Highlights

- The lowest EMI does not always result in the lowest borrowing cost.

- Loan tenure can significantly increase total interest payments over time.

- Additional fees and charges may raise the overall cost of a home loan.

When evaluating a home loan, most borrowers focus on the interest rate and monthly EMI. While these are important factors, they do not always reveal the complete financial commitment involved.

A home loan can include several additional expenses and long-term costs that may substantially increase the amount repaid over the life of the loan. Understanding these components can help borrowers make more informed decisions before signing a loan agreement.

Source: Analysis by Kalkine

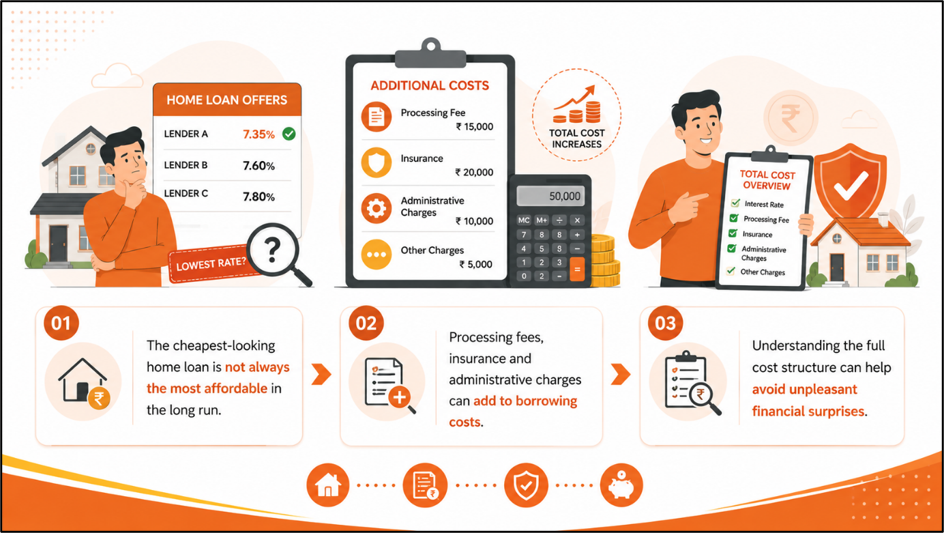

Why a Lower EMI Can Be Misleading

A lower EMI often appears attractive because it reduces the monthly repayment burden. However, lenders frequently achieve lower EMIs by extending the loan tenure. While this may improve short-term affordability, a longer repayment period means interest is charged for a greater number of years. As a result, borrowers may end up paying significantly more in total interest even though the monthly instalment appears manageable. Looking only at the EMI can therefore provide an incomplete picture of the actual borrowing cost.

The Impact of Loan Tenure on Total Repayment

The tenure of a home loan plays a major role in determining the total amount paid to the lender. Shorter tenures generally result in higher EMIs but lower overall interest costs. Conversely, longer tenures reduce monthly payments but increase the cumulative interest paid over the years. Even a difference of a few years can add a substantial amount to the final repayment figure. Borrowers should therefore assess both the EMI and the total repayment obligation before choosing a loan tenure.

Charges Beyond the Interest Rate

The advertised interest rate is only one part of a home loan's cost structure. Borrowers may also incur processing fees, legal verification charges, property valuation fees, documentation expenses and insurance-related costs. While these charges may appear small individually, they can collectively add a significant amount to the overall borrowing expense. Understanding all applicable charges before loan approval can help avoid unexpected costs later.

Hidden Expenses Borrowers Often Overlook

In addition to standard charges, some home loans may involve administrative fees, account maintenance charges, loan conversion fees and expenses associated with restructuring the loan. Property-related registration and documentation costs can also contribute to the overall financial burden. Because these expenses are not always highlighted in loan advertisements, borrowers may underestimate the true cost of home ownership financed through a loan.

Looking at the Total Cost Instead of Just the EMI

A home loan is typically a long-term financial commitment that can span decades. Rather than focusing solely on the monthly EMI, borrowers may benefit from evaluating the total interest payable, the overall repayment amount and all associated fees. Reviewing prepayment conditions, refinancing options and other loan features can also provide a more comprehensive understanding of long-term affordability.

Questions Borrowers Should Ask Before Signing

Before accepting a home loan offer, borrowers should seek clarity on the total repayment amount over the loan tenure, applicable processing and administrative charges, insurance requirements and any fees associated with future modifications to the loan. Understanding these aspects in advance can help prevent surprises and support better financial planning.

Planning for Long-Term Affordability

Obtaining a home loan approval is only the first step in a long financial journey. Borrowers who understand the complete cost structure of their loan are often better equipped to manage repayments and maintain financial stability. Evaluating all costs rather than focusing solely on the headline interest rate or EMI can lead to more informed borrowing decisions.

Key Risks to Watch

- Longer loan tenures can substantially increase total interest costs.

- Hidden charges may raise borrowing expenses unexpectedly.

- Focusing only on EMI can mask the actual loan cost.

- Overlooking loan terms may reduce financial flexibility later.

Summary

A home loan's true cost extends beyond its advertised interest rate and monthly EMI. Factors such as loan tenure, processing fees, legal charges, insurance costs and administrative expenses can significantly affect the total repayment amount. Borrowers who evaluate the complete cost of borrowing rather than focusing solely on monthly instalments may gain a clearer understanding of their long-term financial commitment and make better-informed decisions.

FAQs

Q: Does a lower EMI always mean a cheaper home loan?

A: No. Lower EMIs often result from longer tenures, which can increase total interest payments significantly.

Q: What additional costs should borrowers review before taking a home loan?

A: Processing fees, legal charges, valuation expenses, insurance costs and administrative fees should all be considered.

Q: Why is total repayment amount important when comparing home loans?

A: It reflects the complete borrowing cost, including principal, interest and applicable charges over the loan tenure.