Godrej Consumer Products (NSE:GODREJCP) reported stable demand conditions in the domestic FMCG sector during Q4 FY26. Consumer sentiment remained steady, supported by easing food inflation and normalization of trade channels following the GST transition. Policy measures such as personal income tax relief and GST rationalization are expected to support the sector, even as crude-linked inflation pressures emerge.

Standalone Performance Reflects Volume-Led Growth

The standalone business is expected to deliver double-digit underlying sales growth alongside high-single digit volume growth. Excluding soaps, volume growth continues in double digits, with expansion seen across key categories. The company indicated that growth remains broad-based, supported by performance in its future categories. EBITDA margins are expected to stay within the normative range, aided by cost-saving initiatives implemented during the quarter.

Indonesia Business Shows Signs of Stabilization

The Indonesia segment is expected to record mid-single digit underlying volume growth in Q4 FY26. Competitive intensity has moderated compared to earlier periods, with the business sustaining market share gains across categories. This reflects gradual stabilization following earlier challenges in the region.

GAUM Segment Maintains Growth Momentum

The GAUM (Godrej Africa, USA, and Middle East) business is expected to deliver double-digit sales growth and high-single digit volume growth. Growth has been broad-based across geographies and categories, with Hair Fashion and related segments continuing to see consumer traction across markets.

Consolidated Outlook and Margin Trajectory

At the consolidated level, revenue growth is expected to remain close to double digits, reflecting sequential improvement through the fiscal year. EBITDA growth is projected to remain broadly in line with revenue trends, indicating margin stability despite cost pressures.

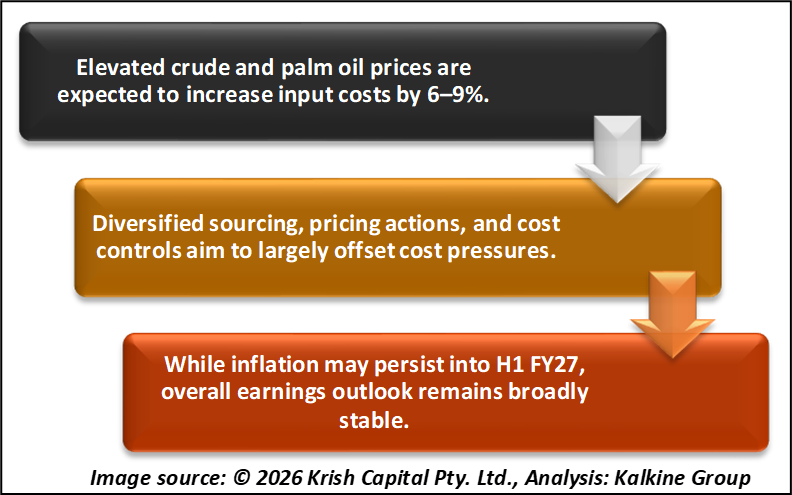

Commodity Inflation and Cost Management Measures

Global developments toward the end of Q4 FY26 have led to a rise in crude oil prices, increasing pressure on derivative input costs. With Brent crude estimated between USD 100–110 and palm oil between MYR 4500–4800, the company expects a cost impact of 6–9%.

To manage this, the company has implemented procurement diversification, pricing adjustments, cost-saving measures, and media optimization. It expects to offset most cost increases and remain broadly aligned with its original bottom-line plans for FY27. However, sustained inflation into the first half of FY27 remains a key consideration.

Share Performance

Godrej Consumer Products (NSE:GODREJCP) is currently trading near 1,032, remaining below its 50-day SMA around 1,129, indicating continued short-term weakness. The stock has corrected sharply from recent highs near 1,240 to around 1,000–1,030, reflecting notable selling pressure. Momentum remains subdued, with RSI near 43, though showing early signs of stabilisation from oversold levels. Immediate support is placed near 1,000, followed by 960, while resistance is likely near 1,080–1,100 and stronger resistance around 1,120–1,130. Overall, the price trend remains cautiously weak unless the stock sustains above key resistance levels.

Charts by TradingView

Summary

Godrej Consumer Products (NSE:GODREJCP) Q4 FY26 update indicates steady demand conditions and volume-led growth across key markets. Standalone and GAUM businesses show broad-based expansion, while Indonesia stabilizes. Commodity inflation remains a concern, with expected cost pressures partly offset through pricing and efficiencies. The company anticipates maintaining its financial trajectory, subject to external volatility and evolving macroeconomic conditions.