Source: company BSE/NSE filings (BSE code 501425), BBTC annual reports. All figures approximate and point-in-time.

Company Overview

The Bombay Burmah Trading Corporation Limited (BBTC) is one of the oldest publicly listed companies in India, incorporated in 1863. Originally set up to trade Burmese teak, it has transformed over 160 years into a diversified conglomerate and the principal holding vehicle of the Wadia Group for its interests in the food, plantation, auto-electricals and real-estate businesses.

BBTC's corporate structure makes it unique on Indian bourses. While the company runs its own operating businesses — tea, coffee, healthcare, auto-electricals, horticulture and real estate — the dominant driver of its consolidated financials is its roughly 50.5% controlling stake in Britannia Industries Limited, one of India's largest and most profitable packaged-foods companies. Because BBTC consolidates Britannia's revenues and profits into its own accounts under Indian accounting standards, the company's reported top-line of over ₹5,000 Cr per quarter is largely a reflection of Britannia's scale rather than BBTC's standalone operations.

This dual identity — operating company plus holding company — is central to understanding BBTC as an investment. On one hand, the consolidated numbers look like an FMCG powerhouse; on the other, the standalone business is a far smaller plantation-and-industrials company. For investors, the question is whether the consolidated earnings power or the look-through value of the Britannia stake is the right valuation lens.

Sum-of-the-Parts (SOTP) Valuation Framework

Business Segments & Key Operations

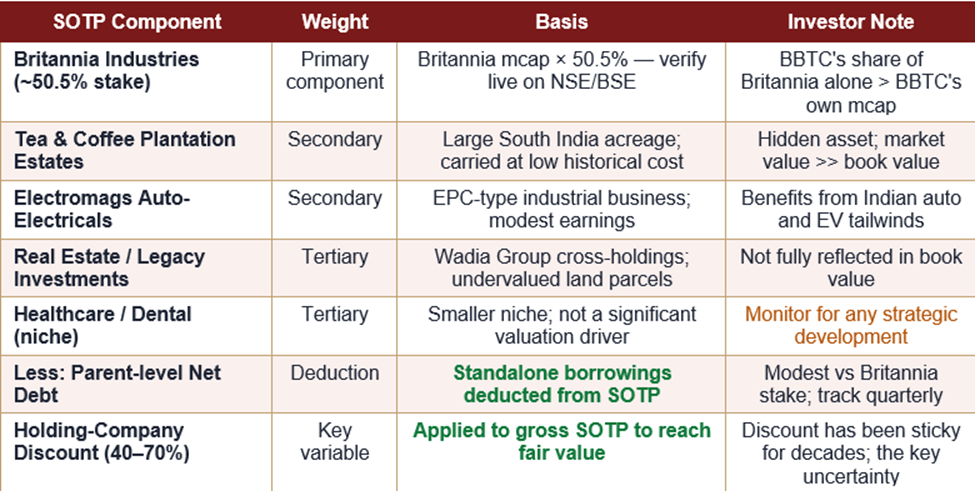

Segment 1 — Foods (Britannia Industries, ~50.5% stake)

Britannia is BBTC's crown jewel. With brands like Good Day, Tiger, Marie Gold, Bourbon, NutriChoice, Treat, Milk Bikis and Britannia Cheese, Britannia commands a leading share of India's organised biscuit market and is rapidly extending into dairy, cakes, rusks, croissants and adjacent categories.

Britannia's own multi-year capacity-expansion programme — greenfield plants across Tamil Nadu, Uttar Pradesh, Odisha and Bihar, plus deep distribution in rural India — flows directly into BBTC's consolidated revenue line. Any margin expansion or volume growth at Britannia moves BBTC's earnings materially.

Segment 2 — Plantations (Tea, Coffee and Horticulture)

BBTC's standalone heritage business operates large tea and coffee estates in South India — primarily the Anamallais and Valparai regions of Tamil Nadu. The company produces bulk tea, specialty coffee, cardamom and allied horticulture crops. Plantations are cyclical and weather-sensitive, but they remain a strategic long-duration land asset and generate modest operating profits.

Segment 3 — Auto-Electricals (Electromags)

Through its Electromags Automotive Products division, BBTC manufactures auto-electrical components — solenoids, switches, starter motor parts, and EV-relevant components — supplying Indian OEMs. This segment benefits from the broader tailwind in Indian auto and the ongoing shift toward electric vehicles.

Segment 4 — Real Estate and Investments

The company owns legacy land parcels and investments, including strategic cross-holdings within the Wadia Group. These are not fully reflected in book value and represent a hidden-asset angle for long-term investors. No near-term monetisation has been announced, but any strategic decision here would be a material value catalyst.

Financial Performance

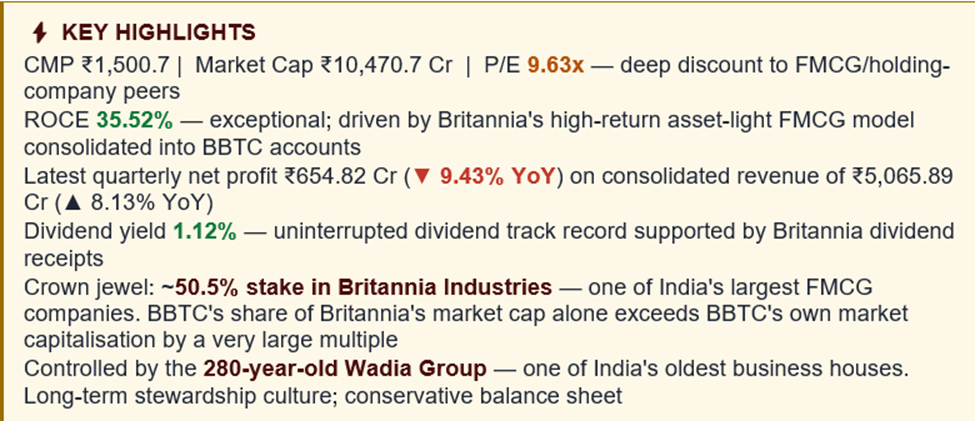

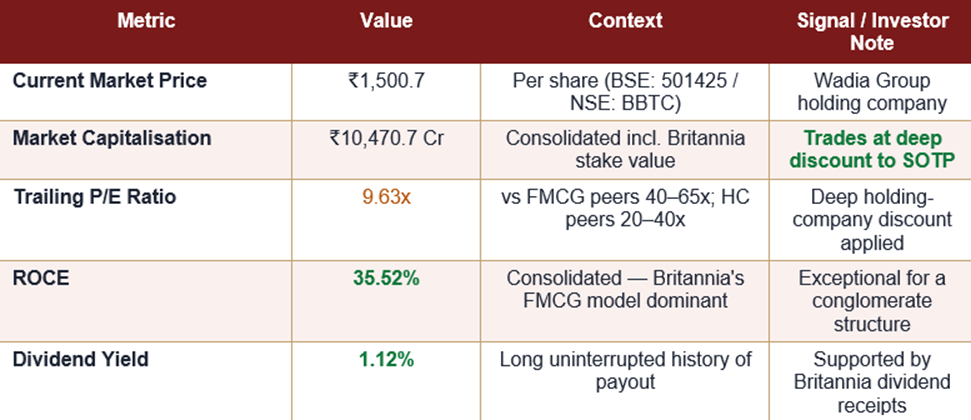

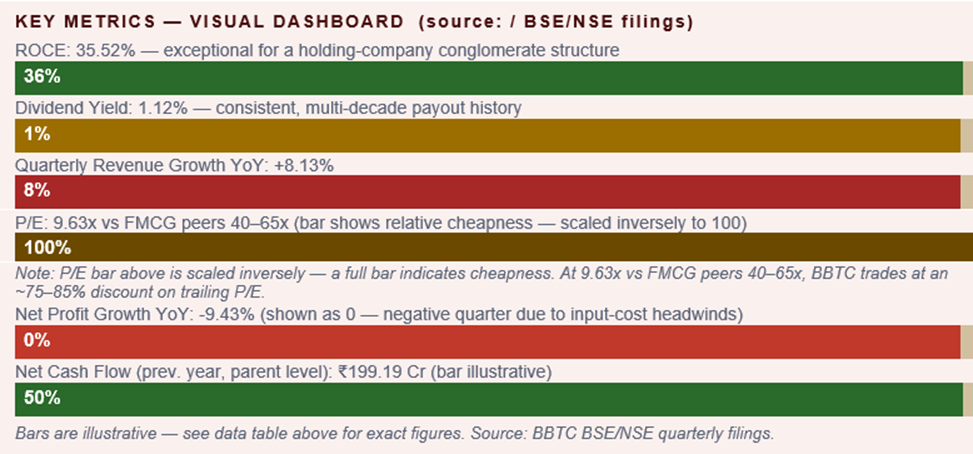

BBTC's consolidated financials reflect the dominance of Britannia in the group P&L. In the most recent reported quarter, the company posted consolidated revenue of ₹5,065.89 Cr, up 8.13% YoY — tracking Britannia's volume-led growth and modest price action. Net profit of ₹654.82 Cr was down 9.43% YoY, with the decline largely attributable to input-cost pressure (wheat, palm oil, sugar, packaging) at the Britannia level, along with some one-off items at the standalone plantation business.

Net cash flow of ₹199.19 Cr (previous year, at parent level) reflects healthy cash generation from dividends received from subsidiaries and operating cash from the plantations and auto-electricals businesses. ROCE of 35.52% is exceptional for a conglomerate structure, driven by the high return profile of Britannia's asset-light FMCG model.

Balance sheet: BBTC carries some debt at the standalone level — a point investors should watch — but the consolidated entity is comfortably serviced by Britannia's cash flows. The company's investment book, primarily the Britannia stake, is carried at historical cost on the balance sheet but has a market value that is a very large multiple of the entire BBTC market capitalisation, which is the core of the holding-company-discount thesis.

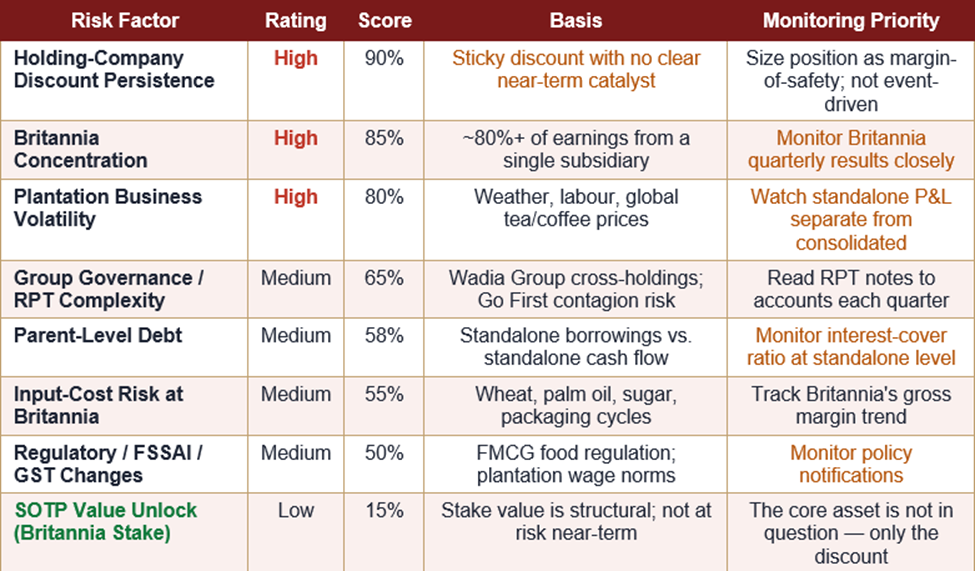

Risk Scorecard — BBTC

Risk ratings are qualitative assessments based on data, BSE/NSE filings, and sector analysis.

Price Performance & Dividend Record

BBTC has been a steady compounder over very long investment horizons, consistent with the Wadia Group's long-term stewardship culture. However, the stock's short-to-medium-term performance has been linked to Britannia's earnings trajectory, broader holding-company sentiment, and any group-level news flow.

The dividend yield of 1.12% represents an uninterrupted track record of distributions over many decades, funded by Britannia's own robust dividend payment to BBTC as the majority shareholder. For income-oriented investors, the dividend provides a modest but reliable cash return while the SOTP thesis plays out.

Valuation — Two Lenses

Lens A — Earnings Multiple (Consolidated Basis)

At a CMP of ₹1,500.7 and trailing P/E of 9.63x, BBTC trades at a very significant discount to the Indian FMCG peer group, which typically commands P/E multiples of 40–65x on data. Even applying a standard holding-company discount of 40–50% to the peer multiple implies a fair P/E for BBTC closer to 20–25x, suggesting the stock is optically cheap on an earnings basis. The ROCE of 35.52% corroborates the quality of the underlying earnings stream.

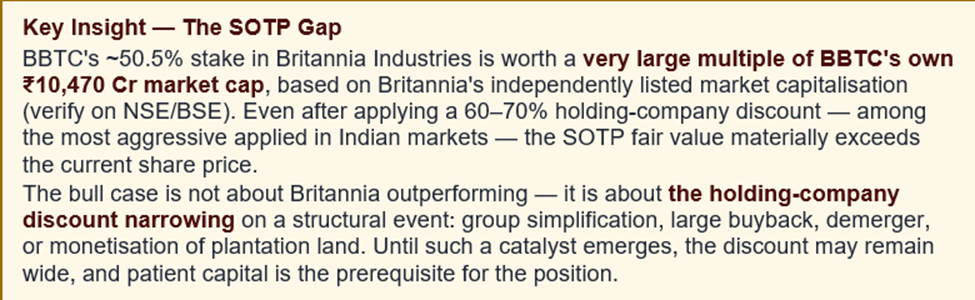

Lens B — Sum-of-the-Parts / Look-Through on Britannia Stake

BBTC owns approximately 50.5% of Britannia Industries. Britannia's own market capitalisation (readily available on NSE/BSE) runs into lakhs of crores; BBTC's share of that market value alone is several multiples of BBTC's ₹10,470.7 Cr market cap. Layered on top are plantation land assets, auto-electricals earnings, and real-estate holdings — each adding further value. Even after applying an aggressive holding-company discount of 60–70%, the SOTP fair value typically sits well above the current market cap.

Key Risks

1 — Holding-Company Discount Persistence

BBTC's market value has historically traded at a steep discount to the look-through value of its Britannia stake. This discount can remain wide for long periods, and the catalyst to close it is uncertain. Investors relying on a re-rating should size the position accordingly.

2 — Concentration in Britannia

Since Britannia drives the bulk of consolidated earnings, any slowdown in FMCG demand, market-share loss to competitors like Parle, ITC Foods, or Mondelez, or sharp input-cost spikes directly compresses BBTC's earnings. The recent 9.43% YoY profit decline is a live example of this pass-through.

3 — Standalone Business Volatility

The plantation business is exposed to weather, labour availability, wage inflation, and global tea/coffee prices. In bad years, the standalone business can post losses that dent sentiment even if consolidated numbers are fine. This creates periodic earnings noise.

4 — Group-Level Governance and Related-Party Complexity

As a Wadia Group entity with multiple cross-holdings and inter-company transactions, BBTC carries the typical complexity risk of Indian promoter-driven holding companies. The prolonged troubles at Go First (another Wadia Group company that went into insolvency) heightened investor caution on group-level capital allocation, though Go First and BBTC are legally distinct.

5 — Parent-Level Debt and Regulatory Risk

Standalone borrowings are modest relative to the Britannia stake value but are meaningful relative to standalone cash flows. Rising interest rates raise financing costs. Separately, changes in FSSAI regulation, GST rates on foods, or import duties on tea/coffee can affect specific segments.

Frequently Asked Questions

Q1. What does BBTC do?

BBTC is a 163-year-old Wadia Group holding company that operates tea and coffee plantations, auto-electrical components (Electromags), healthcare products and real estate, and holds a ~50.5% controlling stake in Britannia Industries Ltd. Most of its consolidated revenues and profits come from Britannia.

Q2. Is Bombay Burmah the same as Britannia Industries?

No. They are two separately listed companies. BBTC is the holding company that owns a majority stake in Britannia. Britannia is the operating FMCG business. Because BBTC consolidates Britannia, its financial statements look similar, but the two stocks trade independently on NSE/BSE.

Q3. Why is BBTC's P/E so low at 9.63x?

The low P/E reflects the holding-company discount that Indian markets typically apply, plus some concerns about group-level governance and concentration in a single underlying asset. On a pure earnings basis — and especially on a sum-of-the-parts basis — BBTC looks cheap relative to FMCG peers.

Q4. Does BBTC pay dividends?

Yes. BBTC has a long, uninterrupted track record of paying dividends, supported by the annual dividend it receives from Britannia. The current dividend yield is approximately 1.12%.

Q5. What are the biggest risks?

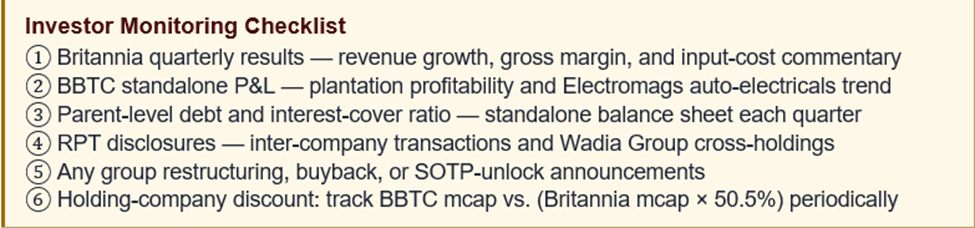

The main risks are: (a) persistence of the holding-company discount, (b) over-reliance on Britannia, (c) volatility in plantation earnings, (d) group-level governance and related-party complexity, and (e) parent-level debt. See the Key Risks section and Risk Scorecard above.

Q6. What is the ROCE and why is it high?

ROCE is 35.52%, driven predominantly by the high-return, asset-light FMCG business of Britannia flowing into BBTC's consolidated accounts. Standalone BBTC's ROCE would be materially lower.

Q7. What could re-rate the stock higher?

Potential catalysts include: (a) simplification of the Wadia Group holding structure, (b) a large share buyback by BBTC, (c) a strategic demerger or value-unlock transaction, (d) sustained outperformance by Britannia, and (e) monetisation of plantation or real-estate assets. Any of these would reduce the holding-company discount materially.

Q8. Where can I verify BBTC's latest financials?

The most reliable sources are BBTC's BSE filings (stock code 501425), NSE filings, and the company's annual reports and quarterly results announcements. Always cross-check against the latest filing before making an investment decision.