Highlights

- Options trading losses may help reduce tax on eligible non-salary income.

- Unused losses can be carried forward for up to eight assessment years.

- Proper ITR filing is essential to preserve future tax adjustment benefits.

Investors often focus on profits earned from derivatives trading, but losses can also have tax implications. Individuals who incurred substantial losses in options trading during FY26 may be able to use those losses to reduce their taxable income, subject to provisions under the Income Tax Act.

Many traders are unaware that options transactions receive different tax treatment from traditional share investments. Understanding how these losses are classified and adjusted can help taxpayers avoid paying more tax than necessary while filing their returns.

Source: Analysis by Kalkine

Why Options Trading Is Treated Differently

Profits and losses from delivery-based share investments are generally taxed under the capital gains framework. However, derivatives such as futures and options (F&O) are classified differently under tax rules.

Recognised exchange-traded derivatives are treated as non-speculative business transactions. As a result, profits and losses arising from options trading are reported under the head "Profits and Gains from Business or Profession" rather than capital gains.

This distinction becomes important because business losses enjoy broader set-off provisions than many other categories of losses.

How a Loss Can Reduce Taxable Income

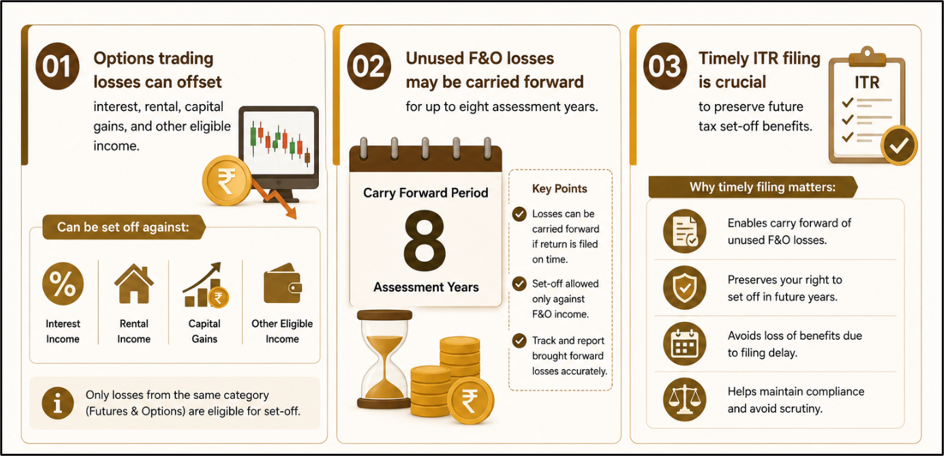

A non-speculative business loss arising from options trading can generally be adjusted against several other categories of income during the same financial year.

For example, such losses may be set off against:

- Interest earned on fixed deposits.

- Savings account interest.

- Rental income.

- Capital gains.

- Other eligible business income.

However, one major restriction applies. Business losses cannot be adjusted against salary income. Therefore, salaried taxpayers cannot use options trading losses to reduce tax payable on their salary earnings.

Example of Tax Adjustment

Suppose a trader records an options trading loss of INR 15 lakh during FY26 and simultaneously earns interest income from fixed deposits and other investments.

In such a case, the loss may be used to offset the interest income while calculating taxable income. This can reduce the overall tax liability for the year, depending on the amount of income available for adjustment.

The actual benefit will depend on the taxpayer's income composition and applicable tax provisions.

What Happens If the Entire Loss Cannot Be Used?

In many situations, the available income may not be sufficient to absorb the entire options trading loss during the same year.

Tax rules permit the unadjusted portion of a non-speculative business loss to be carried forward for future use. Such losses can generally be carried forward for up to eight assessment years and adjusted against eligible business income earned during those years.

This provision allows taxpayers to potentially benefit from the loss even if immediate set-off opportunities are limited.

Importance of Timely Return Filing

The carry-forward benefit is not automatic.

Taxpayers must file their income tax return within the prescribed due date to preserve the right to carry forward business losses. Missing the filing deadline may result in the loss of this tax benefit, preventing future adjustments against eligible income.

Accurate reporting of options trading activity is therefore important even when the overall result is a loss.

Compliance Requirements for Traders

Since F&O transactions are treated as business income, traders may need to maintain supporting records relating to their trading activity.

Depending on turnover levels and other conditions, additional compliance requirements such as bookkeeping and tax audit provisions may also become relevant. Investors should review their obligations carefully before filing returns.

Key Risks

- Business losses cannot be adjusted against salary income.

- Late ITR filing may eliminate carry-forward benefits.

- Incorrect classification can trigger tax reporting errors.

- Audit and compliance requirements may apply in some cases.

Summary

Losses from options trading are generally treated as non-speculative business losses under Indian tax rules. These losses can often be adjusted against interest income, rental income, capital gains, and certain other taxable income streams, though not against salary income. Any unutilised loss may be carried forward for up to eight years, provided the taxpayer files the income tax return within the prescribed deadline and complies with reporting requirements.

FAQs

Q: Can an options trading loss reduce tax on fixed deposit interest?

A: Yes, eligible options trading losses can generally be adjusted against taxable interest income.

Q: Can options trading losses be set off against salary income?

A: No, business losses cannot be adjusted against income taxable under the salary head.

Q: How long can unused options trading losses be carried forward?

A: Eligible non-speculative business losses can generally be carried forward for eight years.