Key Highlights

- New tax regime is now the default regime for salaried employees as per the Finance Act 2023

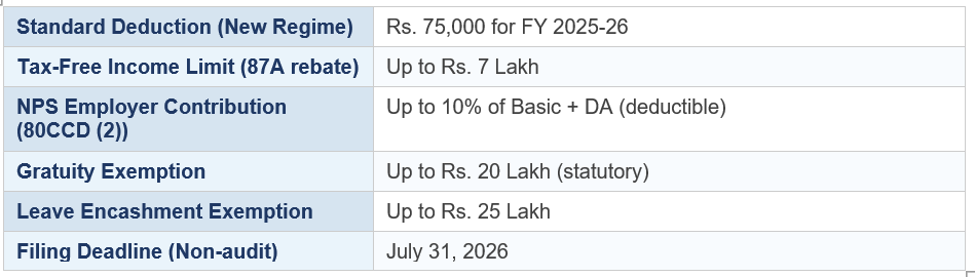

- Standard deduction of Rs. 75,000 applicable under the new regime for FY 2025-26

- NPS employer contribution (Section 80CCD(2)) remains deductible under the new regime

- Exemption on gratuity, leave encashment, VRS proceeds, and certain allowances still available

- Tax rebate under Section 87A makes income up to Rs. 7 lakh tax-free under new regime

- Family pension deduction and disability benefits remain available

- HRA, 80C, 80D deductions not available under new regime — timing of regime choice is critical

📋 Quick Facts

📰 The Story

As the ITR filing season for FY 2025-26 opens, millions of salaried employees are navigating the new tax regime — which became the default option from FY 2023-24 onwards under the Finance Act 2023. While the new regime offers simpler, lower tax slabs, it strips away most of the familiar deductions under Chapter VI-A (80C, 80D, 80G, HRA, etc.), leaving many taxpayers wondering how to meaningfully reduce their liability.

The good news: even within the new regime, there are seven legitimate avenues to reduce taxable income — some of which are frequently overlooked. Understanding these can make a significant difference to the final tax outgo, particularly for those in the Rs. 10–15 lakh income bracket where marginal planning pays the highest dividend.

First, the standard deduction of Rs. 75,000 is automatically available under the new regime — no action required. This applies to all salaried employees and reduces gross salary income before tax computation. Second, employer contributions to the National Pension System (NPS) under Section 80CCD(2) remain deductible up to 10% of Basic salary plus Dearness Allowance, or 14% for central government employees. This is a powerful planning lever, especially if employees can negotiate with employers to restructure CTC to increase NPS employer contribution.

Third, gratuity received on retirement or resignation is exempt up to Rs. 20 lakh for covered employees under the Payment of Gratuity Act, and entirely tax-free for government employees. Fourth, leave encashment on retirement is exempt up to Rs. 25 lakh for non-government employees and fully exempt for government employees. Fifth, Voluntary Retirement Scheme (VRS) compensation is exempt up to Rs. 5 lakh. Sixth, income from agniveer corpus fund is fully exempt — relevant for those who have served under the Agnipath scheme. Seventh, a deduction for family pension income is available at one-third of pension or Rs. 15,000 — whichever is lower.

There are also certain allowances that remain exempt under the new regime, including transport allowance for specially-abled employees, conveyance reimbursements for official duty, and specific perquisites under Rule 3B. Investors and salaried employees should also note that Section 87A rebate makes income up to Rs. 7 lakh entirely tax-free under the new regime — making it compelling for those in lower income brackets.

The critical decision for FY 2025-26 ITR filers is regime selection itself. The new regime is default, but employees can revert to the old regime at the time of ITR filing if it results in lower tax — particularly for those with high HRA, home loan interest, and significant 80C investments. A tax comparison spreadsheet for both regimes is strongly recommended before filing.

📊 Financial Analysis

The new tax regime has fundamentally shifted the tax planning calculus for salaried employees. Under the old regime, the Rs. 1.5 lakh 80C limit, home loan interest deduction (Section 24), and HRA exemptions created a complex but lucrative deduction framework. The new regime trades these for lower slab rates and simplicity.

At an income of Rs. 12 lakh, the new regime results in a tax of approximately Rs. 80,000 (after standard deduction and 87A adjustments), while the old regime could result in Rs. 0 for a taxpayer with Rs. 2.5 lakh in 80C investments, Rs. 1.8 lakh HRA exemption, and Rs. 60,000 in 80D premiums. The crossover point — where the new regime becomes more beneficial — typically falls around Rs. 15–17 lakh for taxpayers who do not maximise old regime deductions.

The NPS employer contribution angle deserves special mention: by restructuring CTC to include a larger NPS employer component, employees can reduce their taxable salary while building a retirement corpus — a double-benefit that works entirely within the new regime framework.

💹 Investor Insights

For investors who are also salaried employees, the regime choice has portfolio implications. Under the old regime, tax-saving instruments (ELSS, PPF, NPS) were incentivised. Under the new regime, the same investments remain rational on their own merits but lose the immediate tax-saving advantage, potentially freeing up capital for more liquid, market-linked investments.

From a wealth management perspective, the new regime works best for younger employees with lower deductions, while the old regime continues to favour those with mortgages, large insurance portfolios, and consistent 80C investments. Certified financial planners recommend a regime comparison at the start of each fiscal year as part of annual tax planning.

Frequently Asked Questions (FAQs)

- Can I switch back from the new regime to the old regime while filing ITR for FY 2025-26?

- Yes — salaried employees (without business income) can choose between regimes at the time of ITR filing each year. However, if your employer has already deducted TDS under a particular regime, you will need to claim any refund (or pay any additional tax) at the time of filing.

- Is Section 80C completely disallowed in the new regime?

- Yes. Deductions under Section 80C (PPF, ELSS, NSC, life insurance premiums, etc.) are not available under the new tax regime. However, the investments themselves remain valid and can continue for wealth creation purposes — they simply will not reduce your taxable income under the new regime.

- What is the maximum tax benefit available under the new regime for a salaried employee?

- The standard deduction (Rs. 75,000) and Section 87A rebate (income up to Rs. 7 lakh) are the most impactful. Add NPS employer contribution deduction, and a well-structured CTC can result in significantly lower effective tax rates compared to the headline slab rates.

- Should I opt for the new or old regime?

- This depends entirely on your individual deduction profile. Run a comparison: if your total old-regime deductions exceed approximately Rs. 3.5–4 lakh (80C + HRA + home loan interest + 80D), the old regime is likely more beneficial. Below that threshold, the new regime's lower slab rates typically win.