Source: company BSE/NSE filings, NHAI project database, investor presentations.

Company Overview

G R Infraprojects Limited (GRIL) is an Udaipur-headquartered integrated EPC and infrastructure concessionaire, and one of the fastest-growing mid-to-large-cap names in the Indian road sector. Incorporated in 1995 and promoted by Mr. Vinod Kumar Agarwal, the company listed in 2021 via a successful IPO. Over the last two decades, GRIL has built a commanding presence in national-highway EPC and HAM projects and has rapidly diversified into adjacent infrastructure verticals.

The core strength of GRIL is vertical integration. Unlike many EPC peers that rely on third parties for core inputs, GRIL operates captive facilities for bitumen, emulsion, ready-mix concrete, road-marking paint, and metal-beam crash-barrier manufacturing, and owns a large fleet of modern construction equipment. This captive integration reduces dependency on external suppliers during input-cost volatility, improves margins, and accelerates execution timelines.

GRIL's business model combines two engines: the EPC revenue stream (build-and-handover contracts) and the HAM SPV portfolio (build-operate-transfer with NHAI annuity payments). Over time, GRIL has built one of the largest HAM portfolios among listed Indian contractors. Management intends to recycle mature HAM assets by divesting them to InvITs, freeing capital for new bids.

Revenue StreamsS — Seven Operating Verticals

HAM Capital-Recycling Cycle — GRIL's Balance-Sheet Engine

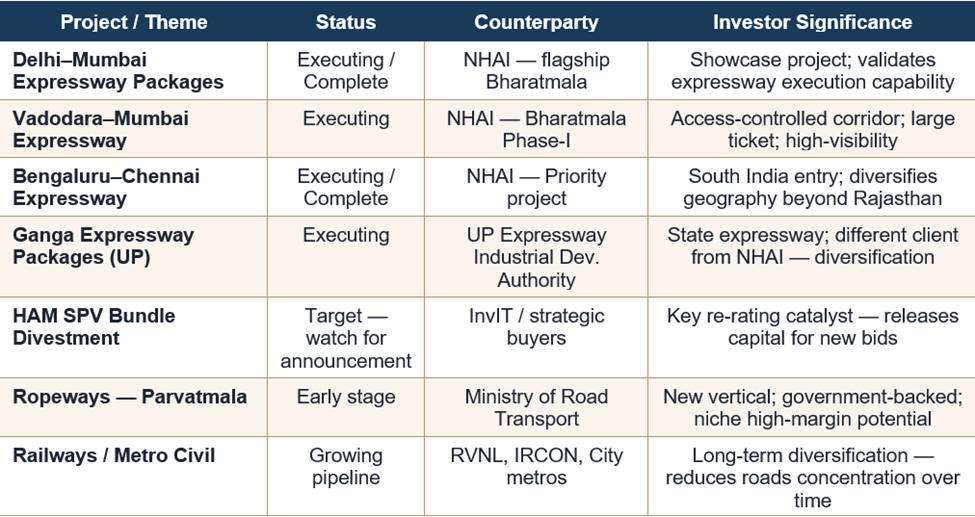

Flagship Project Themes — Status & Investor Significance

Financial Performance

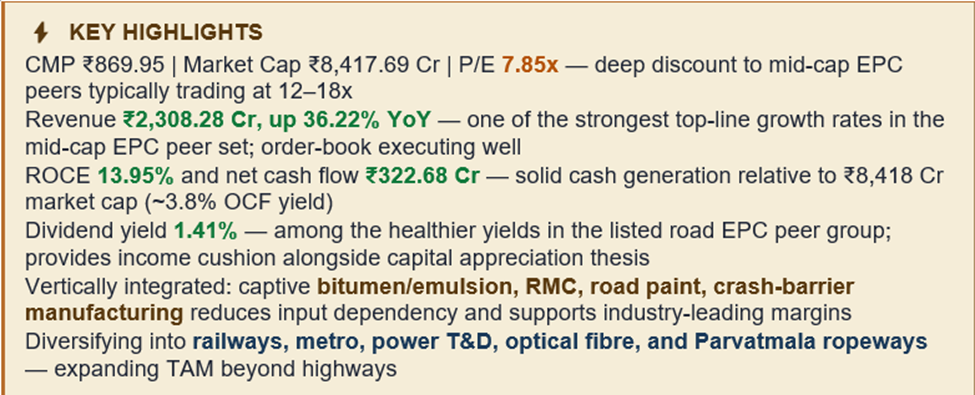

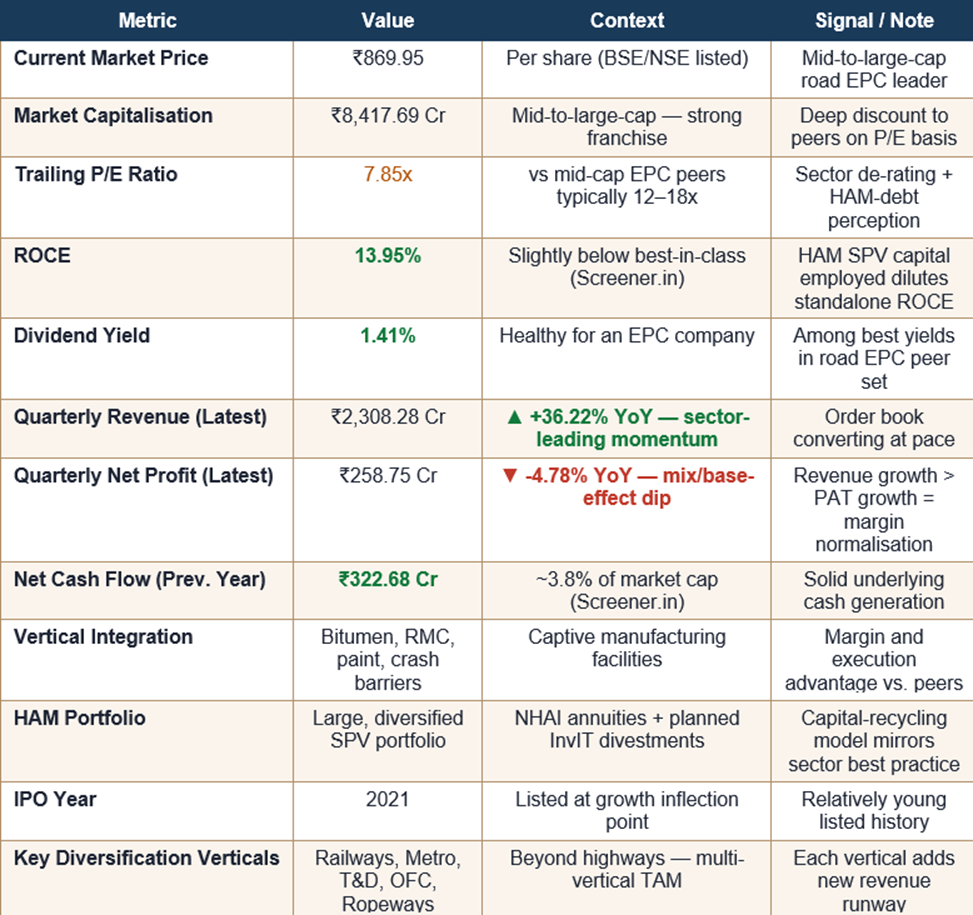

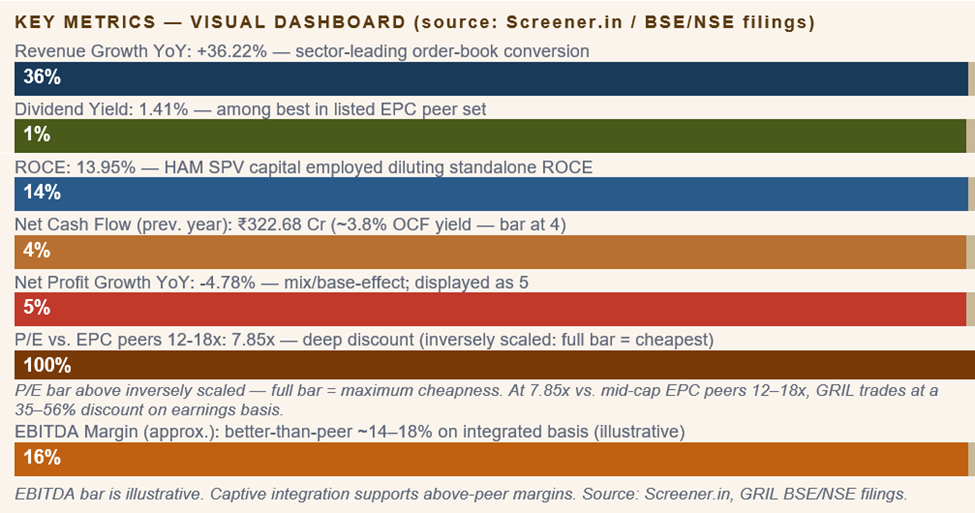

GRIL's latest quarterly print shows revenue of ₹2,308.28 Cr, up a strong 36.22% YoY — one of the strongest top-line growth rates in the mid-cap EPC peer set, reflecting successful conversion of order book into execution. Net profit of ₹258.75 Cr was down 4.78% YoY, a modest dip likely related to mix normalisation from a prior-year quarter that may have included a HAM-divestment or one-off gain.

ROCE of 13.95% is slightly below the best-in-class mid-cap EPC peers but is respectable given the larger share of HAM capital employed on the balance sheet — HAM SPV equity, if stripped out, would leave the standalone EPC ROCE significantly higher. Net cash flow of ₹322.68 Cr is robust relative to the ₹8,418 Cr market cap, implying a ~3.8% operating cash-flow yield.

The dividend yield of 1.41% is one of the healthier profiles among listed road contractors, adding a yield cushion to the total-return profile. Balance sheet: GRIL carries meaningful HAM-related debt at the SPV level, which is non-recourse in structure and backed by contracted NHAI annuities; parent-level leverage is more moderate.

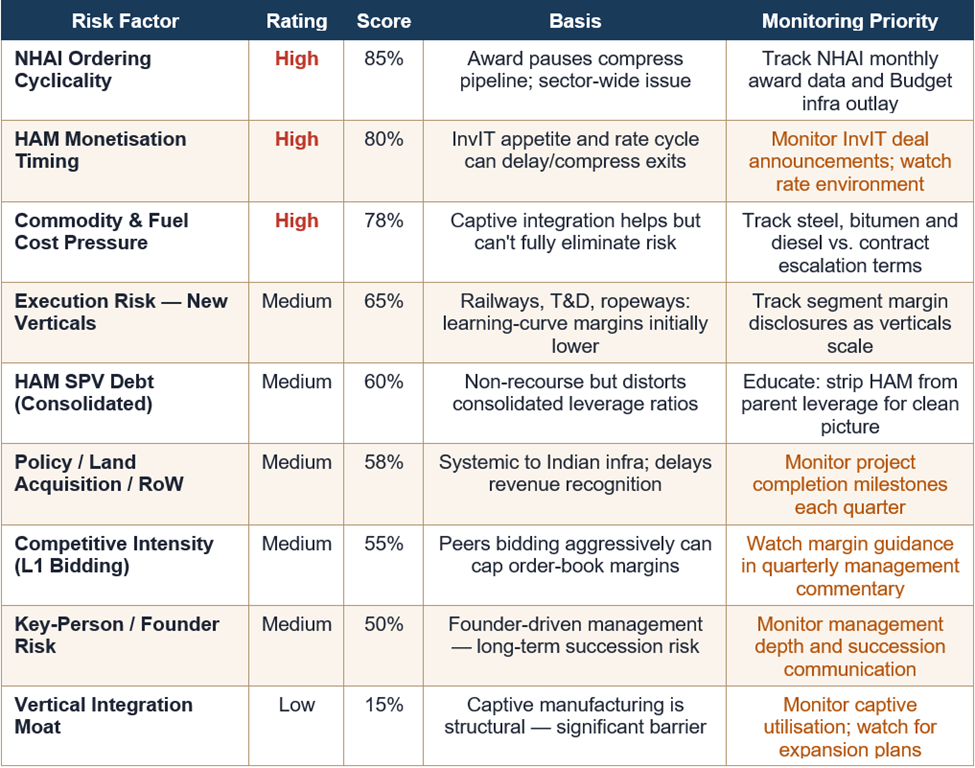

Risk Scorecard — G R Infraprojects

Risk ratings are qualitative assessments based on data, BSE/NSE filings, and sector analysis.

Key Risks

1 — NHAI Ordering Cyclicality

Like all road EPC companies, GRIL's forward order visibility depends heavily on the pace of NHAI awards. Slow award years compress the future pipeline regardless of how well the current book executes. This is the most important external macro variable — tracking NHAI monthly awards and Ministry of Road Transport budget allocations is essential.

2 — HAM Monetisation Risk

The capital-recycling model depends on being able to divest mature HAM assets at attractive valuations via InvITs or strategic buyers. Weakness in infra-funds appetite, rising interest rates, or adverse tax policy could delay or compress monetisation outcomes. The timing of any HAM bundle announcement will be a significant price catalyst.

3 — Commodity and Fuel Cost Pressure

Steel, cement, bitumen and diesel together account for a significant share of EPC costs. While GRIL's captive manufacturing reduces dependency on external suppliers for some inputs, fixed-price contracts still carry residual exposure to sharp commodity up-cycles. Contracts with adequate escalation clauses partially mitigate this.

4 — Other Key Risks

- New vertical execution: Entry into railways, metro, T&D, optical fibre, and ropeways is strategically sound but brings learning-curve risks — initial margins in new segments can be lower than mature highway work.

- HAM SPV debt perception: HAM-level debt, though non-recourse, shows up in consolidated financials. Investors should adjust for this when comparing leverage ratios with pure-EPC peers.

- Competitive intensity: Indian road EPC has become intensely competitive. Aggressive L1 bids from peers can cap order-book margins.

- Key-person risk: Strong founder-driven companies benefit from promoter focus but are exposed to key-person succession risk over the long term.

Valuation

At CMP ₹869.95 and trailing P/E of 7.85x, GRIL trades at a significant discount to its peer set. Mid-cap peers with comparable order-book strength trade at 12–18x. Given GRIL's sector-leading 36% revenue growth, vertical integration moat, and 1.41% dividend yield, the valuation gap appears wider than fundamentals justify.

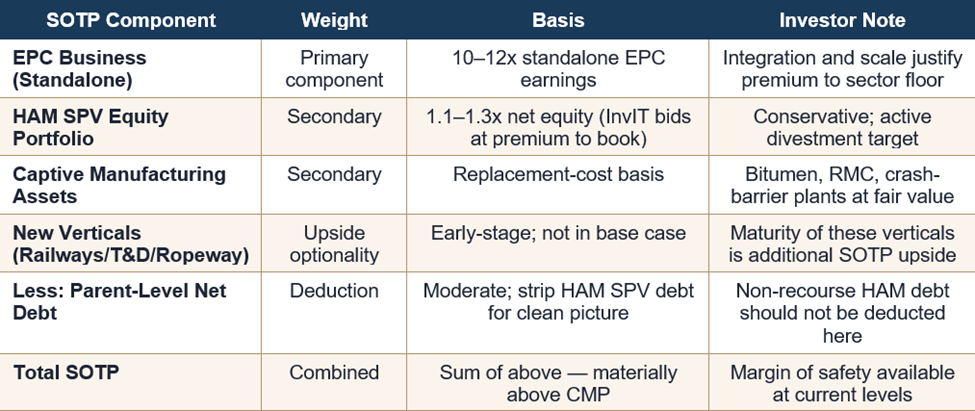

SOTP Valuation Framework

Price Performance

Since its 2021 listing, GRIL's share price has broadly tracked the infrastructure sector cycle. The current CMP of ₹869.95 reflects a period where the strong operational momentum (+36% revenue) has not yet been fully captured in the market multiple, creating a gap between financial performance and market pricing that patient investors may find attractive.

The 1.41% dividend yield provides a real cash return while the re-rating thesis plays out. For investors who entered at the IPO, the total-return profile includes both the dividend income and any capital appreciation since listing.

Frequently Asked Questions

Q1. What does G R Infraprojects do?

GRIL is an integrated road EPC contractor and HAM concessionaire, also operating in railways, metro, power T&D, optical fibre, and ropeways. It owns captive manufacturing facilities for bitumen/emulsion, RMC, road-marking paint, and metal-beam crash barriers — a key differentiator from peers.

Q2. Why is GRIL's P/E only 7.85x?

Sector-wide de-rating in Indian road EPC, investor caution on HAM-driven consolidated debt, and some overhang from the modest PAT decline in the latest quarter. Given strong revenue growth and vertical integration, the multiple appears conservative relative to fundamentals.

Q3. What is GRIL's revenue growth like?

Latest quarterly revenue grew 36.22% YoY — one of the strongest prints in the mid-cap EPC peer group. This reflects successful order-book conversion and broad-based execution across multiple expressway and HAM packages.

Q4. Does GRIL pay dividends?

Yes, with a dividend yield of approximately 1.41% — among the healthier yields in the EPC peer set. This provides an income cushion alongside the capital-appreciation thesis.

Q5. What is the HAM model and why does it matter for GRIL?

Under the Hybrid Annuity Model, GRIL builds highways via SPVs that receive NHAI annuity payments over the concession period. Mature HAM assets are planned for divestment via InvITs to recycle capital into new bids — the same build-sell-redeploy flywheel used by other top-tier EPC players.

Q6. Is GRIL's balance sheet concerning?

Consolidated leverage looks elevated because HAM SPV debt is included, but this debt is non-recourse and backed by contracted NHAI annuities. Parent-level leverage is moderate. Investors should analyse standalone and consolidated financials separately to get a clean view.

Q7. What are the biggest risks?

NHAI ordering volatility, HAM monetisation timing, commodity-cost pressure, execution risk in new verticals (railways, T&D, ropeways), and sector-wide competitive intensity. See the Risk Scorecard above for a structured assessment.

Q8. How is GRIL different from other road EPC peers?

Vertical integration into captive inputs (bitumen, RMC, paint, crash barriers), a larger HAM portfolio than most peers, and active diversification into railways, metro, T&D, fibre, and ropeways — each adding a new revenue stream over time.

Q9. Is GRIL a good long-term investment?

It suits long-duration investors positive on the Indian infrastructure capex cycle, seeking scale, execution track record, vertical integration advantage, and a reasonable dividend yield at a value multiple. Patience on HAM InvIT monetisation is required.

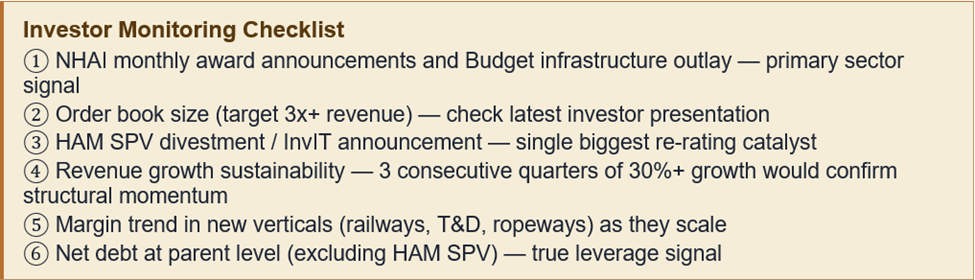

Q10. Where can I find GRIL's latest financials and order book?

On the company's investor-relations website, BSE/NSE filings, quarterly investor presentations, The investor presentation is the most useful source for order-book and project-level updates.