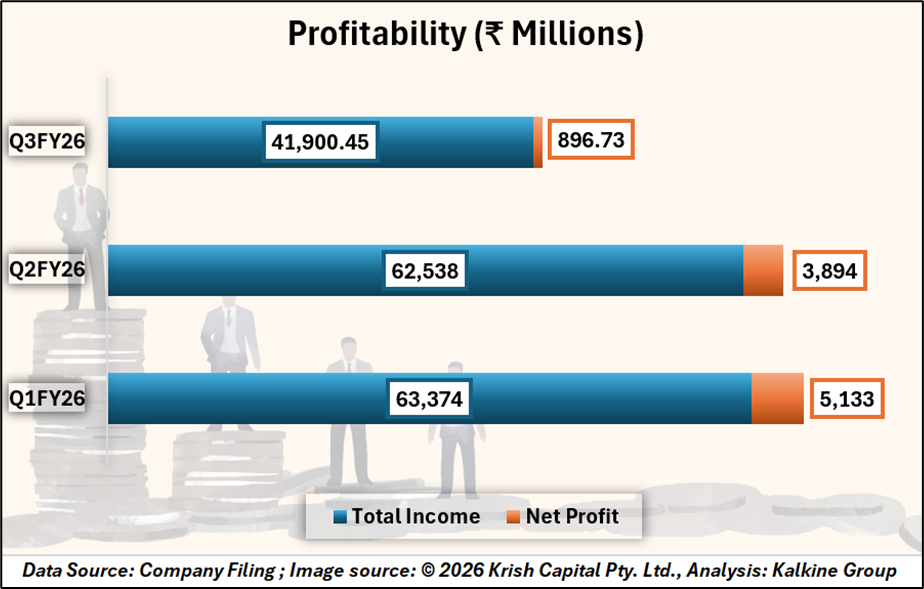

LG Electronics India Ltd reported revenue from operations of ₹41.14 Bn in Q3 FY26, marking a 6.4% decline compared to ₹43.96 Bn in Q3 FY25. On a sequential basis, revenue fell 33.4% from ₹61.74 Bn in Q2 FY26.

EBITDA for the quarter stood at ₹1.96 Bn, down from ₹3.40 Bn in the corresponding quarter last year. EBITDA margin contracted to 4.8% from 7.7% in Q3 FY25, reflecting subdued sales, operating leverage impact, higher input costs, and currency-related headwinds.

Profit before tax came in at ₹1.52 Bn versus ₹3.21 Bn a year earlier. Profit after tax declined to ₹0.90 Bn from ₹2.33 Bn in Q3 FY25.

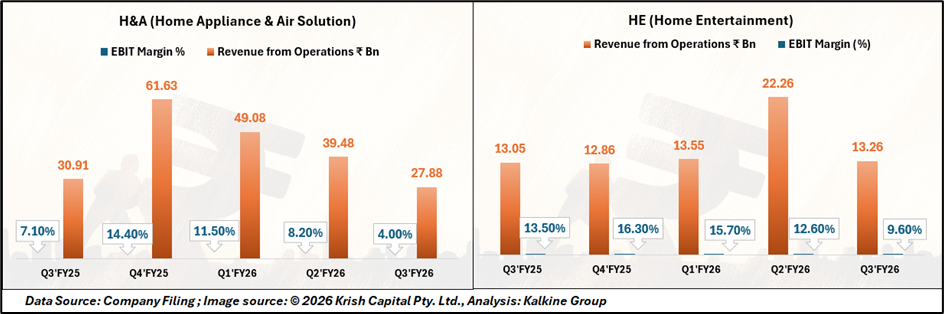

Segment Trends: Appliances Under Pressure, Entertainment Steady

The Home Appliance & Air Solution segment recorded revenue of ₹27.88 Bn in Q3 FY26, down 9.8% YoY. Segment EBIT margin narrowed to 4.0% from 7.1% in Q3 FY25, affected by lower volumes and elevated raw material prices, including copper and aluminium, alongside foreign exchange volatility.

The Home Entertainment segment posted revenue of ₹13.26 Bn, up 1.7% YoY. However, EBIT margin declined to 9.6% from 13.5% in the prior-year quarter, impacted by lower profitability in the Information Display business.

During the quarter, the company maintained offline value market share leadership across key categories, including televisions, refrigerators, room air conditioners, and washing machines.

Cash Flow and Balance Sheet Position

Cash flow from operating activities turned positive at ₹3.91 Bn in Q3 FY26, compared to negative ₹1.29 Bn in Q3 FY25. Cash and cash equivalents stood at ₹45.05 Bn at the end of the quarter, up from ₹34.65 Bn a year earlier.

For the nine months ended December 31, 2025, revenue from operations totaled ₹165.51 Bn, compared to ₹169.18 Bn in the corresponding period of the previous year.

Technical Summary

LG Electronics India Ltd (NSE) is trading near ₹1,469.00, down 3.28%, attempting a rebound after a recent corrective phase. The stock remains below its 51-day SMA at ₹1,492.99, which continues to act as immediate resistance. Price action shows a short-term recovery from the ₹1,350 zone, but the broader structure is still rebuilding after a series of lower highs.

The RSI (14) at 49.19 indicates neutral momentum, suggesting consolidation rather than directional strength. Immediate support is seen around ₹1,360, followed by ₹1,280, while resistance is placed near ₹1,580–₹1,670.

Margins Squeezed, Recovery Hinges on Demand Revival

LG Electronics India’s Q3 FY26 performance reflects margin pressure amid weaker demand, higher input costs, and currency headwinds. While revenue and profitability declined year-on-year, improved operating cash flow and a stronger cash position provide balance sheet comfort. Segment trends show resilience in Home Entertainment but continued stress in Appliances.

Technically, the stock is consolidating near key resistance, with neutral momentum indicating a wait-and-watch phase. Sustained recovery will likely depend on demand revival, cost stabilization, and improved operating leverage in the coming quarters.