HDB Financial Services Limited (NSE:HDBFS) is a leading Non-Banking Financial Company (NBFC) in India and a subsidiary of HDFC Bank. The company focuses on providing financial services to underserved and underbanked customers across the country.

With a strong presence of 1,730 branches across 1,161 cities and towns, HDB has built a wide distribution network, especially in Tier 3 and Tier 4 markets. Its diversified product offerings and strong parentage have helped it establish a reliable position in India’s financial sector.

Financial Performance and Earnings Growth

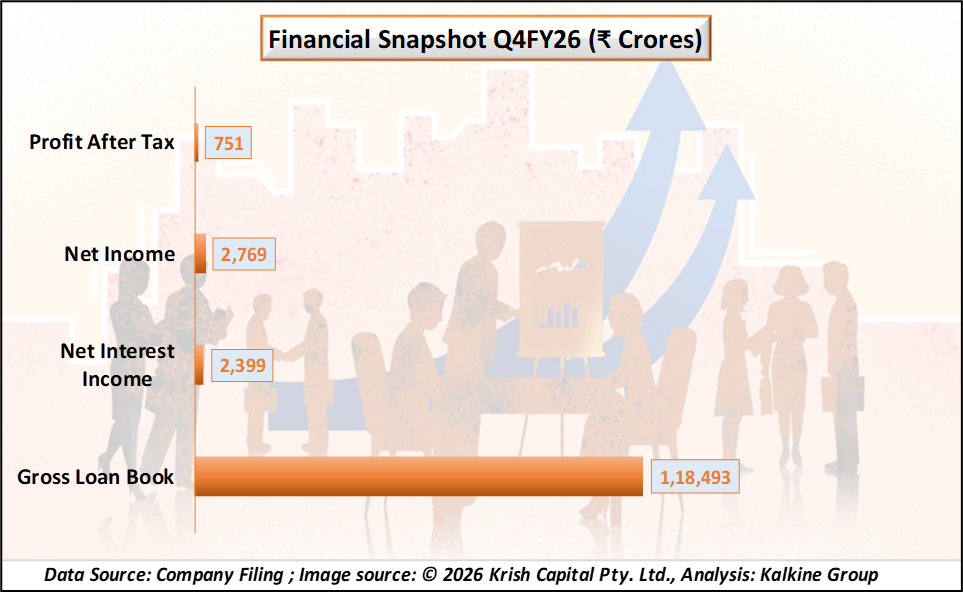

In Q4 FY2026, HDB Financial Services reported strong financial performance. The company recorded a Profit After Tax (PAT) of ₹751 crore, showing significant year-on-year growth. Net Interest Income (NII) stood at ₹2,399 crore, reflecting a 21.6% increase YoY.

The Net Interest Margin (NIM) improved to 8.23%, indicating efficient lending operations. Additionally, the Earnings Per Share (EPS) was ₹9.0, and the Book Value per share reached ₹248.9, highlighting value creation for shareholders. For the full financial year FY26, PAT stood at ₹2,544 crore, showing consistent profitability.

Loan Book Expansion and Business Growth

The company demonstrated steady growth in its lending business, with the Gross Loan Book reaching ₹1,18,493 crore as of March 31, 2026, reflecting a 10.9% year-on-year increase. Quarterly disbursements stood at ₹19,922 crore, indicating strong credit demand.

Importantly, around 74% of the loan book consists of secured loans, which helps reduce risk exposure. The customer base expanded to 22.9 million, registering a 19.7% YoY growth, which shows strong market penetration and customer trust.

Asset Quality and Risk Management

The company continues to maintain stable asset quality. The Gross Non-Performing Assets (GNPA) stood at 2.44%, while Net NPA was controlled at 1.09%. The Provision Coverage Ratio (PCR) remained strong at around 55.5%, providing a buffer against potential credit losses.

Although the Credit Cost for FY26 increased to ₹2,815 crore, it remains within manageable levels. HDB follows a disciplined risk management framework, supported by diversified lending, strict underwriting standards, and strong governance practices.

Business Diversification and Portfolio Strength

HDB Financial Services operates through three major segments: Enterprise Lending (38%), Asset Finance (38%), and Consumer Finance (24%).

This diversified portfolio helps reduce dependence on any single segment and ensures stable revenue streams. Additionally, the company maintains a highly granular loan book, where the top 20 borrowers contribute only around 0.30%, minimizing concentration risk.

Profitability and Efficiency Metrics

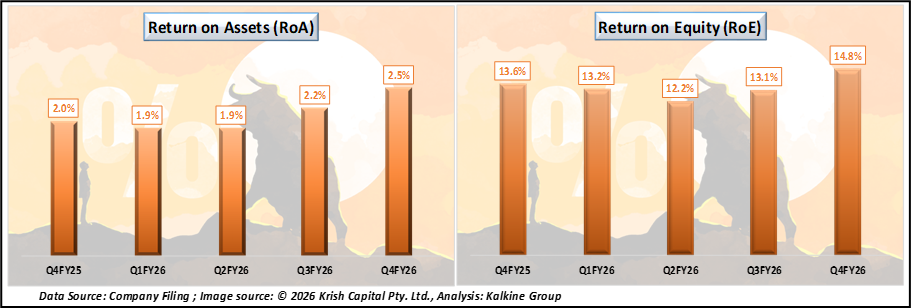

HDB Financial Services maintained healthy profitability ratios during the quarter. The Return on Assets (RoA) stood at 2.48%, while the Return on Equity (RoE) was 14.8%, reflecting efficient use of assets and shareholder capital.

The company also improved its operational efficiency, with the Cost-to-Income ratio declining to 39.5% from higher levels in previous periods. This indicates better cost management and improved operational productivity.

Capital Position and Funding Structure

The company remains well-capitalized, with a Capital Adequacy Ratio (CRAR) of 21.40%, significantly above regulatory requirements.

Its borrowing structure is well-diversified, with 45% sourced from bank loans and 31% from Non-Convertible Debentures (NCDs). The Debt-to-Equity ratio stands at around 5.0x, reflecting a balanced capital structure that supports future growth.

Technical Summary

HDB Financial Services is trading at ₹693.75, up sharply by around 7.67%, and has moved back above the 51-day SMA positioned near ₹668.16, indicating a potential shift in short-term trend from bearish to recovery mode.

The 14-day RSI stands near 64.30, reflecting improving momentum and approaching the overbought region. Immediate support is placed in the ₹660.00–630.00 zone, while resistance is seen near the ₹720.00–750.00 range.

Conclusion

In conclusion, HDB Financial Services has demonstrated strong financial performance, robust growth, and disciplined risk management in Q4 FY2026. With its diversified portfolio, strong capital base, and focus on underserved markets, the company is well-positioned for sustained long-term growth. Its consistent improvement in profitability, asset quality, and operational efficiency makes it a key player in India’s NBFC sector.

Frequently Asked Questions (FAQs)

What is HDB Financial Services?

HDB Financial Services Limited is a leading NBFC in India and a subsidiary of HDFC Bank. It offers a wide range of lending products to retail customers and small businesses, with a strong focus on underserved and underbanked segments.

Is HDB Financial Services a listed company?

HDB Financial Services is not widely listed like other major NBFCs. It is often discussed as a potential IPO candidate, but full public market participation remains limited at present.

What are the key growth drivers for HDB Financial Services?

The company’s growth is driven by its strong parentage, expanding presence in Tier 3 and Tier 4 markets, diversified lending portfolio, and a steadily growing customer base across India.

How strong is the company’s financial performance?

HDB Financial Services has demonstrated consistent profitability with strong growth in net interest income, stable margins, and healthy return ratios such as RoA and RoE, reflecting efficient operations.

Is HDB Financial Services a safe NBFC?

The company maintains relatively stable asset quality with controlled NPAs and a high proportion of secured loans. Its strong capital adequacy and disciplined risk management framework add to its overall stability, though it still carries typical NBFC risks.