattern. However, it does mean the company is dependent on external financing (equity and debt) to fund growth, and the sustainability of the growth trajectory is contingent on continued access to that financing.

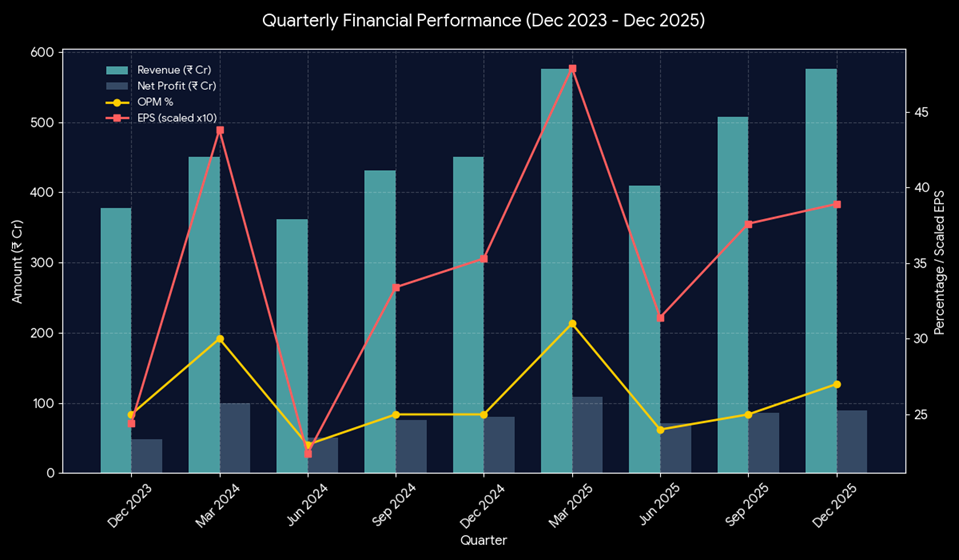

- Quarterly Performance Trend

Data Source: REFINITIV, Analysis: Kalkine Group

The quarterly trajectory demonstrates consistent revenue growth (Dec 2025 revenue of ₹576 Cr matches the record Mar 2025 quarter) and margin stability in the 24–31% range. The pattern of stronger March quarters (year-end) is typical for capital goods companies with government and defence customers who front-load procurement decisions toward fiscal year-end. The Dec 2025 quarter's ₹576 Cr revenue matching the prior peak is an encouraging sign that the growth trend is continuing.

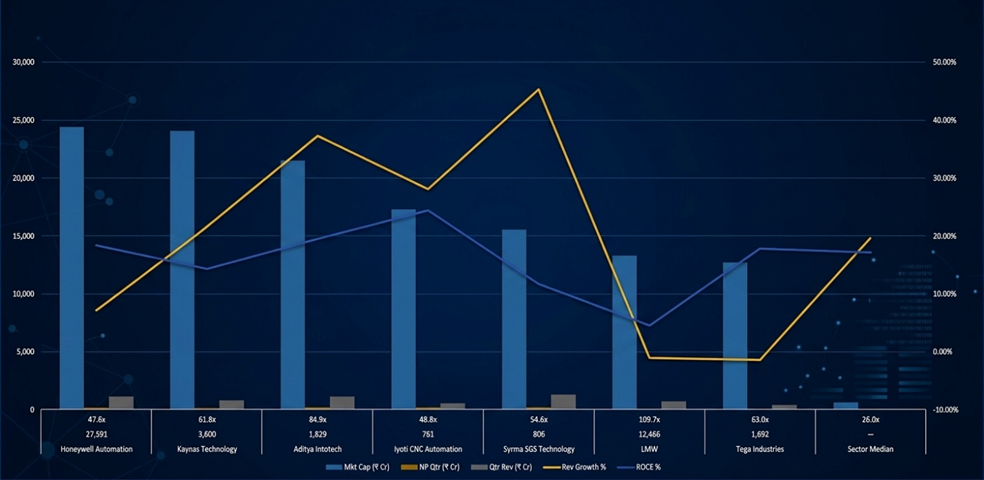

- Peer Comparison

Data Source: REFINITIV, Analysis: Kalkine Group

Data Source: REFINITIV, Analysis: Kalkine Group

Key Peer Observations

Valuation: Jyoti CNC's P/E of 48.8x is below the peer group average (excluding LMW's distorted 109.7x) and broadly in line with Honeywell (47.6x) — a profitable, well-established multinational. Given Jyoti's superior ROCE (24.4%) relative to most peers, including Honeywell (18.4%), Kaynes (14.3%), and Syrma (11.7%), the relative valuation is arguably reasonable rather than stretched.

ROCE Leadership: Jyoti's ROCE of 24.4% is the highest in the peer group, indicating it generates more operating return per rupee of capital employed than any listed comparable. This is a meaningful quality signal for a manufacturing business.

Revenue Growth: At 28.1% quarterly revenue growth, Jyoti is growing faster than Honeywell (7.1%), LMW (-1.1%), and Tega (-1.4%), and broadly comparable with the higher-growth electronics manufacturing peers Kaynes and Syrma — though in a different business and at a different margin profile.

Scale Gap: Jyoti's quarterly revenue of ₹576 Cr is smaller than Honeywell's ₹1,169 Cr and Syrma's ₹1,264 Cr, but the growth trajectory suggests this gap is narrowing. The company is at an earlier stage of its revenue compounding curve than its larger peers.

Dividend: In line with most growth peers in this comparison, Jyoti pays no dividend, retaining all earnings for reinvestment. Given the negative free cash flow profile, this is both expected and appropriate.

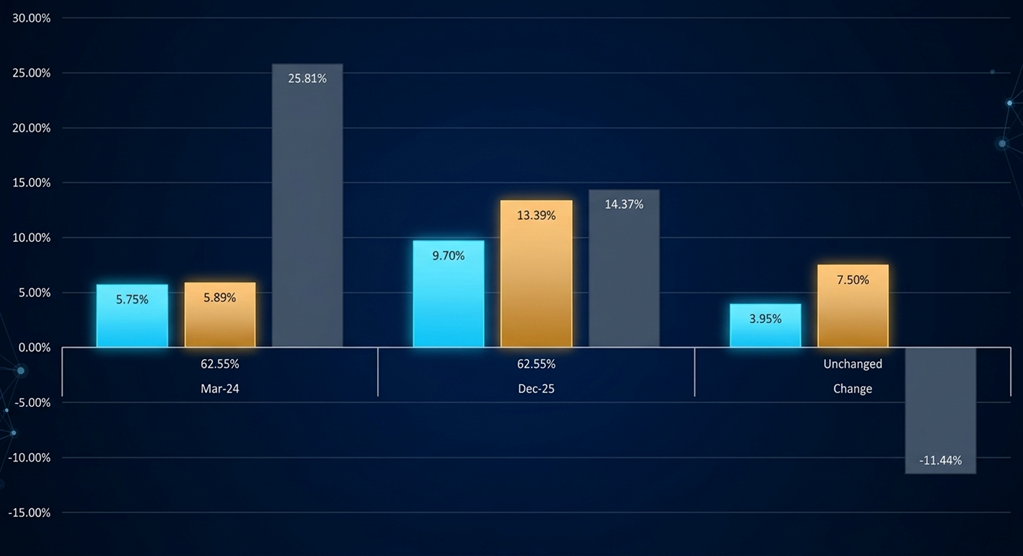

- Shareholding Pattern

Data Source: REFINITIV, Analysis: Kalkine Group

The shareholding trend over the past four quarters is one of the most constructive signals in the entire Jyoti CNC investment case. Institutional investors — both foreign (FIIs) and domestic (DIIs) — have collectively increased their stake from 11.64% in March 2024 to 23.09% by December 2025, an increase of nearly 12 percentage points. This accumulation has come almost entirely at the expense of retail public shareholders, whose holding has declined from 25.81% to 14.37%.

Institutional accumulation of this magnitude typically reflects fundamental conviction rather than momentum trading. The promoter holding remains stable at 62.55%, indicating no dilution from the founding family and sustained alignment with minority shareholders.

- Key Strengths

Market leadership with pricing power: A 10–12% domestic market share in a technically demanding product category provides genuine competitive insulation. CNC machine tool customers — particularly in aerospace and defence — have high switching costs and a preference for proven suppliers, giving Jyoti pricing power that lower-value capital goods manufacturers do not possess.

Defence and aerospace tailwind: India's defence indigenisation mandate (the Positive Indigenisation Lists issued by the Ministry of Defence) and the rapid expansion of Indian aerospace manufacturing capacity — driven by both domestic defence programmes and international MRO outsourcing — create a structural, multi-year demand tailwind for precision machining equipment. Jyoti is a direct beneficiary.

European manufacturing presence: The Huron acquisition gives Jyoti access to European OEM customers and validates its technical capability on the global stage. This is a rare differentiator for an Indian capital goods manufacturer at this market capitalisation.

Rapid margin improvement: The move from loss-making to 27% OPM in under three years demonstrates significant operating leverage and management execution quality.

Institutional accumulation: The near-doubling of combined FII and DII ownership over four quarters reflects growing institutional conviction in the fundamental investment case.

- Key Risks

|

Risk Factor |

Description |

Severity |

|

Working Capital Deterioration |

Debtor days rising to 98; working capital days at 203 |

High |

|

Negative Free Cash Flow |

FCF of -₹415 Cr in FY2025 despite strong reported profits |

High |

|

Debt Re-accumulation |

Borrowings rising from ₹304 Cr to ₹724 Cr (Sep 2025) |

Moderate–High |

|

Valuation Premium |

Trading at 9x book value; P/E of 48.8x leaves limited margin of safety |

Moderate–High |

|

Order Execution Concentration |

Defence/aerospace clients can defer or delay orders |

Moderate |

|

1-Year Price Correction |

Stock is -33% from 52-week highs, indicating prior overvaluation or sentiment shift |

Moderate |

|

No Dividend |

Zero dividend payout despite returning to profitability |

Low |

- Bull & Bear Case

Bull Case

India's defence and aerospace capital expenditure cycle continues its multi-year upswing, driving sustained order inflows for precision machining equipment. Jyoti CNC consolidates market share from smaller domestic competitors and international suppliers, as defence indigenisation mandates favour domestic OEMs. Operating margins are maintained in the 25–30% range as product mix continues shifting toward higher-value 5-axis machines. Working capital improves as order execution timelines shorten and customer payment cycles normalise. The stock re-rates toward ₹1,100–₹1,331 (52-week high) as institutional ownership continues to build and earnings compound.

Bear Case

Government defence procurement timelines slip — a historically common occurrence — causing order conversions to be deferred and revenue growth to disappoint. Working capital continues to deteriorate, pushing the company toward further debt raises and potential equity dilution. The stock, already trading at 9x book value, de-rates further from its 52-week high of ₹1,331 as retail investors, who have been net sellers, continue to exit. A broader small-cap/midcap correction compounds company-specific weakness.

- Valuation Assessment

At ₹761 per share and a TTM EPS of ₹15.58, Jyoti CNC trades at a TTM P/E of approximately 48.8x. On a forward basis, assuming continued earnings growth consistent with the recent quarterly run-rate, the forward P/E is closer to 38–42x — still a premium, but more reflective of the growth trajectory.

The Price-to-Book of approximately 9x is the most challenging valuation metric to defend in isolation. However, for a business generating 24.4% ROCE with a demonstrated earnings inflection and strong institutional accumulation, a premium to book is structurally warranted. The appropriate comparable is not a commodity manufacturer but rather a high-quality precision engineering franchise with a defensible market position.

The 1-year stock price CAGR of -33% — from a 52-week high of ₹1,331 to the current ₹761 — suggests the stock corrected from an arguably overvalued position reached in 2025 and is now trading at a more moderate multiple. The current price represents a meaningful discount to peak valuation, which may offer an improved entry point for investors with a 3–5 year horizon.

- Investment Conclusion

Jyoti CNC Automation is a fundamentally transformed business — from a loss-making, over-leveraged manufacturer through FY2021–FY2023 to a profitable, high-return capital goods company generating ₹354 Cr in TTM net profit at a 27% operating margin. The structural tailwinds of Indian defence indigenisation and aerospace capacity expansion provide a durable multi-year demand environment that few capital goods peers can match.

The investment case is not without complexity. The working capital deterioration, negative free cash flow, and re-accumulation of debt are genuine risks that require monitoring over upcoming quarterly results. The gap between reported profits and cash generation must narrow for the investment thesis to be fully validated.

For long-term investors, the combination of ROCE leadership within the peer group, accelerating institutional ownership, stable promoter holding, and exposure to India's most structurally sound capital goods end-markets makes Jyoti CNC one of the more compelling precision engineering investment opportunities on Indian exchanges.

Investor suitability: Growth-oriented investors with a 3–5 year horizon, seeking exposure to India's defence and aerospace capital expenditure cycle through a high-margin, market-leading precision manufacturer. Investors should size positions with an awareness of working capital risk and monitor debtor days and free cash flow conversion closely in upcoming quarterly disclosures.