Highlights

- Lower interest rates can reduce overall borrowing costs significantly.

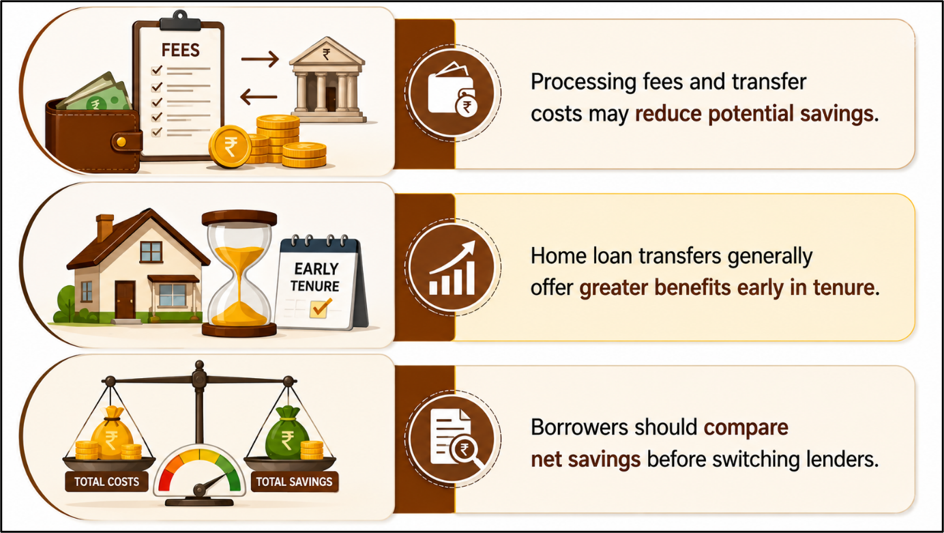

- Processing fees and transfer expenses may reduce potential savings.

- Timing and remaining loan tenure play a critical role in benefits.

A home loan is often one of the longest financial commitments undertaken by an individual. Since loan tenures can extend over two or three decades, changes in interest rates during the repayment period may prompt borrowers to explore alternatives.

One such option is a home loan balance transfer, where the outstanding loan amount is moved from an existing lender to another bank or housing finance company offering different loan terms. The objective is typically to secure a lower interest rate, reduce monthly repayments, or improve overall loan conditions.

Source: Analysis by Kalkine

Source: Analysis by Kalkine

Why Borrowers Consider Switching Lenders

The primary reason for transferring a home loan is the possibility of lowering interest costs.

Even a small reduction in interest rates can generate substantial savings when the outstanding loan amount is large and the repayment period is long. Borrowers may also use a balance transfer to lower their EMIs or shorten the loan tenure while maintaining the same EMI amount.

Apart from interest rates, some borrowers seek better customer service, more flexible repayment options, faster processing, or improved prepayment facilities from another lender.

The Importance of Calculating Actual Savings

A lower advertised interest rate should not be the sole factor driving a transfer decision.

Borrowers must compare the projected interest savings with the total cost of transferring the loan. Expenses may include processing charges, legal fees, valuation costs, documentation expenses, and administrative charges. In some cases, these costs can significantly reduce the expected financial benefit.

Before proceeding, it is advisable to calculate the net savings after considering all associated expenses.

Timing Can Make a Significant Difference

The stage of the loan plays a major role in determining whether a balance transfer is worthwhile.

Home loans are generally interest-heavy during the initial years. As a result, transferring a loan early in its tenure often provides greater savings because a larger portion of future payments would otherwise go toward interest.

On the other hand, borrowers nearing the end of their repayment period may see limited benefits because much of the interest has already been paid.

Evaluate the Interest Rate Difference Carefully

Financial experts often suggest that a meaningful difference between the existing and proposed interest rates is necessary for a transfer to make economic sense.

A minor reduction may not justify the paperwork, documentation requirements, and transfer expenses. Borrowers should therefore focus on overall savings rather than being influenced solely by promotional rates.

In some situations, negotiating with the current lender for a rate reduction may prove more practical than switching institutions entirely.

Credit Score Remains Important

A home loan transfer is treated similarly to a fresh loan application.

The new lender typically evaluates the borrower's credit score, repayment history, income profile, existing liabilities, and overall financial standing before approving the transfer. Borrowers with stronger credit profiles are generally better positioned to secure competitive loan terms.

Reviewing credit reports and addressing any discrepancies before applying can improve the likelihood of approval.

Check the Fine Print Before Signing

Borrowers should carefully examine all loan terms before finalizing a transfer.

Factors such as floating-rate reset mechanisms, prepayment conditions, loan servicing standards, and future interest-rate transmission policies can affect the long-term value of the transfer. A lower initial rate may not necessarily remain the most attractive option throughout the loan tenure.

Understanding these conditions can help prevent unexpected costs later.

Conclusion

A home loan balance transfer can help reduce borrowing costs and improve loan terms when executed under the right circumstances. However, the decision should be based on comprehensive calculations rather than headline interest rates alone.

Borrowers should assess transfer costs, remaining tenure, interest savings, credit eligibility, and lender policies before making a final decision. A careful evaluation can determine whether the switch genuinely delivers long-term financial benefits.

Key Risks

- Transfer costs may offset expected interest savings.

- Small rate differences may provide limited financial benefit.

- Loan transfer approval depends on credit assessment.

- Attractive introductory rates may change over time.

Summary

A home loan balance transfer allows borrowers to move an existing loan to another lender offering different terms. While lower interest rates can reduce overall repayment costs, borrowers must evaluate processing charges, legal expenses, remaining tenure, and credit eligibility. Transfers generally provide greater benefits during the early years of a loan. Careful calculations are essential to determine whether the switch creates meaningful long-term savings.

FAQs

Q: What is a home loan balance transfer?

A: It involves shifting an existing home loan to another lender offering different interest rates or repayment terms.

Q: When does a home loan transfer make the most sense?

A: It is generally more beneficial during the early years of repayment when interest costs remain relatively high.

Q: Should borrowers focus only on lower interest rates?

A: No, transfer fees, legal costs, loan terms, and overall savings should also be evaluated before switching lenders.