Highlights

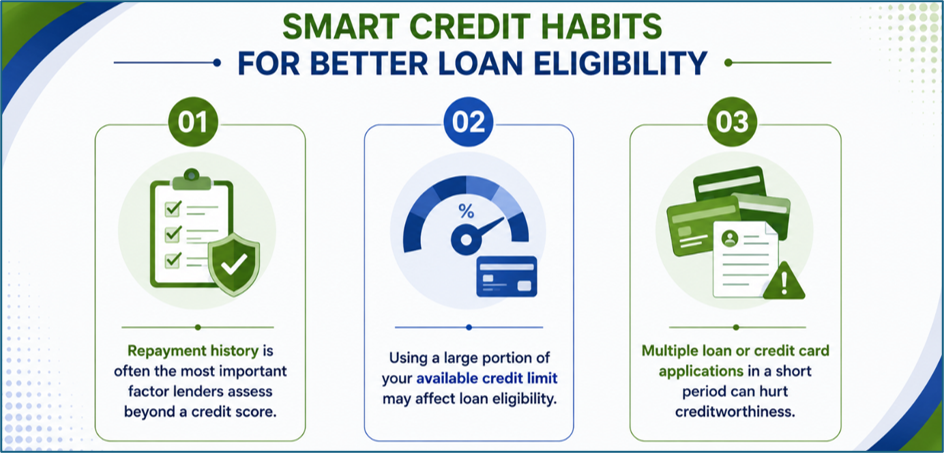

- Repayment behaviour remains one of the most important credit assessment factors.

- Credit utilisation and borrowing patterns can influence loan eligibility.

- Multiple loan applications within a short period may affect creditworthiness.

When applying for a loan, many borrowers focus primarily on their credit score. While the score is an important indicator of creditworthiness, lenders often assess a broader set of factors derived from an individual's credit report before making lending decisions.

A credit report contains detailed information about a borrower's financial behaviour, including repayment history, existing liabilities, credit usage patterns, and recent borrowing activity.

These elements collectively help lenders evaluate the likelihood of timely repayment. Credit scores are generated using data contained within these reports and are periodically updated as new information is reported by financial institutions.

Source: Analysis by Kalkine

Source: Analysis by Kalkine

Why Credit Reports Matter

A credit report acts as a financial track record. It captures information related to loans, credit cards, repayment performance, outstanding balances, and lender enquiries.

When a borrower applies for credit, lenders review this information to determine risk levels. A healthy credit profile may improve the chances of approval, while negative credit behaviour can raise concerns regarding repayment capacity.

The Biggest Factor: Repayment History

Among the various components of a credit report, repayment history generally carries the highest weight in credit assessment models. Timely payment of EMIs and credit card dues indicates responsible borrowing behaviour.

Conversely, missed payments, loan defaults, settlements, or prolonged delays can adversely affect creditworthiness and remain visible in credit records for extended periods. Even a single missed payment can have a noticeable impact on a credit profile, particularly when the borrower has a relatively limited credit history.

Credit Utilisation Can Influence Risk Assessment

Credit utilisation refers to the proportion of available credit being used by a borrower. For example, if an individual has a credit card limit of INR 2 lakh and consistently uses INR 1.5 lakh, lenders may view the high utilisation level as a sign of increased dependence on borrowed funds.

Financial experts often suggest maintaining utilisation levels well below the sanctioned credit limit, with many lenders viewing lower utilisation more favourably.

Length and Diversity of Credit History

A longer credit history provides lenders with more information about a borrower's financial discipline over time. In addition, maintaining a mix of secured and unsecured credit products can contribute to a more balanced credit profile.

Housing loans, vehicle loans, personal loans, and credit cards all contribute differently to a person's credit record. A well-managed credit portfolio can provide lenders with greater confidence regarding repayment behaviour.

Why Multiple Loan Applications Can Hurt

Every time a borrower applies for a loan or credit card, the lender may conduct a hard enquiry on the credit report. A limited number of enquiries is generally not a concern.

However, repeated applications within a short period may signal financial stress or urgent borrowing needs, potentially affecting lending decisions. Borrowers are therefore often advised to apply selectively rather than submitting multiple applications simultaneously.

Improving Creditworthiness Before Applying

Borrowers planning to seek credit may consider several steps before submitting an application:

- Pay all EMIs and card dues on time.

- Keep credit utilisation under control.

- Avoid unnecessary loan applications.

- Review credit reports for inaccuracies.

- Maintain existing credit accounts responsibly.

These measures may help strengthen a credit profile over time.

Key Risks

- Missed EMI payments can negatively affect credit records.

- High credit utilisation may increase perceived borrowing risk.

- Frequent loan enquiries can impact credit assessments.

- Errors in credit reports may affect loan approvals.

Summary

Loan approvals depend on more than a three-digit credit score. Information contained in a credit report, including repayment history, credit utilisation, account age, credit mix, and recent loan enquiries, contributes to the overall assessment of creditworthiness. Borrowers who manage credit responsibly and maintain healthy financial habits may improve their chances of obtaining favourable lending terms.

FAQs

Q: Is a high credit score enough to guarantee loan approval?

A: No, lenders also assess income, repayment history, liabilities, and overall credit behaviour before approving loans.

Q: Why does credit utilisation matter when applying for loans?

A: High utilisation may indicate greater dependence on credit and can influence lender risk assessments.

Q: Do multiple loan applications affect creditworthiness?

A: Yes, numerous hard enquiries within a short period may negatively influence credit evaluations.