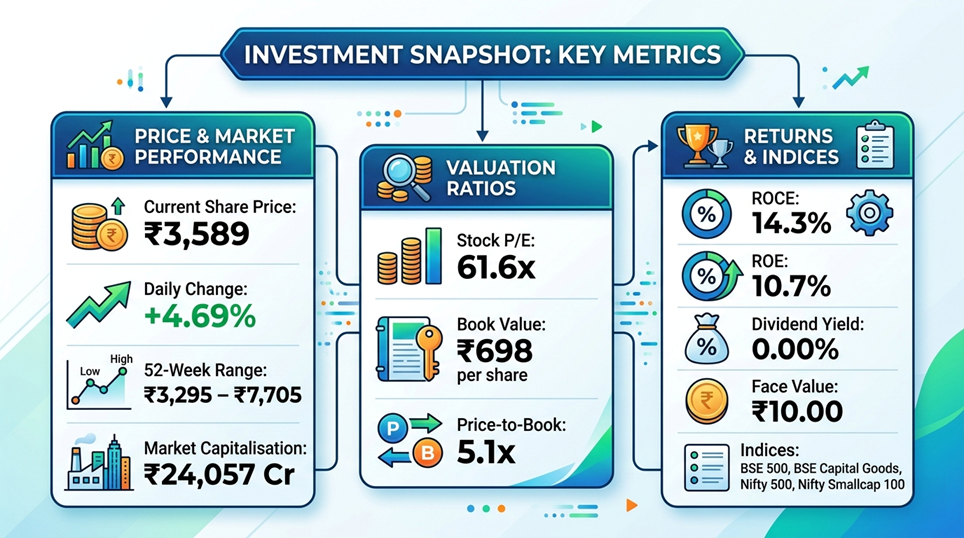

- Investment Snapshot

Data Source: REFINITIV, Analysis: Kalkine Group

- Company Overview

Kaynes Technology India Ltd is one of India's foremost end-to-end, IoT-enabled Integrated Electronics Manufacturing Services (IEMS) companies. Incorporated in 2008 and listed on Indian exchanges, Kaynes provides a comprehensive suite of services across the entire electronics value chain — from conceptual design and process engineering through to integrated manufacturing and full life-cycle support.

The company's customer base spans some of the most technically demanding and structurally growing end-markets in India and globally: automotive electronics, industrial automation, aerospace and defence, outer-space applications, nuclear systems, medical devices, railways, IoT, and IT infrastructure. This breadth of exposure is both a strategic strength and a reflection of Kaynes' ambition to be a platform-level electronics manufacturer rather than a single-vertical contract manufacturer.

In recent years, Kaynes has made a deliberate and significant pivot beyond traditional electronics manufacturing into adjacent high-growth verticals: Smart Metering (under India's national smart metering programme), Advanced Semiconductor Packaging (OSAT — Outsourced Semiconductor Assembly and Test), High-Density Interconnect (HDI) PCBs, and AI-Powered Railway Safety systems. The inauguration of its Kaynes Semicon subsidiary's Sanand GIDC plant by Prime Minister Narendra Modi on March 31, 2026 marks a landmark moment in this strategic evolution — placing Kaynes at the front of India's nascent domestic semiconductor ecosystem.

- Financial Performance Analysis

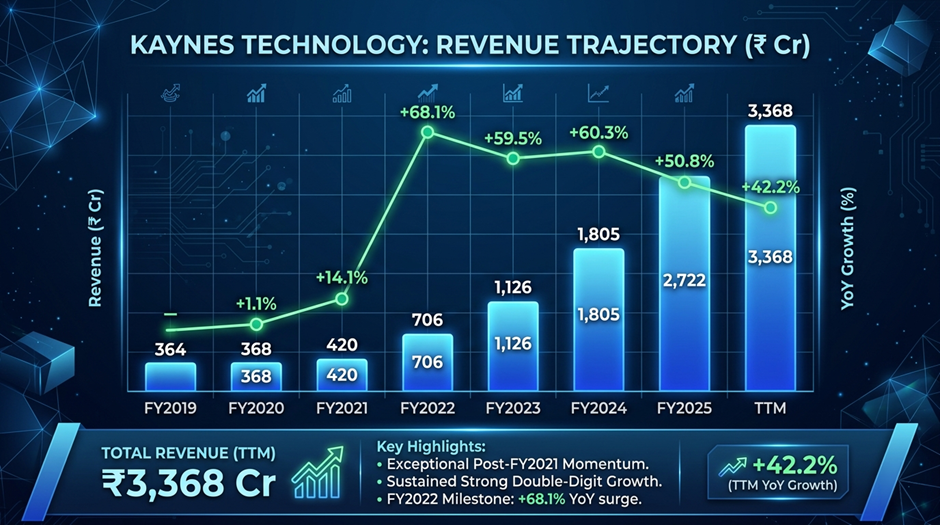

3.1 Revenue Growth — Exceptional Compounding

Kaynes' revenue trajectory is among the strongest in the Indian electronics manufacturing sector over any meaningful time horizon.

Data Source: REFINITIV, Analysis: Kalkine Group

The 5-year revenue CAGR of 49% and 3-year CAGR of 57% are genuinely exceptional for a manufacturing business of this scale. From a base of ₹364 Cr in FY2019, Kaynes has grown to a TTM revenue run-rate of ₹3,368 Cr — nearly a 9x increase in six years. The growth has been broad-based across end-markets, driven by both organic market share gains and the expansion into new verticals such as smart metering and semiconductor packaging.

Crucially, growth has remained robust even as the base has grown larger. The TTM growth rate of 42% — on a ₹2,722 Cr FY2025 base — indicates the demand environment continues to support rapid scaling without visible deceleration.

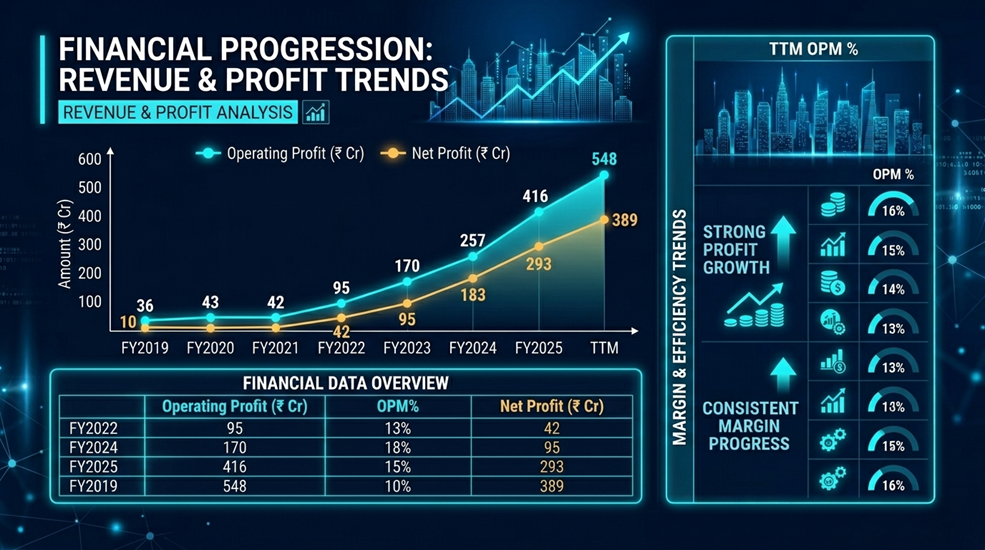

3.2 Profitability — Consistent but Margin-Constrained

Operating margins have been notably stable — fluctuating within a tight 13–17% band across all years — reflecting the nature of the integrated electronics manufacturing business, which operates at lower margins than capital goods peers like Jyoti CNC but compensates through volume and revenue growth velocity. The TTM OPM of 16% represents the upper end of Kaynes' historical range, driven by improving product mix and the higher-margin semiconductor and smart metering businesses gaining share within the revenue mix.

Net profit has grown at a 5-year CAGR of 95% and a 3-year CAGR of 90% — exceptional compounding driven by operating leverage and the significant reduction in the effective tax rate from earlier years.

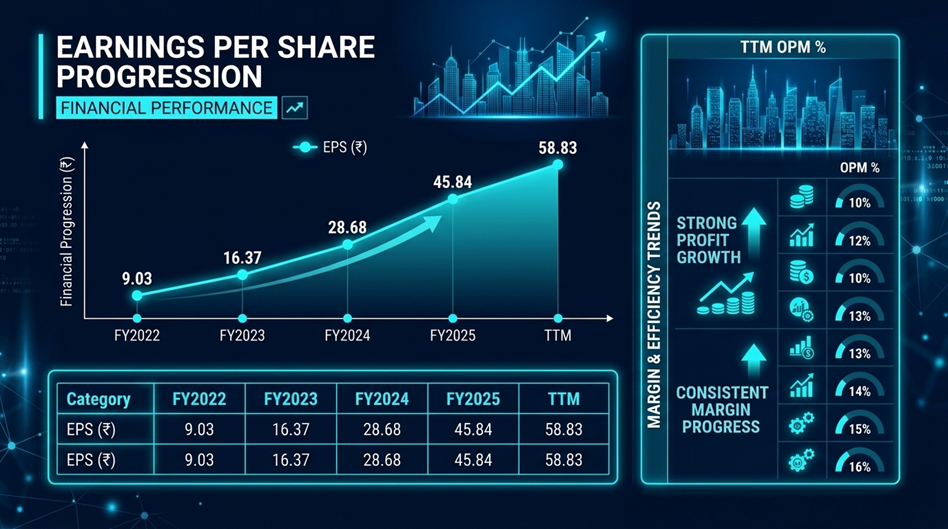

3.3 Earnings Per Share Progression

Data Source: REFINITIV, Analysis: Kalkine Group

EPS has more than tripled over three years, reflecting both profit growth and the absence of meaningful equity dilution since the IPO-era capital raise. The TTM EPS of ₹58.83 against the current share price of ₹3,589 implies a TTM P/E of approximately 61x — a premium that the market is sustaining on the basis of growth expectations for the semiconductor and smart metering businesses.

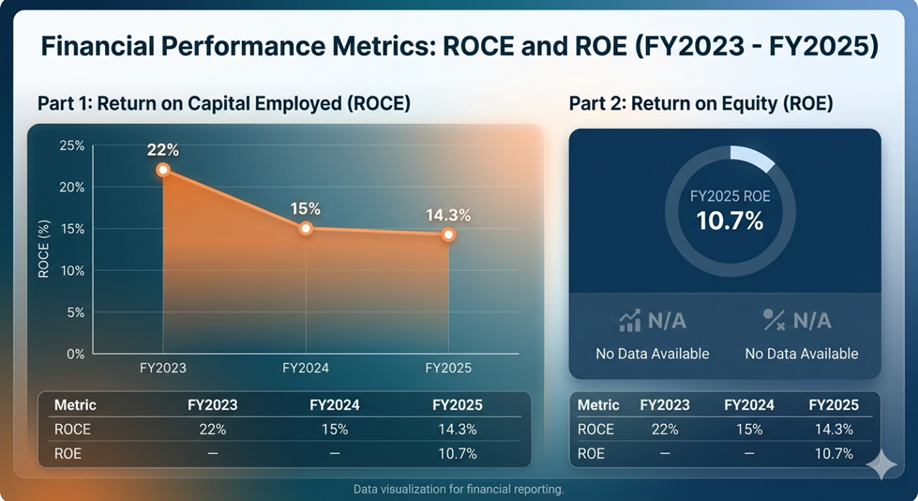

3.4 Return Metrics

Data Source: REFINITIV, Analysis: Kalkine Group

The decline in ROCE from 22% in FY2023 to 14.3% in FY2025 is the most analytically important financial trend in this report and warrants careful examination. This compression is not indicative of business deterioration — it is a direct consequence of the massive capital deployment into new infrastructure, particularly the semiconductor OSAT facility. The company has invested heavily in fixed assets (₹845 Cr in FY2025, up from ₹319 Cr in FY2024) and CWIP (₹391 Cr), infrastructure that has not yet begun generating returns. As these assets move from construction to production, ROCE should recover. However, investors must price in the near-term dilution of capital efficiency metrics that large-scale greenfield investment invariably produces.

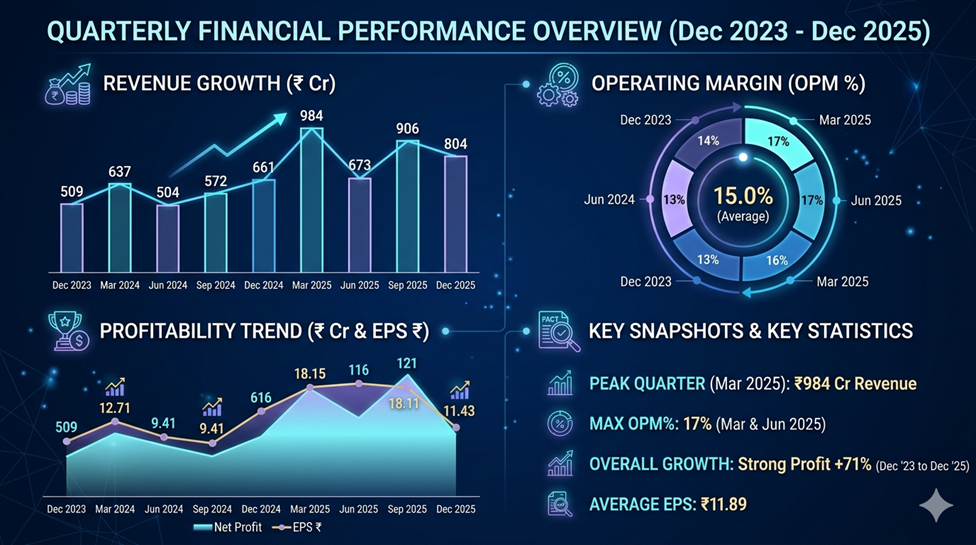

- Quarterly Performance Trend

Data Source: REFINITIV, Analysis: Kalkine Group

The quarterly data reveals two important patterns. First, Kaynes exhibits a pronounced March quarter seasonality — the Mar 2025 quarter at ₹984 Cr revenue is 46% higher than the Jun 2025 quarter at ₹673 Cr, a pattern consistent with government procurement and defence order closures before fiscal year-end. Second, the Sep 2025 quarter at ₹906 Cr and OPM of 16% represents a strong mid-year performance, indicating the March-quarter pattern is being complemented by improving non-March quarter execution.

The Dec 2025 quarter revenue of ₹804 Cr, while below the Sep 2025 peak, represents 21.6% year-on-year growth — consistent with the company's stated growth trajectory. Quarterly net profit has more than tripled from ₹23 Cr in Dec 2022 to ₹77 Cr in Dec 2025.

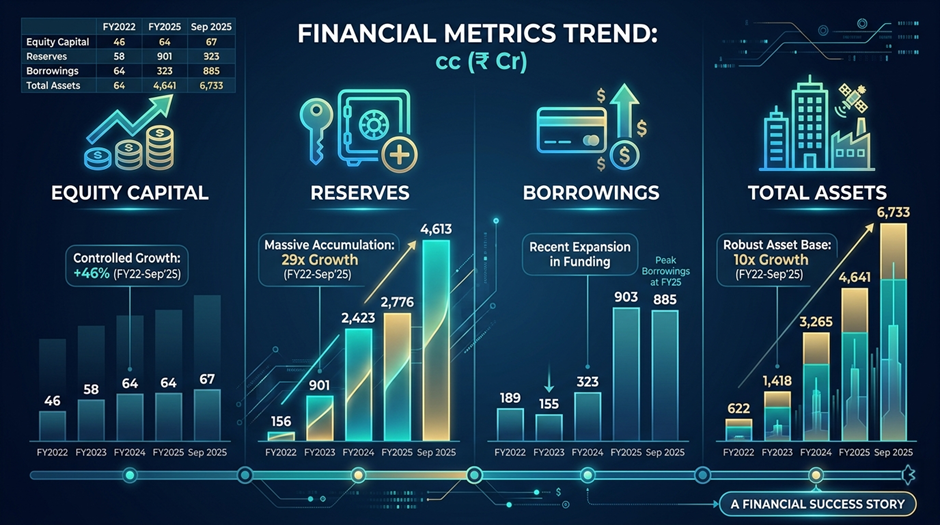

- Balance Sheet & Capital Deployment Analysis

Data Source: REFINITIV, Analysis: Kalkine Group

The balance sheet has expanded dramatically — from ₹622 Cr in FY2022 to ₹6,733 Cr by September 2025 — driven primarily by successive equity raises that have funded the semiconductor and smart metering capex programme. Reserves of ₹4,613 Cr by September 2025 reflect both retained earnings and the substantial fresh equity capital raised.

Borrowings have increased from ₹323 Cr in FY2024 to ₹903 Cr in FY2025 and ₹885 Cr in September 2025, reflecting debt financing of the OSAT facility capex. This is manageable relative to the equity base (debt-to-equity is less than 0.2x), but rising interest costs — from ₹56 Cr in FY2024 to ₹106 Cr in FY2025 — are beginning to represent a more meaningful drag on the P&L.

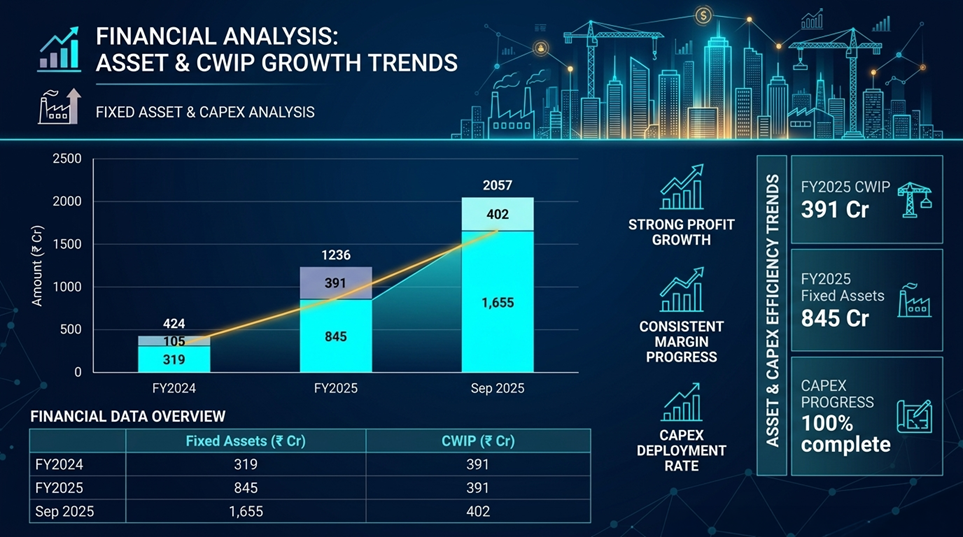

5.2 Fixed Asset & Capex Investment

Data Source: REFINITIV, Analysis: Kalkine Group

Fixed assets have grown from ₹319 Cr to ₹1,655 Cr in approximately 18 months — a 5x increase reflecting the scale of the semiconductor and advanced manufacturing infrastructure being built. The CWIP balance of ₹402 Cr as of September 2025 indicates further assets are in the pipeline. The Sanand GIDC semiconductor plant inaugurated by the Prime Minister in March 2026 is the most significant of these, and its transition from CWIP to productive fixed assets will be the critical inflection point for ROCE recovery.

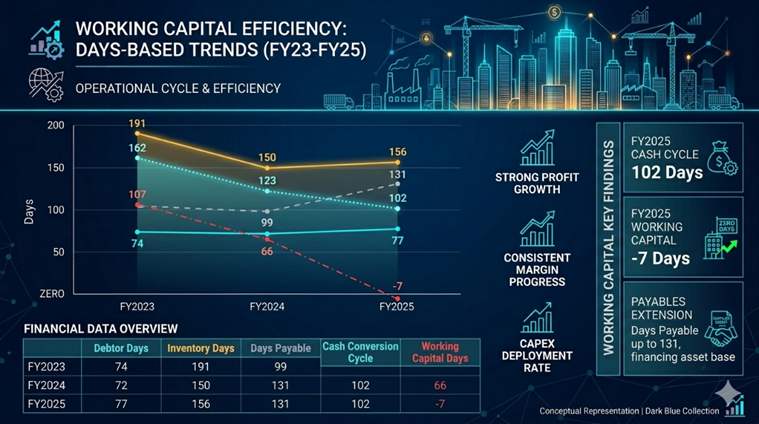

5.3 Working Capital Position

Data Source: REFINITIV, Analysis: Kalkine Group

Unlike Jyoti CNC, where working capital deterioration is a key concern, Kaynes has demonstrated impressive working capital discipline. The cash conversion cycle has compressed from 162 days in FY2023 to just 102 days in FY2025, and working capital days have improved from 107 to effectively zero (-7 days). This is a hallmark of strong receivables management and increasingly favourable supplier payment terms — typically a sign of improved commercial positioning and procurement leverage as the business scales.

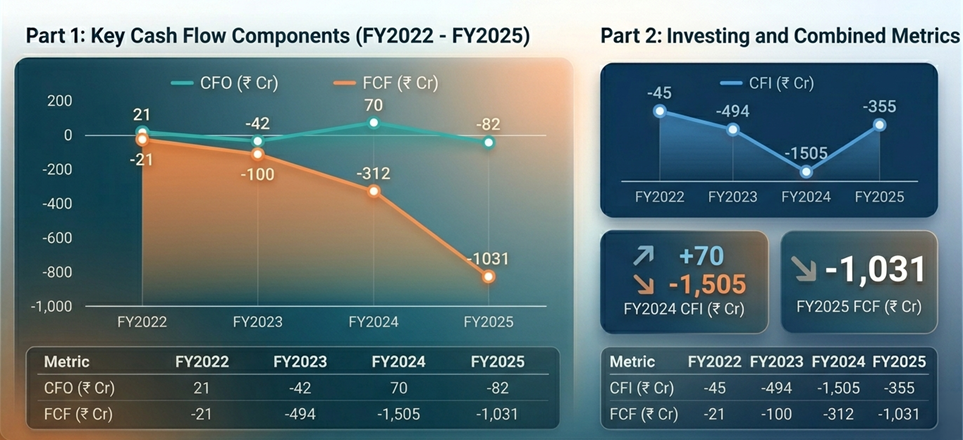

5.4 Cash Flow Analysis

Data Source: REFINITIV, Analysis: Kalkine Group

Free cash flow has been deeply negative across recent years — reflecting the scale of capital investment in new manufacturing infrastructure rather than operational underperformance. The CFI of -₹1,505 Cr in FY2024 reflects the single largest investment year, associated with the semiconductor facility and smart metering capacity expansion. FY2025's CFI moderated to -₹355 Cr as the major capex phase moved toward completion. Operating cash flow of -₹82 Cr in FY2025 remains a concern, though the improving working capital position should support CFO normalisation as the scale of new business from the semiconductor facility begins to flow through.

- Peer Comparison

|

Company |

CMP (₹) |

P/E |

Mkt Cap (₹ Cr) |

NP Qtr (₹ Cr) |

Qtr Rev (₹ Cr) |

Rev Growth % |

ROCE % |

|

Honeywell Automation |

27,522 |

47.5x |

24,329 |

121 |

1,169 |

+7.1% |

18.4% |

|

Kaynes Technology |

3,589 |

61.6x |

24,057 |

77 |

804 |

+21.6% |

14.3% |

|

Aditya Infotech |

1,800 |

83.6x |

21,207 |

96 |

1,139 |

+37.3% |

19.5% |

|

Jyoti CNC Automation |

776 |

49.7x |

17,643 |

89 |

576 |

+28.1% |

24.4% |

|

Syrma SGS Technology |

798 |

54.1x |

15,384 |

110 |

1,264 |

+45.4% |

11.7% |

|

LMW |

12,520 |

110.2x |

13,375 |

15 |

758 |

-1.1% |

4.5% |

|

Tega Industries |

1,693 |

63.0x |

12,717 |

20 |

404 |

-1.4% |

17.8% |

|

Sector Median |

— |

27.2x |

620 |

5.6 |

81 |

+19.7% |

17.1% |

Key Peer Observations

Valuation premium: Kaynes trades at 61.6x P/E — the second-highest in the peer group after Aditya Infotech (83.6x) and materially above Jyoti CNC (49.7x) and Syrma (54.1x). This premium reflects the market’s ascription of option value to the semiconductor packaging and smart metering businesses, which carry higher long-term growth and margin potential than traditional IEMS.

ROCE at the lower end: Kaynes’ ROCE of 14.3% is below Jyoti CNC (24.4%), Honeywell (18.4%), Aditya Infotech (19.5%), and Tega (17.8%), and only marginally above Syrma (11.7%). This reflects the capital deployment phase the company is in — large investments in fixed assets and infrastructure not yet generating full returns. The ROCE figure should be evaluated in context of the investment cycle rather than as a static quality indicator.

Revenue growth leadership: At 21.6% quarterly revenue growth, Kaynes lags Syrma (45.4%), Aditya (37.3%), and Jyoti (28.1%) in the peer group. However, Kaynes is growing off a larger base (₹804 Cr quarterly revenue vs. Jyoti’s ₹576 Cr) and has guided for accelerating growth from the OSAT and smart metering businesses.

Market cap premium to peers: At ₹24,057 Cr, Kaynes carries the second-highest market capitalisation in the peer group behind Honeywell (₹24,329 Cr) — a global, multi-decade industrial giant. This valuation positioning implies the market believes Kaynes’ growth trajectory justifies a premium over more established peers.

- 7 7. Strategic Developments & Catalysts

- 1 Kaynes Semicon — The Defining Strategic Pivot

The inauguration of Kaynes Semicon's’Sanand GIDC plant by Prime Minister Modi on March 31, 2026 is the most consequential development in the company's’history. This facility positions Kaynes as a participant in India's’domestic semiconductor ecosystem — a market the government has targeted with over ₹76,000 Cr in incentive support under the India Semiconductor Mission.

OSAT (Outsourced Semiconductor Assembly and Test) is the entry point for most countries into semiconductor manufacturing. India's’OSAT market is nascent but strategically prioritised, with domestic demand from defence electronics, consumer devices, and automotive chips providing a captive market for the initial production ramp. If Kaynes executes the Sanand facility ramp-up successfully, it gains first-mover advantage in a segment with very high barriers to entry and government-supported demand.

7.2 Smart Metering — Recurring Revenue Visibility

India's’national smart metering programme, targeting over 250 million smart meters, represents a multi-year procurement opportunity with government-backed demand visibility. Kaynes' ’mart metering manufacturing capacity positions it as a key supply-side beneficiary of this programme. Smart meters represent a shift toward more recurring, contracted revenue — different in character from the project-by-project nature of traditional IEMS and defence electronics.

7.3 Credit Rating — CRISIL A/Stable Reaffirmed

CRISIL's’reaffirmation of an A/Stable rating for ₹770 Cr of facilities (March 2026) is a meaningful signal of credit quality. An 'A‘ ’ating from CRISIL — India's’most established rating agency — indicates adequate capacity to service debt obligations and provides Kaynes with continued access to bank financing at competitive rates. The removal of the rating watch (previously on watch for the semiconductor investment) normalises the credit profile and reduces financing risk.

7.4 MD Insider Trading Settlement

The SEBI settlement announced March 27, 2026 — in which MD Ramesh Kunhikannan was fined ₹23,42,600 for insider trading, paid personally — is a governance event that requires acknowledgement. The company has made clear the fine was paid personally by the MD rather than by the company. While the settlement amount is modest relative to the company's’scale, it is a governance flag that institutional investors will assess carefully, particularly in the context of promoter holding reduction (discussed below).

- Shareholding Pattern Analysis

Data Source: REFINITIV, Analysis: Kalkine Group

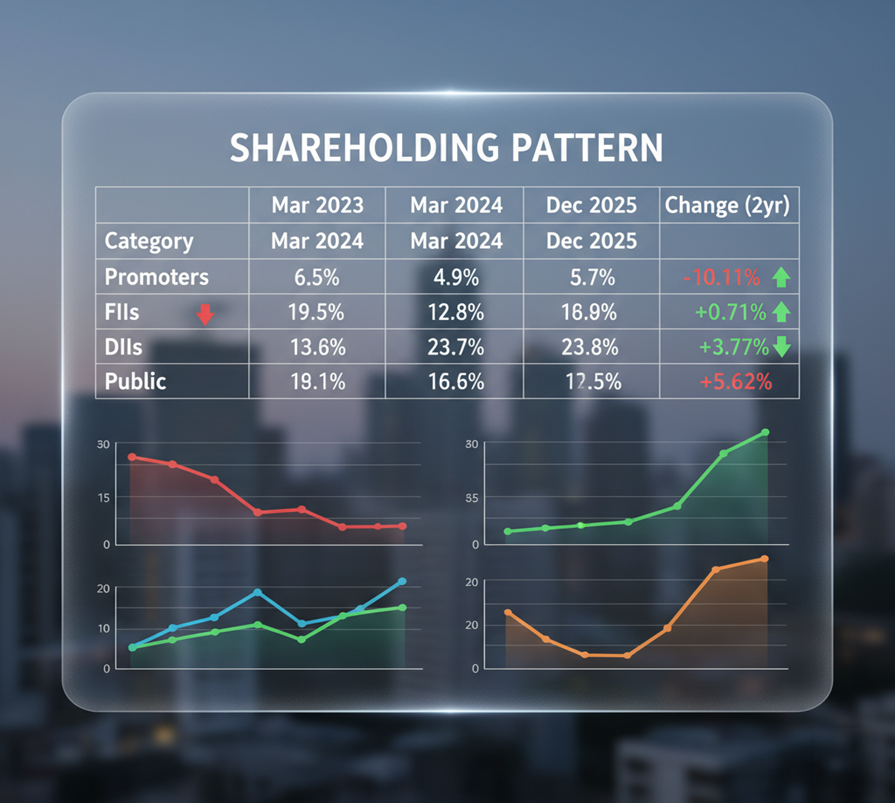

The shareholding trend contains the most analytically mixed signals in the Kaynes investment case. Two contrasting dynamics are present simultaneously:

Promoter holding decline: Promoter stake has fallen from 63.57% in March 2023 to 53.46% in December 2025 — a reduction of over 10 percentage points over two years. This is flagged explicitly as a "con" by the screener. Promoter selling at a time when the company is in the middle of its most ambitious capital investment cycle raises questions about insider conviction in the near-term risk/reward profile. The MD's insider trading settlement adds a layer of governance concern to this trend.

Institutional accumulation: Domestic institutional investors have increased holdings from 12.96% to 16.73% over the same period, indicating professional investor conviction in the medium-term thesis. DII ownership peaked at 23.66% in September 2025 before moderating to 16.73% in December 2025 — the moderation may reflect profit-taking after the stock's decline from its ₹7,705 52-week high.

Public shareholder growth: The number of shareholders has grown from 45,643 in March 2023 to 366,333 in December 2025 — an 8x increase — indicating rapidly broadening retail interest in the stock.

- Key Strengths

Platform business model: Kaynes is not a single-vertical contract manufacturer — it is a platform spanning automotive, defence, aerospace, medical, IoT, smart metering, and semiconductor packaging. This diversification provides resilience against end-market cyclicality and creates multiple independent growth engines.

Semiconductor first-mover advantage: The Sanand OSAT facility places Kaynes ahead of most Indian peers in the domestic semiconductor manufacturing ecosystem, a segment with high barriers to entry, government support, and long-term strategic demand.

Working capital excellence: The compression of the cash conversion cycle from 162 days to 102 days and improvement of working capital days to near-zero is a genuine operational achievement that most electronics manufacturers struggle to replicate.

Revenue compounding at scale: Sustaining 42%+ TTM revenue growth on a ₹2,722 Cr FY2025 base is a rare quality that justifies premium valuation multiples.

CRISIL A credit rating: Provides low-cost debt access and financial credibility for the capital-intensive semiconductor investment cycle.

- Key Risks

|

Risk Factor |

Description |

Severity |

|

Promoter Stake Reduction |

-10.1% over 2 years raises governance and conviction questions |

High |

|

OSAT Ramp-Up Execution |

Semiconductor facility must achieve utilisation targets to justify capex |

High |

|

ROCE Compression |

Capital deployed not yet generating returns; ROE at a 3-year low of 11.3% |

Moderate–High |

|

Negative Free Cash Flow |

FCF of -₹1,031 Cr in FY2025; sustained external funding dependency |

Moderate–High |

|

Valuation at 61.6x P/E |

-53% decline from 52-week high signals prior overvaluation; still premium |

Moderate–High |

|

MD Governance Event |

SEBI insider trading settlement; personal fine but corporate reputation risk |

Moderate |

|

Interest Cost Escalation |

Interest charges doubled from ₹56 Cr to ₹106 Cr; rising with borrowings |

Moderate |

- Bull & Bear Case

Bull Case

The Sanand OSAT facility ramps up successfully, generating semiconductor revenue that carries materially higher margins than traditional IEMS. Smart metering contracts flow at scale, providing multi-year revenue visibility. ROCE recovers toward 20%+ as the capital investment cycle completes and productive capacity generates returns. The market re-rates the stock toward its 52-week high as the semiconductor thesis is validated, with a path toward ₹5,000–₹6,000 over 18–24 months. India's electronics manufacturing ecosystem continues to attract global OEM supply chain diversification away from China, driving structural demand for Kaynes' capabilities.

Bear Case

The OSAT facility ramp is slower than anticipated — a common pattern for first-of-kind manufacturing facilities — extending the period of ROCE compression and negative free cash flow. Promoter selling continues, signalling insider concern about near-term execution risk. The stock, already down 53% from its 52-week high, de-rates further as the market loses patience with the capital deployment cycle. Rising interest costs and borrowings pressure the P&L at a time when returns on invested capital remain subdued.

- Valuation Assessment

At ₹3,589 and a TTM EPS of ₹58.83, Kaynes trades at 61x TTM P/E. On a forward basis, assuming continued earnings growth toward ₹80–90 EPS in FY2026 (extrapolating the quarterly run-rate), the forward P/E moderates to approximately 40–45x — a more palatable multiple for a business with 40%+ revenue growth and a potentially transformative semiconductor business in early ramp.

The Price-to-Book of 5.1x — materially lower than Jyoti CNC's 9x — reflects the much larger equity base built through successive capital raises. At ₹6,733 Cr in total assets and growing, Kaynes is a capital-intensive infrastructure business as much as it is a services company.

The stock's 1-year decline of 28% (from a 52-week high of ₹7,705 to the current ₹3,589) has brought the valuation from extreme to elevated. For investors with a 3–5 year horizon and conviction in the semiconductor and smart metering growth engines, the current price represents a meaningfully improved entry point relative to 2025 peak valuations.

- Investment Conclusion

Kaynes Technology is at an inflection point. The traditional IEMS business — spanning automotive, defence, aerospace, and IoT — is performing well, growing at 40%+ and generating improving profitability. Overlaid on this is a strategic transformation of potentially much greater long-term significance: the entry into semiconductor OSAT and smart metering manufacturing at scale, backed by government support and anchored by the Prime Minister-inaugurated Sanand facility.

The near-term financial picture is complex. ROCE and ROE are compressed by capital deployment. Free cash flow is deeply negative. Promoter selling is a governance concern. The stock has declined 53% from its peak, reflecting market recognition that near-term execution risk is elevated.

For long-term investors, the question is whether the semiconductor and smart metering businesses will deliver the transformative growth and margin improvement that the current investment cycle is designed to enable. If they do, Kaynes at current prices represents a compelling entry point into what could become India's first significant vertically integrated electronics and semiconductor company.

Investor suitability: Growth-oriented investors with a 3–5 year horizon, high conviction in India's electronics and semiconductor manufacturing ecosystem, and tolerance for near-term execution risk, ROCE compression, and continued negative free cash flow during the investment cycle. Close monitoring of OSAT ramp-up progress, promoter shareholding trends, and quarterly ROCE trajectory is essential.