Highlights

- EPF withdrawals before five years of service may attract tax liability.

- Tax treatment depends on service duration, withdrawal amount, and documentation.

- Premature withdrawals can also reduce long-term retirement corpus growth.

The Employees' Provident Fund (EPF) serves as one of the primary retirement savings vehicles for salaried employees in India. While the accumulated corpus can provide financial support during emergencies or career transitions, withdrawing EPF funds without understanding the tax implications can lead to unexpected costs.

Before initiating an EPF withdrawal, members should evaluate not only their immediate financial needs but also the tax consequences and long-term impact on retirement savings. In many cases, the timing of the withdrawal plays a significant role in determining whether taxes apply.

Source: Analysis by Kalkine

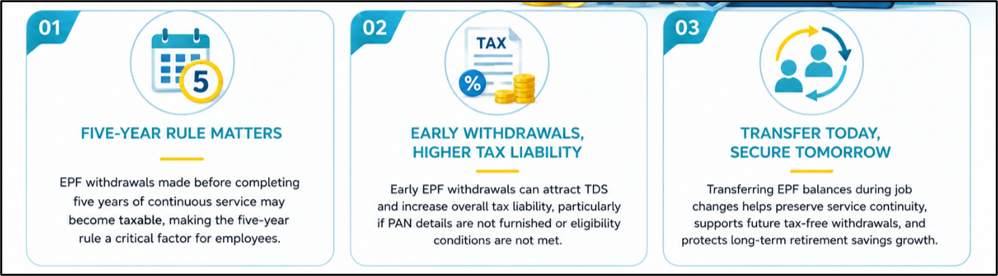

The Five-Year Rule Remains Critical

One of the most important factors governing EPF taxation is the duration of continuous service. In general, EPF withdrawals made after completing five years of continuous service are exempt from tax. Continuous service includes periods spent with multiple employers, provided the EPF balance has been transferred rather than withdrawn when changing jobs.

However, if a member withdraws EPF savings before completing five years of continuous service, the withdrawal may become taxable under applicable income tax provisions.

How Early Withdrawals Can Trigger Tax Liability

Premature withdrawals can result in multiple tax implications. Components such as the employer's contribution, interest earned, and certain tax benefits claimed earlier may become subject to taxation.

The withdrawn amount may be added to the individual's taxable income for the relevant financial year, increasing the overall tax burden depending on the applicable income tax slab.

For many employees, this comes as a surprise because the full impact often becomes evident only when filing the income tax return.

Understanding TDS on EPF Withdrawals

Tax Deducted at Source (TDS) can apply when EPF funds are withdrawn before completing five years of continuous service and the withdrawal exceeds prescribed thresholds.

Where Permanent Account Number (PAN) details are available, TDS may be deducted at the applicable rate. Higher deductions may apply if PAN information is not furnished. Eligible individuals may submit Form 15G or Form 15H, subject to conditions, to seek relief from TDS deductions.

It is important to remember that TDS is not necessarily the final tax liability. The final tax obligation is determined while filing the income tax return.

Job Changes Can Affect Tax Outcomes

Many employees switch jobs several times during their careers. In such cases, transferring EPF balances to the new employer's account can help preserve continuity of service.

If the EPF balance is withdrawn at every job change, the five-year service period effectively resets. This may increase the chances of future withdrawals becoming taxable. On the other hand, transferring the account helps maintain continuity and may support tax-free withdrawals later.

Retirement Planning Considerations

Apart from taxes, withdrawing EPF savings prematurely can affect long-term wealth creation.

EPF is designed as a retirement-oriented savings instrument that benefits from compounding over extended periods. Frequent withdrawals reduce the amount available for future growth and may weaken retirement preparedness.

Financial planners often advise evaluating alternative funding options before tapping into retirement savings unless the requirement is unavoidable.

When Withdrawal May Make Sense

There are circumstances where EPF withdrawals may be necessary, including prolonged unemployment, medical emergencies, housing-related requirements, education expenses, or retirement.

In such situations, understanding eligibility rules and tax treatment beforehand can help members make informed financial decisions and avoid surprises after receiving the funds.

Key Risks of Early EPF Withdrawal

- Tax liability may arise before five years of service.

- TDS deductions can reduce immediate payout amounts.

- Retirement corpus growth may be interrupted.

- Service continuity benefits could be lost.

Summary

EPF withdrawals can provide financial support during important life events, but tax consequences should not be overlooked. The five-year continuous service rule remains a key determinant of taxability. Early withdrawals may attract tax and TDS, while frequent withdrawals can disrupt retirement planning and service continuity. Understanding the applicable rules before submitting a claim can help employees make more informed decisions regarding their provident fund savings.

FAQs

Q: Is EPF withdrawal always tax-free?

A: No. Withdrawals before completing five years of continuous service may attract tax under applicable rules.

Q: Does changing jobs reset the five-year EPF period?

A: Not if the EPF account is transferred. Service continuity can continue across employers.

Q: Can TDS deducted on EPF withdrawal be claimed back?

A: Eligible taxpayers may claim credit or refunds while filing their income tax returns.