Highlights

- Sweep-in FDs combine savings account liquidity with fixed deposit interest earnings.

- Emergency funds require quick access, making liquidity a key consideration.

- A balanced approach may help improve returns without sacrificing accessibility.

An emergency fund serves as a financial cushion during unexpected situations such as medical emergencies, job loss, urgent home repairs, or other unforeseen expenses. While many individuals keep this money in a traditional savings account for easy access, the relatively low interest earned on idle balances often raises an important question: should emergency fund money be moved into a sweep-in fixed deposit (FD)?

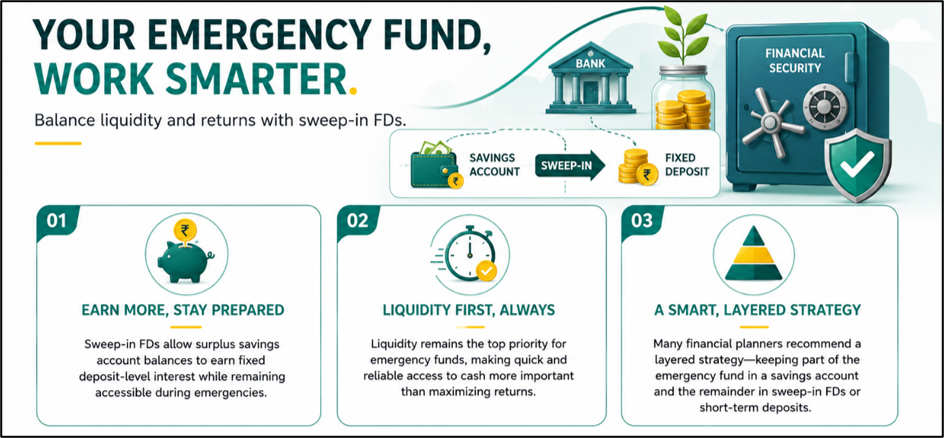

The answer depends on balancing two essential goals—maintaining immediate access to funds and earning a better return on money that may remain unused for long periods.

Source: Analysis by Kalkine

Source: Analysis by Kalkine

Understanding How a Sweep-In FD Works

A sweep-in FD is a banking facility that automatically transfers surplus money from a savings account into a linked fixed deposit once the account balance exceeds a pre-defined threshold.

When funds are required, the bank automatically breaks the necessary portion of the FD and transfers it back into the savings account. This arrangement allows customers to earn FD-level interest on excess balances while retaining access to funds when needed.

Why Emergency Funds Need Liquidity First

The primary purpose of an emergency fund is not wealth creation. Its role is to provide immediate financial support during unforeseen events.

For this reason, accessibility remains more important than maximizing returns. Money needed during an emergency should be available without delays, complicated procedures, or significant penalties. Financial planners generally emphasize liquidity and capital protection as the key characteristics of an emergency fund.

Potential Benefits of Using a Sweep-In FD

One of the biggest advantages of a sweep-in FD is the ability to earn higher interest compared to a standard savings account.

Since only the amount above a specified threshold is transferred into the deposit, account holders continue to maintain a minimum readily available balance while surplus funds generate improved returns. This can help reduce the opportunity cost of keeping large sums idle in a low-interest account.

Another advantage is convenience. The movement of funds happens automatically, eliminating the need to manually create and break fixed deposits.

Why Keeping Everything in a Sweep-In FD May Not Be Ideal

Although sweep-in facilities offer flexibility, moving the entire emergency corpus into a sweep-in structure may not suit every situation.

Unexpected expenses often require immediate access to cash. Maintaining a portion of emergency savings directly in a regular savings account can provide additional comfort and ensure funds remain instantly available under all circumstances. Experts often recommend avoiding excessive dependence on a single emergency fund vehicle.

In addition, different banks may have varying rules regarding minimum thresholds, withdrawal mechanisms, and interest calculations. Understanding these terms is important before enabling the facility.

A Layered Approach May Offer Greater Flexibility

Rather than choosing between a savings account and a sweep-in FD, many financial experts advocate dividing emergency savings into multiple layers.

A common approach involves keeping one portion in a savings account for immediate use while placing the remaining balance in sweep-in deposits or short-term fixed deposits. This structure aims to preserve liquidity while allowing part of the emergency fund to earn higher returns.

Community discussions among investors also indicate growing preference for a layered strategy that combines accessibility, safety, and reasonable returns.

When a Sweep-In FD Makes Sense

A sweep-in FD may be suitable for individuals who:

- Maintain a sizeable emergency fund in a savings account.

- Want better returns without actively managing deposits.

- Require continued access to funds for emergencies.

- Prefer banking products over market-linked alternatives.

However, the suitability of the facility ultimately depends on personal cash-flow requirements, risk tolerance, and emergency fund size.

Key Risks to Consider

- Emergency access may depend on bank systems functioning smoothly.

- Different banks may impose varying sweep-in conditions.

- Premature withdrawal rules can affect interest earnings.

- Over-optimizing returns may reduce liquidity flexibility.

Summary

Sweep-in fixed deposits can help emergency fund holders earn higher returns than a traditional savings account while retaining access to funds when required. However, emergency savings should prioritize liquidity and safety over yield. Many financial planners favor a layered strategy that combines a savings account with sweep-in deposits or short-term FDs. The objective is not to maximize returns but to ensure money remains available when an unexpected expense arises.

FAQs

Q: What is a sweep-in FD?

A: It automatically transfers excess savings account balances into fixed deposits while keeping funds accessible when required.

Q: Is a sweep-in FD suitable for emergency funds?

A: It can be useful if liquidity remains available and sufficient funds stay accessible for immediate emergencies.

Q: Should an entire emergency fund be placed in a sweep-in FD?

A: Many experts recommend keeping some money in savings and the remainder in sweep-in deposits.