Highlights

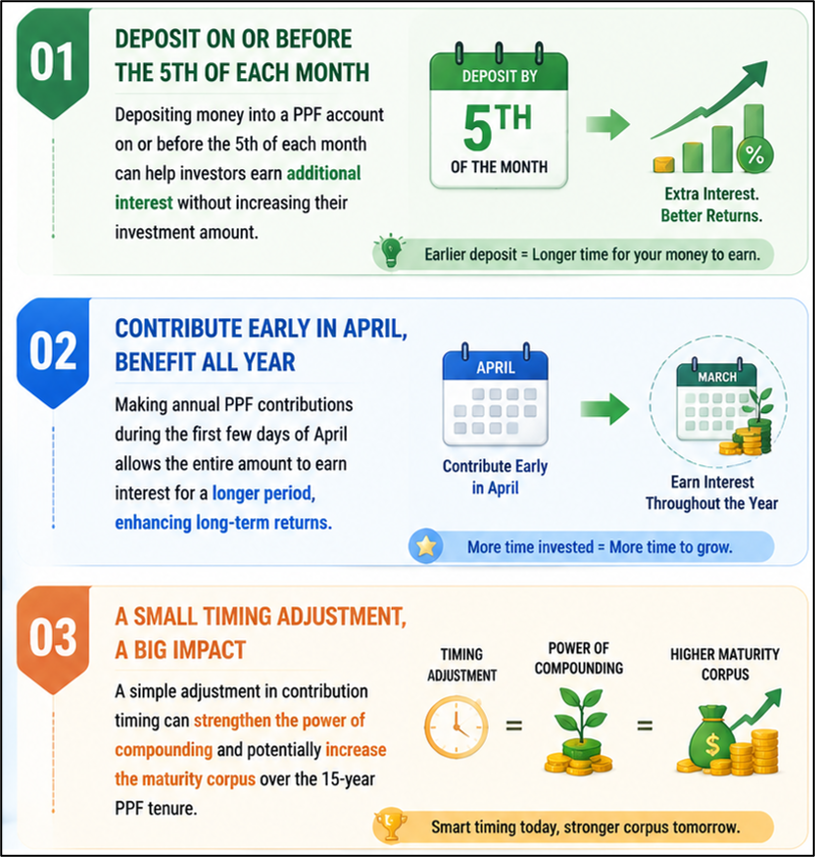

- Depositing money before the 5th of the month helps maximise PPF interest.

- A small timing adjustment can improve long-term compounding benefits.

- Annual contributions made early in the financial year earn interest longer.

The Public Provident Fund (PPF) remains one of India's most widely used long-term savings schemes, offering government-backed security, tax benefits and fixed-income returns. While most investors focus on the amount they contribute, the timing of those contributions can also influence overall returns. A simple deposit-timing strategy can help investors earn additional interest each year without increasing the amount invested. This lesser-known rule stems from the way PPF interest is calculated.

Source: Analysis by Kalkine

Understanding How PPF Interest Is Calculated

PPF interest is calculated every month but credited to the account at the end of the financial year. The calculation is based on the lowest balance available in the account between the 5th day and the last day of each month. As a result, the date on which money is deposited can affect whether that contribution earns interest for the current month or only from the following month.

For example, if a contribution is credited to a PPF account on or before the 5th of a month, it becomes part of the balance considered for interest calculations during that month. However, if the deposit is made after the 5th, the amount generally begins earning interest only from the next month.

Why the First Five Days Matter

The difference may appear minor in a single month, but over several years it can add up through compounding. By ensuring that monthly contributions reach the account before the 5th, investors can capture an additional month's interest on each contribution. This approach does not require any increase in investment amount and relies solely on better timing.

Financial planners often suggest scheduling automatic transfers during the first few days of every month to avoid missing the interest calculation window. Depositing on the 1st of the month is generally considered the safest approach because it reduces the risk of processing delays.

Annual Investors Have an Additional Advantage

Investors who prefer making a lump-sum contribution instead of monthly deposits can also benefit from this timing rule. Those planning to invest the maximum annual contribution may earn more interest by depositing the amount during the first few days of April, the beginning of the financial year. This allows the entire contribution to remain in the account for a longer period and potentially earn interest for all twelve months of the year.

Because PPF has a long tenure of 15 years, even small improvements in annual interest accumulation can have a noticeable effect on the maturity corpus. The impact becomes more visible when compounded over multiple years.

Compounding Makes Small Gains More Meaningful

The benefit of depositing before the 5th may not seem substantial in the first year. However, PPF returns are compounded over time, meaning additional interest earned today can itself generate future interest. This compounding effect is what transforms a seemingly small timing advantage into a potentially meaningful gain over the life of the account.

Several investor discussions also highlight that while the difference from a single month's interest may appear limited, following the rule consistently over many years can improve overall returns without requiring additional savings.

Automating Contributions Can Help

For investors making regular monthly contributions, setting up automated transfers before the 5th can ensure consistency. This removes the possibility of forgetting a contribution or missing the interest calculation period. Since PPF is designed as a long-term savings vehicle, disciplined and timely investing can be as important as the amount invested.

Timing Is a Simple Way to Improve Returns

While market-linked investments often require investors to manage risk and volatility, PPF offers an opportunity to improve returns through a simple administrative step. Depositing contributions before the 5th of each month helps ensure that money begins earning interest sooner. Over a long investment horizon, this small adjustment can contribute to higher overall earnings and a larger maturity corpus.

Key Risks

- Deposits after the 5th may miss interest for that month.

- Delayed transfers can reduce annual interest earnings.

- Inconsistent contributions may limit compounding benefits.

- Waiting until year-end reduces interest accumulation potential.

Summary

PPF investors can improve returns through a simple timing strategy. Since interest is calculated on the lowest balance between the 5th and the end of each month, contributions credited on or before the 5th begin earning interest sooner. Whether investing monthly or annually, making deposits early can enhance long-term compounding and increase the maturity value without requiring additional investment.

FAQs

Q: Why is the 5th of the month important for PPF investors?

A: PPF interest is calculated on the balance maintained between the 5th and month-end.

Q: Does depositing after the 5th affect returns?

A: Yes, contributions made after the 5th generally start earning interest from the following month.

Q: When should annual PPF contributions ideally be made?

A: Many investors prefer depositing during the first five days of April for maximum annual interest.