Source: Company BSE/NSE filings, NHAI project database, investor presentations.

Company Overview

KNR Constructions Limited is a Hyderabad-headquartered infrastructure construction company incorporated in 1995 and promoted by Mr. K. Narasimha Reddy. Over nearly three decades, KNR has established itself as one of India's most operationally efficient mid-cap highway EPC contractors, specialising in national highways, expressways, bridges, flyovers, and irrigation projects.

KNR's hallmark is disciplined project selection and on-time execution. Unlike many EPC peers that chased order-book growth at the cost of margins and balance-sheet strength during the 2010s, KNR has historically been selective about bids, avoided over-leverage, and maintained one of the cleanest balance sheets in the roads sector. This conservatism is reflected in its consistently high ROCE, low debt-to-equity, and positive operating cash flows across cycles.

The company operates across two broad streams: pure EPC contracts (build and hand over) and HAM (Hybrid Annuity Model) projects for NHAI, where it builds, owns during the concession period, and receives annuity payments. KNR monetises mature HAM assets by divesting them to infrastructure investment trusts (InvITs) and strategic buyers, recycling capital into new projects — a model pioneered effectively by only a handful of Indian infra companies.

HAM Capital-Recycling Model — KNR's Key Differentiator

The HAM capital-recycling cycle is what separates KNR from generic EPC players. By divesting mature SPVs rather than holding them through the full concession life, KNR recovers its equity faster, limits balance-sheet drag and redeploys capital at higher-ROCE entry points — effectively operating as a build-sell-redeploy infrastructure compounder rather than a pure constructor.

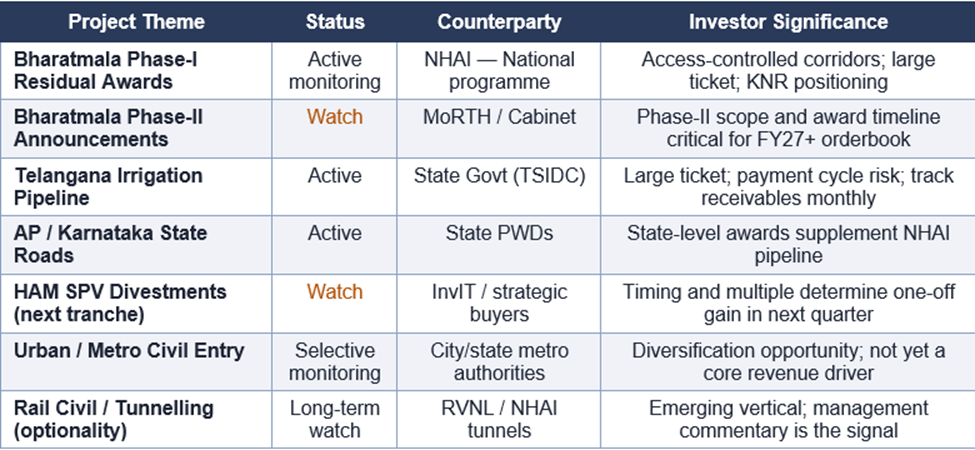

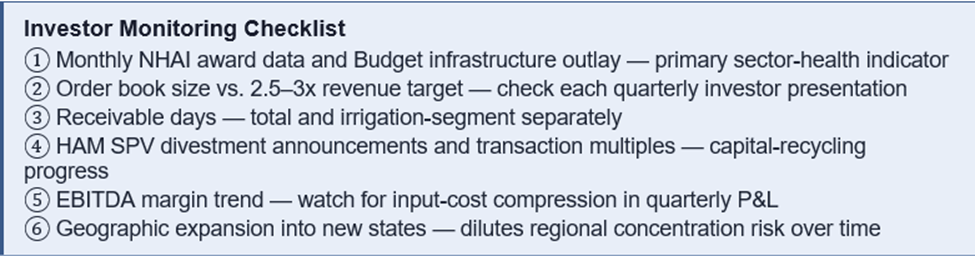

Key Projects & Pipeline — What to Monitor

Financial Performance

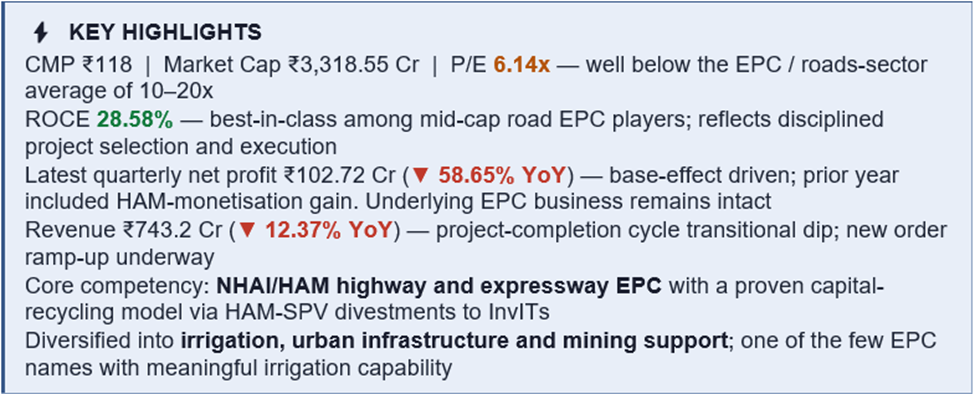

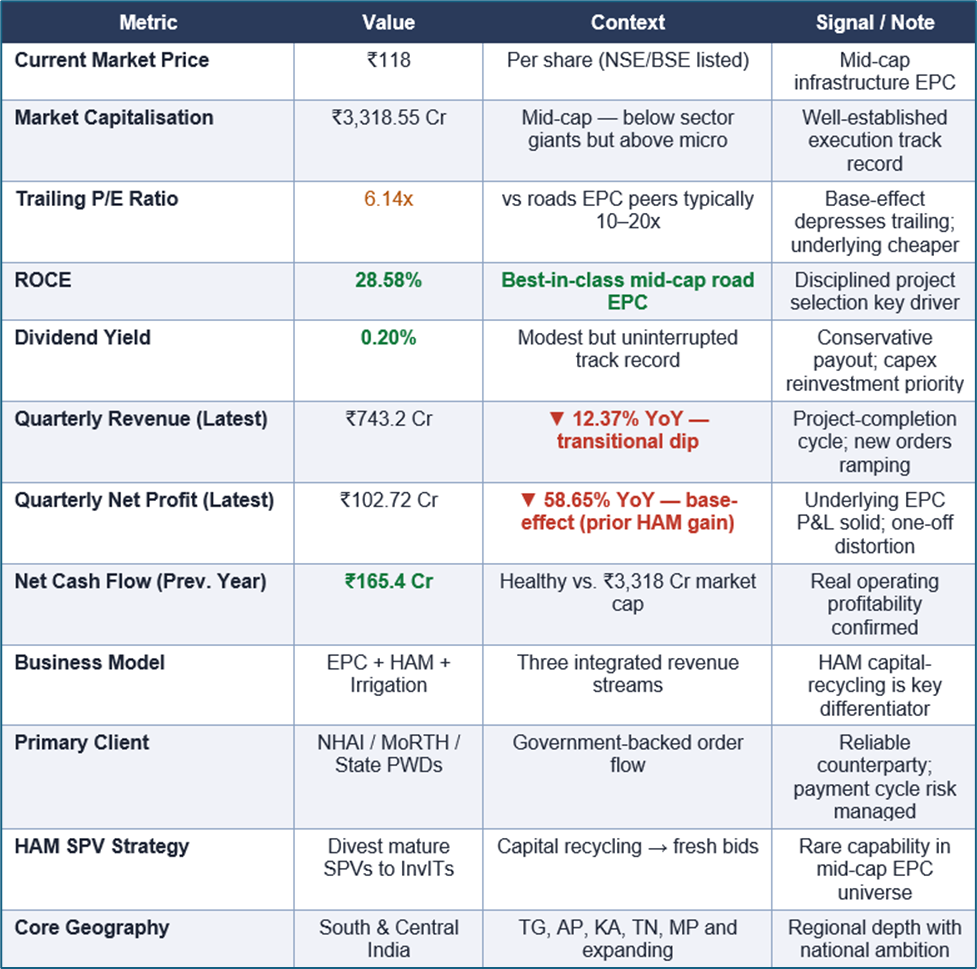

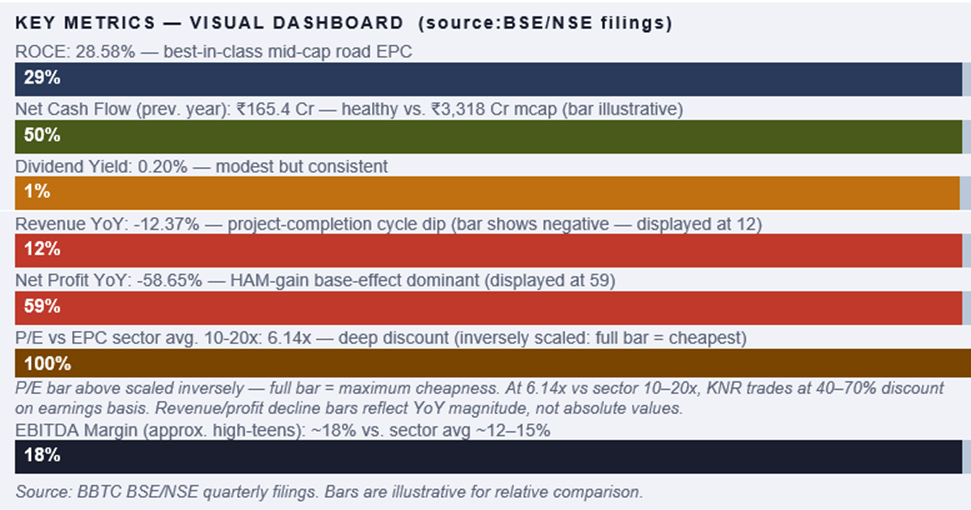

KNR's latest quarterly print shows consolidated revenue of ₹743.2 Cr, down 12.37% YoY, and net profit of ₹102.72 Cr, down 58.65% YoY. These headline numbers require careful interpretation — the YoY decline in profit is primarily a base-effect: the prior-year comparison quarter included a significant one-off gain from the divestment of a HAM SPV stake. Stripping that gain out, the underlying EPC business performance is materially better than the headline YoY suggests.

Structural strengths visible in the numbers are important context: ROCE of 28.58% is exceptional in a sector where many peers earn mid-teens at best. Cash generation of ₹165.4 Cr (previous year, at operating level) is healthy relative to the ₹3,318 Cr market cap, indicating real underlying profitability rather than accounting profits. EBITDA margins in the high-teens to low-twenties compare favourably with peers in the 10–15% range.

Revenue softness often reflects project-completion cycles — as legacy projects complete and new orders ramp up, quarterly revenue can dip temporarily. The most important forward indicator for an EPC company is not the current quarter's revenue but the order book and inflow trend, which investors should verify from the latest investor presentation.

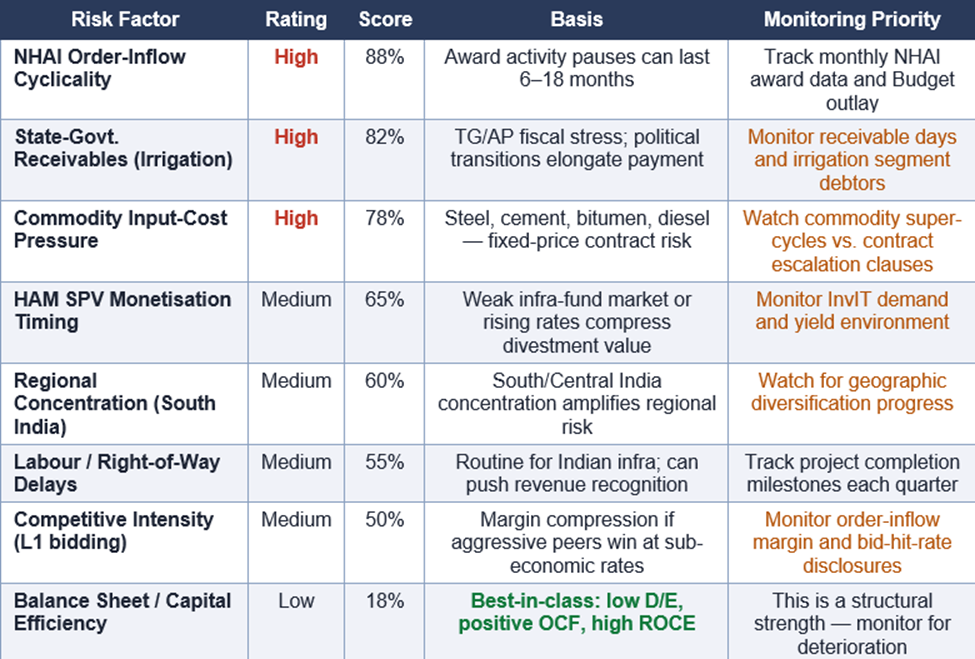

Risk Scorecard — KNR Constructions

Risk ratings are qualitative assessments based on BSE/NSE filings, and sector analysis.

Key Risks

1 — Order-Inflow Volatility (NHAI Cyclicality)

NHAI ordering activity has historically been cyclical — strong years followed by pauses for policy review or fiscal consolidation. Slow award activity delays revenue visibility across the entire roads EPC sector. KNR's strong track record and pre-qualification credentials provide an edge in competitive bids, but a sector-wide slowdown affects it alongside peers.

2 — State-Government Receivables (Irrigation)

Irrigation projects, particularly in Telangana, carry elevated payment risk during state fiscal stress or political transitions. Delayed payments stretch working capital and can trigger impairments. Investors should track the irrigation-segment debtor days separately from the highways segment each quarter.

3 — Commodity Cost Pressure

Steel, cement, bitumen and diesel are major cost inputs. Fixed-price EPC contracts without adequate price-escalation clauses expose margins during commodity up-cycles. KNR's project-selection discipline includes careful review of escalation terms, but sharp commodity spikes — such as steel surges — can still pressure margins on contracts in mid-execution.

4 — HAM Monetisation Timing

The capital-recycling model depends on being able to divest mature HAM assets at attractive valuations. A weak infra-funds market or rising interest rates can compress divestment multiples. Any mismatch between when KNR needs capital for new bids and when it can sell SPV stakes at acceptable prices creates a timing risk.

5 — Other Risks

- Concentration risk: South and Central India execution footprint means regional disruptions affect a larger share of the book.

- Competitive intensity: Aggressive L1 bidders can compress order inflows even when KNR doesn't compromise on its own bid discipline.

- Labour and execution risk: Land acquisition, right-of-way, and local disruptions are endemic to large Indian civil projects.

- Regulatory / policy risk: Changes in NHAI payment norms, arbitration processes, or HAM model parameters directly affect sector economics.

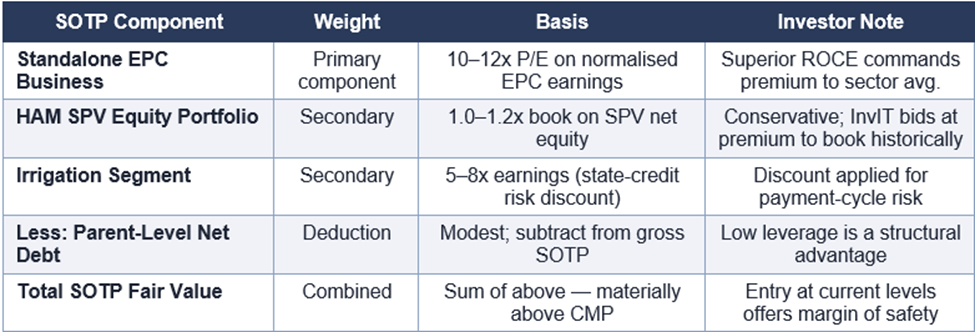

Valuation

At CMP ₹118 and trailing P/E of 6.14x, KNR trades at a meaningful discount to the Indian roads EPC peer set, which generally trades in a 10–20x earnings band. Given KNR's superior ROCE (28.58% vs. 12–15% for many peers), cleaner balance sheet, and proven capital-recycling capability, the valuation gap appears wider than fundamentals justify.

SOTP Valuation Framework

Key re-rating catalysts: (1) strong NHAI order awards, (2) visible ramp-up in order book toward 3x revenue, (3) successful HAM bundle monetisation at healthy multiples, (4) entry into new verticals (metro civil, rail civil, tunnelling). Consistent delivery on these unlocks the valuation gap; any setback on order flow extends the discount period.

Price Performance

KNR's share price trajectory has broadly tracked the Indian roads-sector EPC cycle — strong phases during peak NHAI award years, followed by de-rating during order-flow pauses. The current CMP of ₹118 reflects a period of softer reported earnings (driven by the HAM-gain base effect) and some uncertainty around order-book momentum.

For long-term investors, the key observation is that operational ROCE has remained high through this period, suggesting that the underlying business is healthy and the share-price weakness is sentiment-driven rather than fundamental. Dividend yield of 0.20% provides a modest income return while the thesis plays out.

Frequently Asked Questions

Q1. What does KNR Constructions do?

KNR Constructions is a Hyderabad-based infrastructure EPC company that primarily builds national highways, expressways, bridges, flyovers, and irrigation projects for NHAI, MoRTH, and state governments across India — particularly South and Central India.

Q2. Why is KNR's P/E only 6.14x?

The low P/E reflects (a) the broader de-rating in mid-cap EPC names during periods of slow NHAI ordering, (b) lumpiness in reported profits due to HAM-monetisation gains in prior years inflating the base, and (c) sector-wide concerns on working capital. Given the strong ROCE, the valuation appears conservative on a normalised earnings basis.

Q3. What is KNR's ROCE and why does it matter?

KNR's ROCE is 28.58% — significantly higher than most road EPC peers. It reflects strong project-selection discipline, efficient execution, and a low-capital-intensity operating model. High ROCE in EPC indicates the company is not chasing revenue at the cost of returns — a key quality screen.

Q4. What is the HAM model and how does KNR use it?

Under the Hybrid Annuity Model, the concessionaire (KNR SPVs) builds the road with a mix of NHAI upfront grants (40%) and its own equity/debt (60%), then receives semi-annual annuity payments from NHAI over the concession period. KNR later divests mature HAM SPVs to InvITs or infra funds to free up equity capital for fresh bids — a build-sell-redeploy model.

Q5. Is KNR financially strong?

Yes. KNR maintains one of the cleaner balance sheets in the sector, with moderate leverage, healthy operating cash flows (₹165.4 Cr in the previous year), and a track record of dividend payment. The ROCE of 28.58% confirms the underlying quality of the business.

Q6. What are the biggest risks?

Order-inflow volatility from NHAI, state-government receivables (especially irrigation), commodity cost pressure on fixed-price contracts, HAM monetisation timing risk, and regional concentration in South/Central India. See the Risk Scorecard above for a structured view.

Q7. Is KNR a good long-term investment?

For investors positive on India's long-term highway and infrastructure capex cycle and comfortable with EPC cyclicality, KNR is one of the higher-quality mid-cap options offered at a reasonable valuation. Patient capital and a 2–3-year horizon are prerequisites.

Q8. What are the re-rating catalysts?

A strong pick-up in NHAI highway awards, an expanded order book toward 2.5–3x revenue, successful HAM asset divestments at healthy InvIT multiples, entry into adjacent civil-infrastructure verticals like metro and rail, and sustained EBITDA-margin delivery above peers.

Q9. Where can I find KNR's latest order book and results?

From the company's investor-relations page, BSE/NSE filings (quarterly results and investor presentations), NHAI's public award data. The quarterly investor presentation is the most useful source for order-book and project-level updates.

Q10. Does KNR pay dividends?

Yes, KNR pays modest dividends. Current dividend yield is approximately 0.20%, reflecting a conservative payout policy focused on reinvesting into new projects and HAM bids.