Source: company BSE/NSE filings, NHPC/SJVN project announcements.

Company Overview

Patel Engineering Limited is one of India's oldest and most specialised infrastructure construction companies, incorporated in 1949. Over more than seven decades, the company has built a reputation as the go-to contractor for complex hydropower, dam and underground tunnelling projects — some of the most technically demanding categories in Indian civil engineering. Patel Engineering has contributed to dozens of large hydroelectric projects across India, Nepal, Bhutan and other geographies, and owns one of the largest fleets of specialised tunnelling and heavy civil equipment in the country.

The company's core differentiation lies in its deep technical capability. Tunnelling, underground powerhouses, large concrete dams, and high-head hydropower works require decades of know-how, specialised equipment like TBMs (Tunnel Boring Machines), and experienced project teams. Very few Indian players possess this combination. Patel Engineering is among the handful recognised by NHPC, SJVN, THDC, NEEPCO, state hydro utilities and international multilaterals as a pre-qualified contractor for such work.

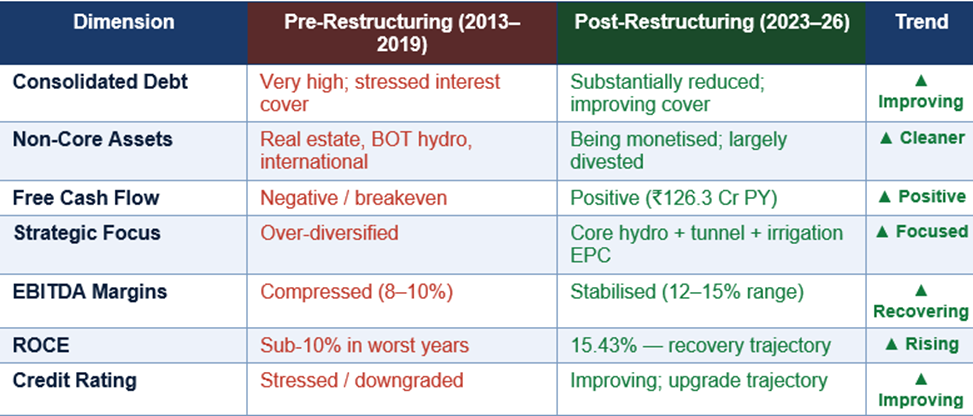

Historically, Patel Engineering suffered from over-diversification and excessive leverage during the 2000s. Over the last several years, management has pursued a comprehensive restructuring: non-core assets monetised or divested, debt substantially reduced, and strategic focus restored squarely to core EPC work in hydro, dams, tunnels, irrigation and urban infrastructure. The company is now generating positive free cash flow and rebuilding ROCE — a turnaround story that the market has partially but not fully priced in.

Balance-Sheet Restructuring — Before vs. After

|

⚡ Key Optionality — Pumped-Storage Hydropower (PSP) India's 500 GW renewable energy target by 2030 creates a critical need for grid-firming storage. Pumped-storage hydropower (PSP) — where water is pumped uphill using surplus solar/wind power and released to generate electricity during peak demand — is the most scalable and cost-effective long-duration storage solution available. India has a pipeline of hundreds of gigawatts of PSP projects in various stages of planning. Patel Engineering's underground powerhouse and high-head tunnelling capability is directly applicable to PSP projects. The company has executed technically similar work at major hydro projects. With very few listed Indian EPC companies able to execute PSP-scale underground civil work, Patel Engineering's franchise could see a step-change in order-book quality if the PSP ordering wave accelerates as expected over FY26–FY30. |

Financial Performance

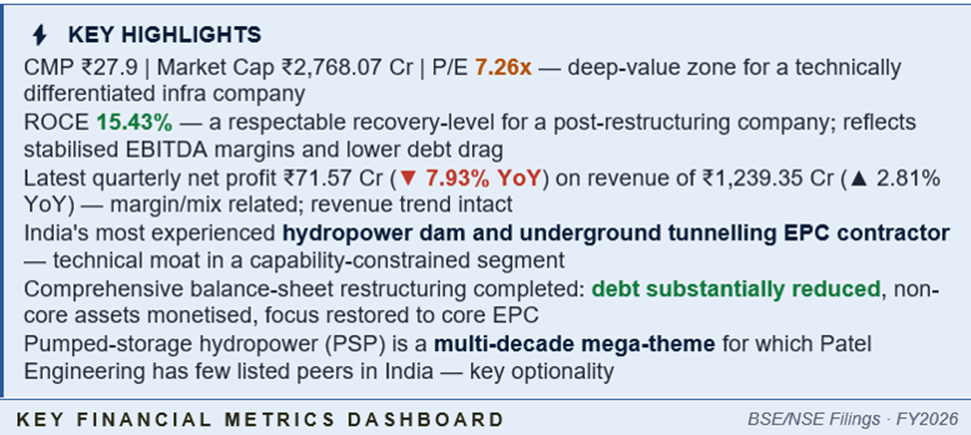

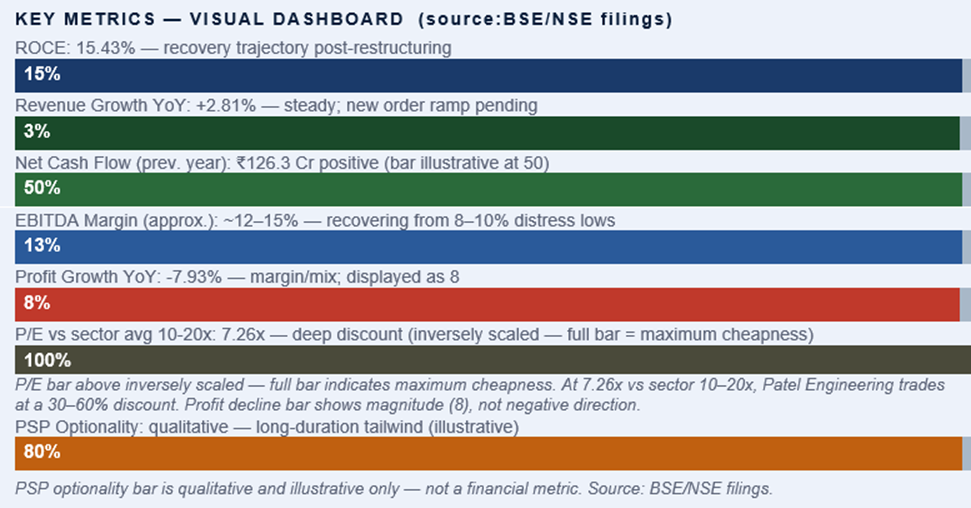

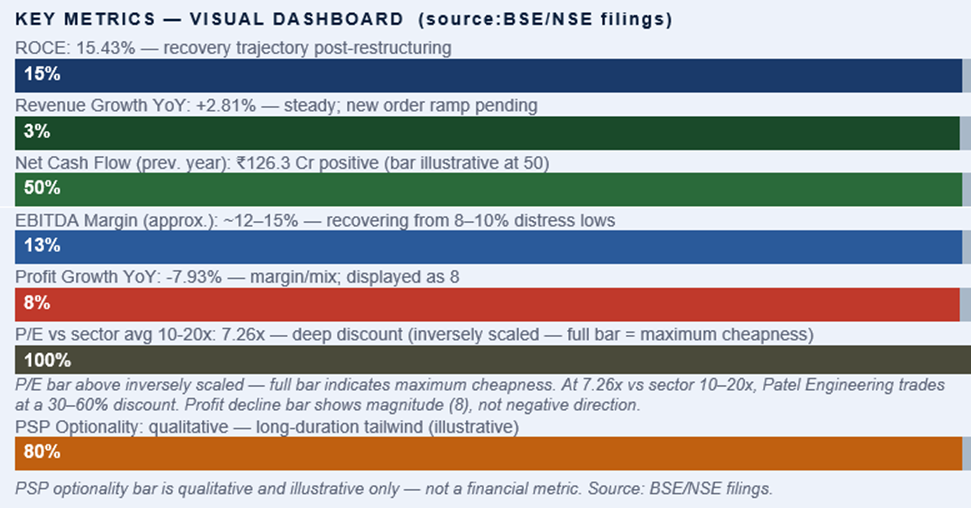

Patel Engineering's latest quarterly print shows revenue of ₹1,239.35 Cr, up 2.81% YoY, and net profit of ₹71.57 Cr, down 7.93% YoY. The profit decline is margin- and mix-related rather than a structural reversal — reflecting the typical lumpiness of large hydro and tunnelling projects where revenue phasing and cost recognition can move quarterly profits meaningfully.

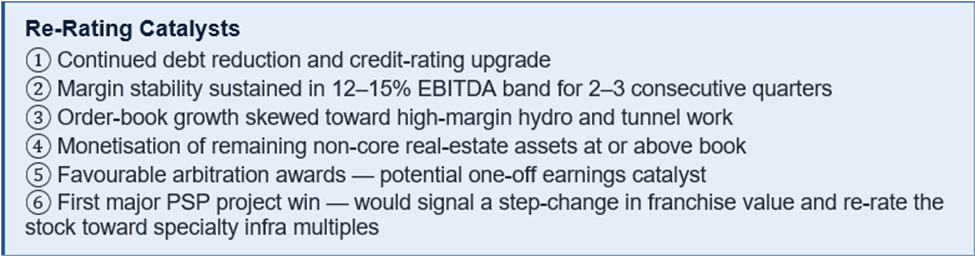

The structural recovery is clearly visible in the broader trend. ROCE of 15.43% is a respectable recovery level for a post-restructuring infra company. Net cash flow of ₹126.3 Cr in the previous year confirms real cash generation rather than paper profits. EBITDA margins have stabilised in the 12–15% range — materially better than the 8–10% range during the distress years, though still below the 17–20% peak achievable on a fully de-levered balance sheet.

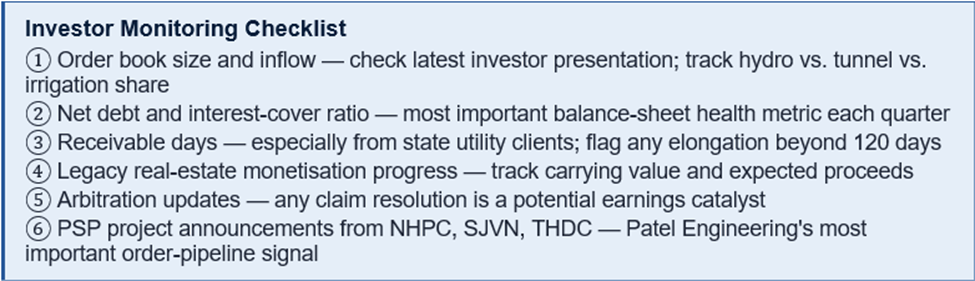

Order book: Patel Engineering historically targets an order book of ~3–4x revenue, offering strong multi-year revenue visibility. The current order book should be checked from the latest investor presentation, with particular attention to the share of high-margin hydro and tunnelling work vs. lower-margin irrigation and urban packages.

|

FINANCIAL PERFORMANCE & RISK SCORECARD |

BSE/NSE Filings · FY2026 |

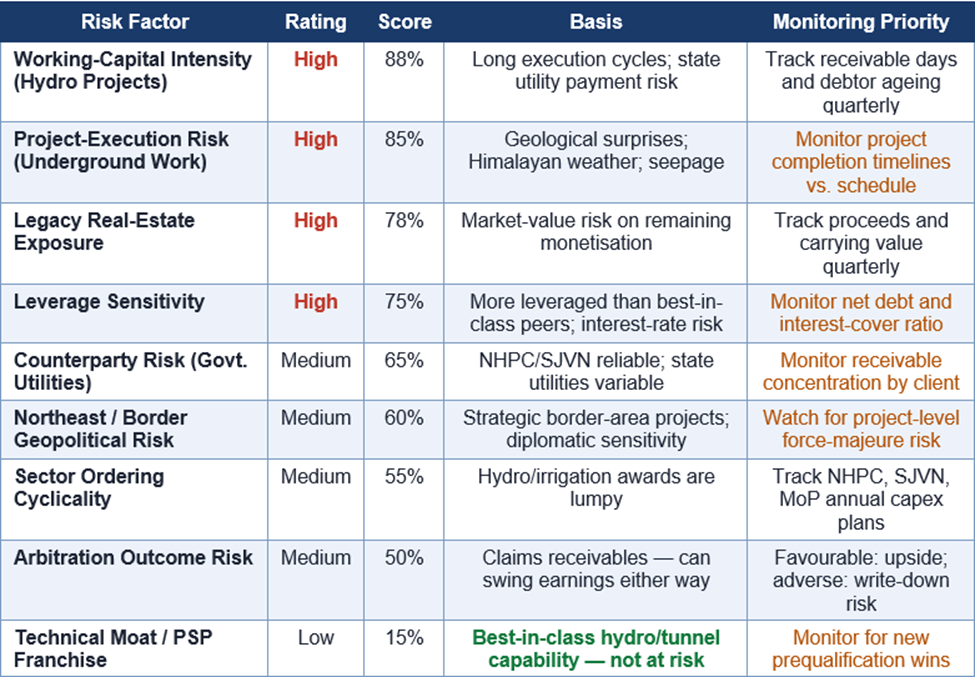

Risk Scorecard — Patel Engineering

Risk ratings are qualitative assessments based on BSE/NSE filings, and sector analysis.

Key Risks

1 — Working-Capital Intensity

Hydro, dam and tunnel projects have long execution cycles and elevated working-capital needs. Any stretch in client payment cycles — especially from state utilities — can strain liquidity. This is the most important ongoing monitoring metric: receivable days and the ageing of outstanding dues from state hydro utilities should be checked every quarter.

2 — Project-Execution Risk (Underground Work)

Large underground works are inherently risky. Geological surprises, seepage, cavity collapses, and weather disruptions in the Himalayas can delay completion and invoke cost overruns. While Patel Engineering's experience is the best available in India, no contractor is immune to geological risk in complex mountain environments.

3 — Legacy Real-Estate Exposure

Although being monetised, any adverse real-estate market movement could affect the valuation realised on remaining legacy assets. If market conditions deteriorate before the assets are sold, the proceeds could be below current book estimates, reviving balance-sheet concerns.

4 — Leverage Sensitivity

While debt has come down, the business remains more leveraged than best-in-class peers. Any sharp rise in interest rates or execution slippage could revive balance-sheet concerns. The improving interest-cover trajectory is the key metric to watch — any deterioration is an early warning signal.

5 — Other Risks

- Geopolitical risk: Some hydro and tunnelling work is in strategically sensitive border regions of the Northeast and J&K.

- Sector ordering cyclicality: Government hydro and irrigation ordering can be lumpy; slow award years affect order-book momentum.

- Arbitration outcomes: Meaningful claims and arbitration receivables outstanding — favourable outcomes are upside; adverse rulings are downside.

- Competition: While the moat is real, Chinese and Korean TBM contractors and aggressive domestic entrants can create bidding pressure.

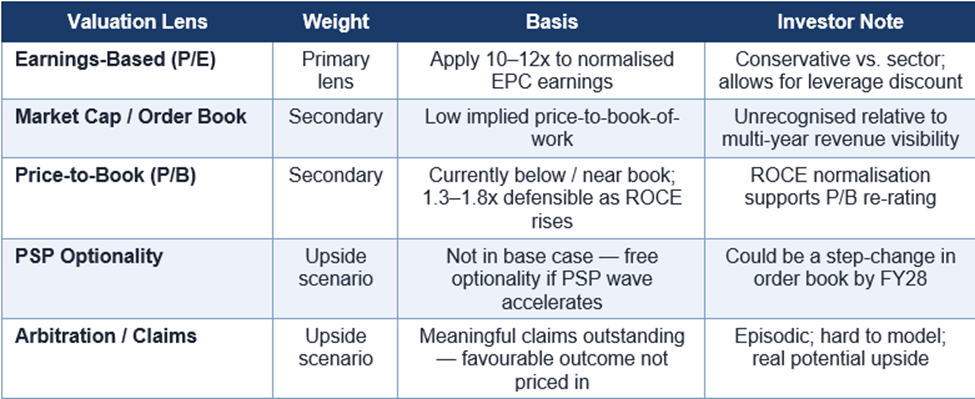

Valuation

At CMP ₹27.9 and trailing P/E of 7.26x, Patel Engineering trades at a clear deep-value multiple relative to the wider infra EPC peer set. Even applying a conservative 10–12x multiple — well below market averages — suggests meaningful re-rating potential if earnings sustain.

Price Performance

Patel Engineering's share price has broadly reflected the company's restructuring journey — weak during the 2013–2019 period of stress, gradually recovering as debt declined and profitability stabilised. At ₹27.9, the stock remains at levels that offer asymmetric upside if the PSP optionality materialises.

Dividend yield is 0% — management has deliberately prioritised debt reduction over dividends. For income-oriented investors this is a limitation; for capital-appreciation investors it is a positive signal that incremental cash is being deployed constructively.

Frequently Asked Questions

Q1. What does Patel Engineering do?

Patel Engineering is one of India's oldest infrastructure companies, specialising in hydropower projects, dams, underground tunnels, irrigation works and urban infrastructure. It is particularly known for technically complex hydro and tunnelling projects executed for NHPC, SJVN, THDC, NEEPCO, and state hydro utilities.

Q2. Why is Patel Engineering's P/E only 7.26x?

The deep-value multiple reflects the market's residual caution after the company's extended restructuring period, its historical leverage, and the inherent cyclicality of infrastructure ordering. As the balance sheet continues to strengthen and ROCE improves, the multiple has room to normalise toward 10–12x.

Q3. Is Patel Engineering profitable?

Yes. Latest quarterly net profit was ₹71.57 Cr on revenue of ₹1,239.35 Cr, with ROCE of 15.43% and positive operating cash flow of ₹126.3 Cr in the previous year. The business has emerged from its restructuring as a profitable, cash-generating entity.

Q4. Does Patel Engineering pay dividends?

Currently no. Management is prioritising debt reduction and redeployment of cash into working capital for new orders. This is a deliberate and rational policy choice — zero dividend signals discipline, not distress.

Q5. What are Patel Engineering's biggest risks?

Working-capital intensity on long-cycle hydro and tunnel projects, project-execution delays due to geological and weather risk in the Himalayas, payment cycles from government clients, legacy real-estate exposure, and ongoing leverage sensitivity. See the Risk Scorecard for a structured assessment.

Q6. Why is Patel Engineering well-positioned in pumped-storage hydropower?

India's energy transition requires large-scale pumped-storage hydropower (PSP) to firm up intermittent solar and wind power. PSP projects require underground powerhouses, high-head tunnels, and large dam civil work — exactly what Patel Engineering specialises in. With very few listed Indian EPC companies able to execute PSP-scale underground civil work, Patel Engineering faces limited direct competition for these orders.

Q7. What is the company's current order book?

Patel Engineering typically operates with an order book of ~3–4x annual revenue, offering strong multi-year visibility. Exact current figures should be checked from the latest investor presentation and quarterly results on BSE/NSE.

Q8. Has Patel Engineering reduced its debt?

Yes, significantly. Over the past several years, the company has monetised non-core assets, tightened working capital, and generated positive free cash flow, all of which have contributed to a substantial reduction in consolidated debt. This process is ongoing but the hardest phase appears complete.

Q9. Is Patel Engineering a good long-term investment?

It is a special-situations / deep-value opportunity suited to patient investors who are positive on Indian hydro, tunnelling and water-infrastructure capex, and comfortable with the residual risks around leverage and execution. The PSP optionality is a potential multi-year re-rating catalyst not widely priced in.

Q10. Where can I find Patel Engineering's latest results?

On the company's investor-relations website, BSE/NSE filings (quarterly results and investor presentations). NHPC, SJVN and MoP (Ministry of Power) publications are useful for tracking the hydro/PSP ordering pipeline.