Hindustan Unilever Limited’s Q3FY26 earnings season presented investors with a familiar paradox. On the surface, the country’s largest FMCG company delivered steady revenue growth, stable volumes, and a sharp rise in reported profits. Yet, the market responded with a sharp correction, as the stock declined over 4% following the results.

Operational Performance Remains Resilient

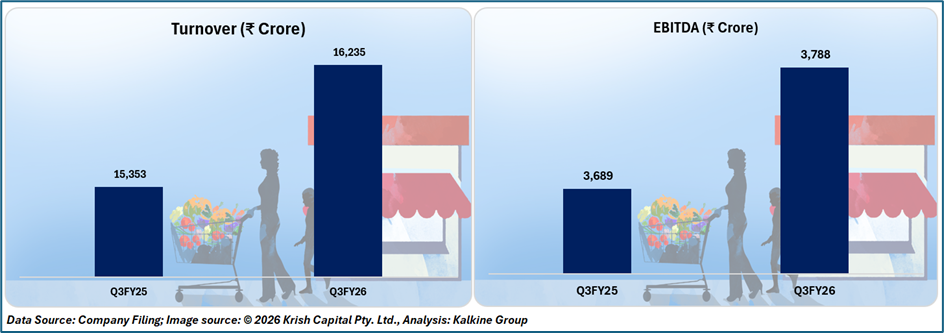

For the quarter ended December 2025, Hindustan Unilever reported turnover of ₹16,235 crore, reflecting a year-on-year growth of 6%. EBITDA stood at ₹3,788 crore, up 3% YoY, while profit after tax before exceptional items rose marginally by 1% to ₹2,562 crore.

However, EBITDA margins declined by 70 basis points to 23.3%, highlighting persistent cost pressures and elevated investment intensity. While volume growth of 4% indicates improving consumer demand, limited pricing power constrained margin expansion, particularly in mass and mid-premium categories.

Earnings Quality Under Scrutiny

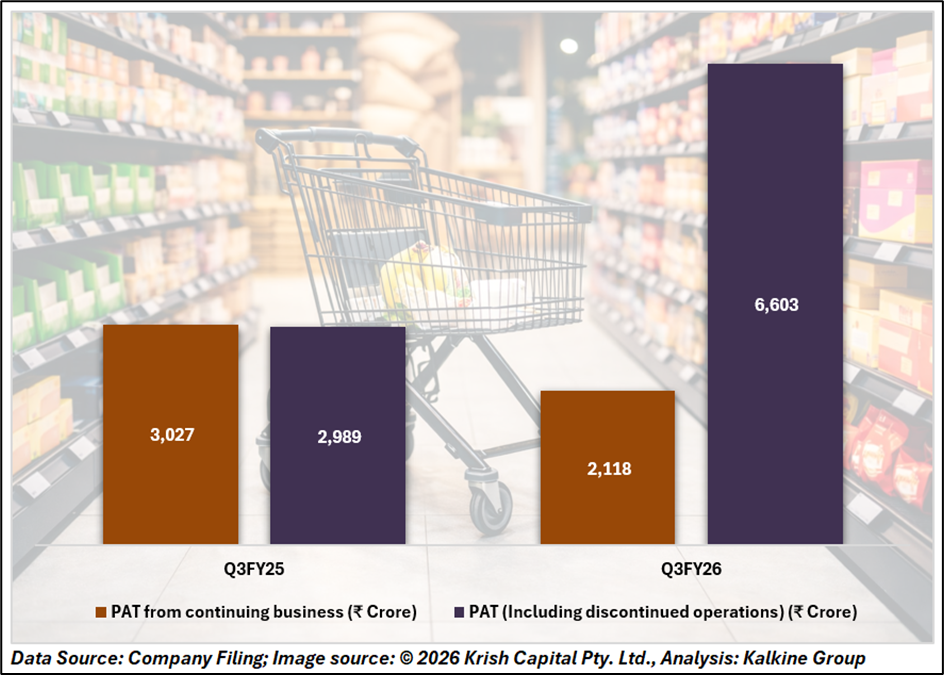

A key feature of Q3FY26 was the sharp divergence between underlying profitability and reported earnings. Reported profit surged 121% year-on-year to ₹6,603 crore, largely driven by exceptional items linked to portfolio restructuring.

These included gains from the demerger of the ice cream business, fair valuation adjustments on financial liabilities, and restructuring-related expenses. Notably, the demerger generated a one-time gain of ₹4,611 crore. Excluding these items, profit from continuing operations declined by 30% YoY, reinforcing investor concerns regarding the sustainability of near-term earnings.

Strategic Portfolio Realignment Accelerates

Q3FY26 also marked an important milestone in HUL’s portfolio transformation strategy.

The company approved the acquisition of the remaining 49% stake in Zywie Ventures (OZiva) for ₹824 crore, making it a wholly owned subsidiary. This move strengthens HUL’s presence in the fast-growing health and wellness segment.

Simultaneously, HUL approved the divestment of its 19.8% stake in Nutritionalab for ₹307 crore. The exit reflects a sharper focus on scalable and synergistic assets.

In addition, the completed demerger of the ice cream business into Kwality Wall’s India Limited has structurally simplified the company’s operating model, allowing management to focus on core FMCG categories.

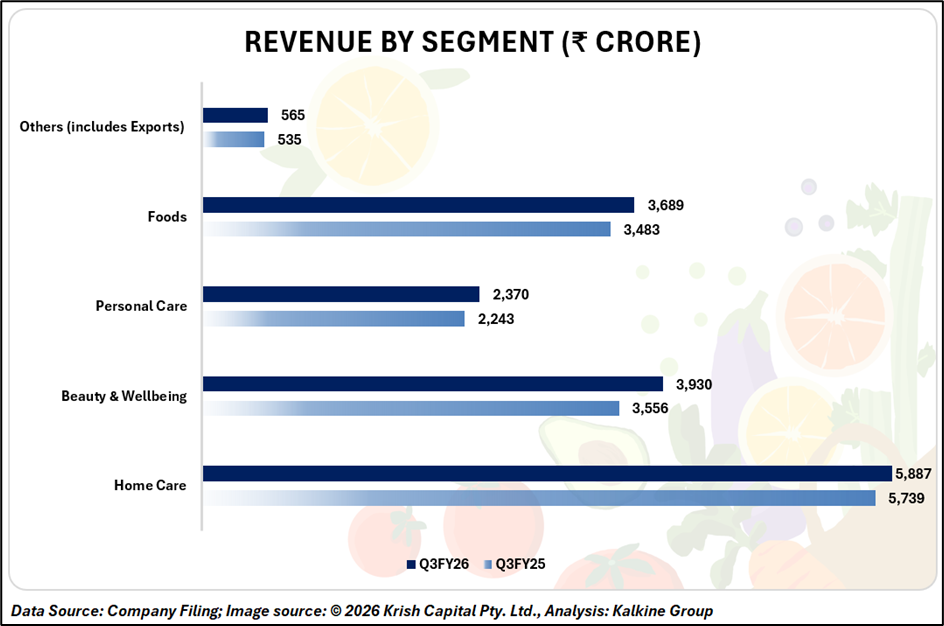

Segment Trends Highlight Volume-Led Growth

Segment-wise performance during the quarter reflected broad-based demand recovery, though pricing remained restrained.

Home Care strengthened its leadership position with its highest-ever market share. Beauty & Wellbeing benefited from strong hair care and wellness brand performance. Personal Care saw continued premiumisation, while Foods delivered high-single-digit volume growth, supported by beverages and packaged foods.

Management highlighted underlying sales growth of 5% and volume growth of 4% during the quarter.

Technical Analysis

Hindustan Unilever is trading near ₹2,356, below its 9-day EMA, indicating short-term weakness. The recent sharp decline reflects renewed selling pressure. RSI at around 46 suggests subdued momentum and limited buying strength. Immediate support lies near ₹2,300-2,180, while resistance is placed around ₹2,580–2,700. Overall, the near-term trend remains neutral with a cautious outlook.

Conclusion

Hindustan Unilever’s Q3FY26 performance reflects steady operational resilience but weak earnings quality due to one-off gains. While volume recovery and portfolio realignment support long-term prospects, margin pressure and limited pricing power remain key concerns. In the near term, subdued momentum and cautious investor sentiment may keep the stock range-bound.