Highlights

- Delaying retirement planning can significantly reduce the benefits of long-term compounding.

- Underestimating healthcare and living expenses may strain retirement savings over time.

- Relying on a single income source can increase financial vulnerability after retirement.

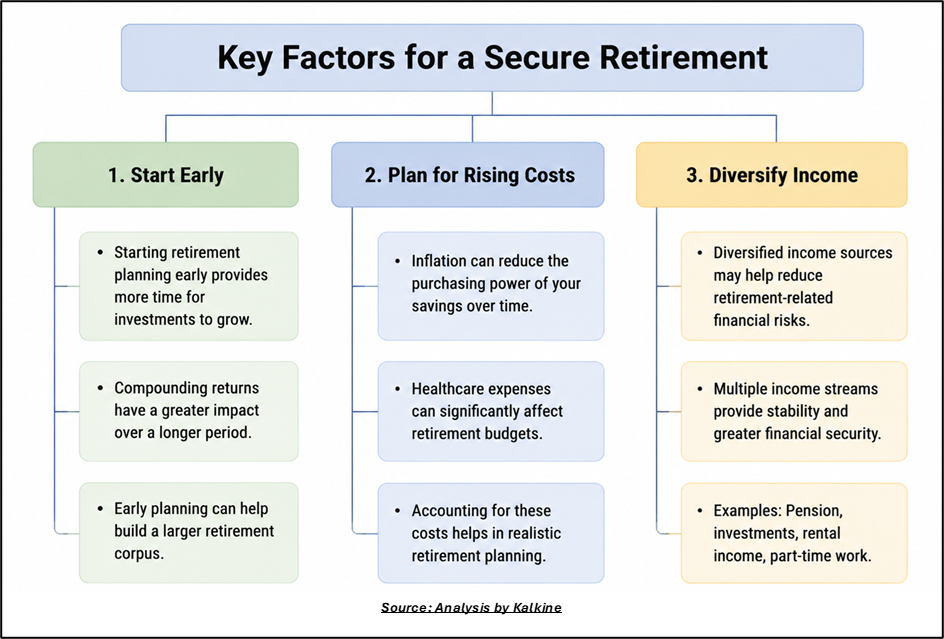

Many people postpone retirement planning because other financial goals appear more urgent. However, time is one of the most valuable resources in wealth creation. Investors who start early can spread contributions over a longer period and benefit from years of investment growth. Those who delay often need larger monthly investments later to reach similar retirement goals.

Retirement Expenses May Not Fall as Expected

A common misconception is that spending drops significantly after retirement. While commuting and work-related expenses may decline, other costs can rise. Medical treatment, insurance, household expenses, and lifestyle activities can create ongoing financial commitments. Planning retirement based on lower future expenses may lead to funding gaps later.

Why Multiple Income Streams Matter

Depending on a single source of retirement income can expose retirees to financial uncertainty. Rental income, pension payments, fixed-income investments, or business earnings may all face unexpected disruptions. Building multiple income sources can provide greater flexibility and reduce dependence on any one asset or investment.

Balancing Safety and Growth

Protecting savings becomes important as retirement approaches, but excessive caution can also create challenges. Investments that generate returns below inflation may gradually lose purchasing power. A retirement portfolio often needs a balance between capital preservation and long-term growth to support spending requirements over several decades.

Planning for a Longer Lifespan

Advances in healthcare and living standards mean people are generally living longer. While increased longevity is positive, it also means retirement savings may need to last for a longer period. Retirement plans that fail to account for a longer lifespan may face financial pressure in later years.

Keep Revisiting the Plan

Retirement planning should evolve alongside changes in income, expenses, family responsibilities, and market conditions. Regular reviews can help individuals assess progress, update assumptions, and make adjustments when necessary. Ongoing monitoring can help keep retirement goals on track despite changing circumstances.

Key Risks

- Delayed investing reduces the long-term benefits of compounding.

- Rising healthcare costs can exceed retirement projections.

- Inflation may steadily reduce purchasing power.

- Overdependence on one income source increases financial risk.

Summary

Retirement planning requires more than simply accumulating savings. Delayed investing, inaccurate expense estimates, overreliance on a single income source, overly conservative investments, and inadequate longevity planning can affect long-term financial stability. Reviewing plans regularly and maintaining a diversified approach can help individuals prepare for changing financial needs throughout retirement.

FAQs

Q: Why is early retirement planning important?

A: Early planning allows investments more time to benefit from compounding and can reduce future savings pressure.

Q: Should retirees completely avoid equity investments?

A: Not necessarily. A balanced allocation may help combat inflation and support long-term portfolio growth.

Q: How often should retirement plans be reviewed?

A: Reviewing plans annually or after major life events can help maintain alignment with financial goals.