Highlights

- Certain Sovereign Gold Bond redemptions are not treated as taxable transfers.

- Early redemption through RBI may not create a capital gains reporting obligation.

- Tax treatment differs significantly between redemption and market sale transactions.

Investors preparing to file Income Tax Returns for Assessment Year 2026-27 are reviewing the tax implications of various investment transactions completed during the previous financial year. Among the areas generating questions is the treatment of Sovereign Gold Bond (SGB) redemptions, particularly for investors who opted for the early redemption facility available after the completion of the prescribed holding period.

Many taxpayers assume that any profit earned from gold-linked investments automatically requires disclosure under capital gains schedules. However, the tax treatment of Sovereign Gold Bonds follows a distinct framework that differs from several other investment products.

Source: Analysis by Kalkine

Understanding the Special Nature of SGB Redemptions

Sovereign Gold Bonds are government-backed securities linked to gold prices and issued through the Reserve Bank of India on behalf of the Government of India.

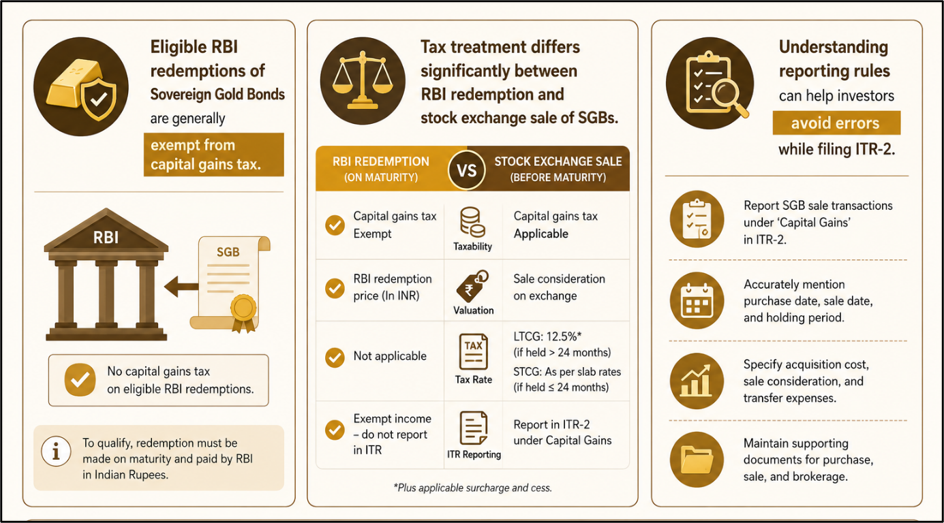

Unlike traditional investments where gains arise upon transfer or sale, redemption of eligible SGBs through the RBI is subject to specific provisions under income tax law. In certain circumstances, such redemption is not regarded as a transfer for capital gains purposes. As a result, investors may not face a capital gains tax liability despite earning appreciation on the investment.

Why Early Redemption Receives Different Treatment

SGB investors are generally allowed to seek redemption before final maturity after completing the minimum qualifying holding period specified under the scheme.

Where an individual investor redeems eligible bonds directly through the RBI redemption mechanism, the transaction is generally not considered a taxable transfer under the applicable provisions of the Income Tax Act. Since capital gains normally arise from the transfer of a capital asset, the absence of a transfer means there may be no capital gains to compute or disclose.

This treatment applies differently from situations where bonds are sold in the secondary market.

Redemption and Sale Are Not the Same

One of the most important distinctions for investors is the difference between redemption and sale.

When eligible bonds are redeemed through the RBI mechanism, the transaction may qualify for tax-exempt treatment. However, when an investor sells SGBs on a stock exchange or transfers them to another party, the transaction can trigger capital gains taxation based on the applicable holding period and tax rules.

Therefore, investors should carefully identify the nature of the transaction before determining reporting obligations in their income tax return.

Do Investors Need to Report Such Gains in ITR-2?

Since eligible redemption proceeds are generally not regarded as taxable capital gains, investors may not be required to report them under the capital gains schedule of ITR-2.

Tax experts note that because the redemption itself is not treated as a transfer, the resulting proceeds are not considered taxable capital gains income. Consequently, many investors will not find a specific capital gains disclosure requirement for such transactions.

Some taxpayers may nevertheless choose to disclose the amount under the exempt income section as an additional precaution, although such reporting is generally considered optional rather than mandatory.

Importance of Reviewing Updated Tax Rules

Investors should also remain aware that taxation rules relating to Sovereign Gold Bonds have undergone changes in recent years.

The applicable treatment may vary depending on factors such as acquisition method, redemption date, and whether the investor originally subscribed to the bond issue or acquired the bonds through secondary market transactions. As a result, reviewing the rules relevant to the specific investment period remains important before filing returns.

Record Keeping Remains Essential

Even where tax is not payable, maintaining proper records remains advisable.

Investors should preserve allotment documents, redemption statements, bank credit records, and interest payment details. These records can assist in explaining the nature of the transaction if clarification is sought at a later stage.

Proper documentation also helps distinguish between tax-exempt redemption transactions and taxable sale transactions.

Key Risks

- Confusing redemption with market sale may result in incorrect reporting.

- Secondary market transactions may attract capital gains taxation.

- Tax rules may vary based on acquisition method.

- Inadequate documentation can complicate future verification.

Summary

Sovereign Gold Bond investors who redeemed eligible bonds through the RBI's redemption mechanism may not be required to report capital gains in ITR-2 because such redemptions are generally not treated as taxable transfers. However, this treatment differs from stock exchange sales, which can trigger capital gains tax. Investors should review transaction details carefully and maintain proper documentation while preparing their tax returns.

FAQs

Q: Does early RBI redemption of Sovereign Gold Bonds always create capital gains tax?

A: Eligible RBI redemptions by individuals are generally not treated as taxable capital gains transfers.

Q: Is selling SGBs on a stock exchange treated differently?

A: Yes, exchange sales can trigger capital gains taxation depending on holding period rules.

Q: Must exempt SGB redemption proceeds be reported in ITR-2?

A: Generally no, though some taxpayers voluntarily disclose them under exempt income schedules.