Key Takeaways

- FCNR(B) accounts eliminate currency risk and are ideal for foreign-currency savings.

- NRE accounts are best for transferring and managing overseas income in India.

- NRO accounts are mandatory for handling income earned within India.

- FCNR(B) and NRE accounts offer full repatriation benefits, while NRO accounts have regulatory limits.

- Rising FCNR(B) rates in 2026 have made them increasingly attractive for NRIs seeking higher returns and currency protection.

FCNR(B) vs NRE vs NRO: Which Account Should NRIs Choose?

The recent surge in Foreign Currency Non-Resident (Bank) [FCNR(B)] deposit rates, with some banks such as HDFC Bank offering up to 6% for longer tenures, has renewed interest among Non-Resident Indians (NRIs) looking to optimize their savings and investments in India.

For NRIs, choosing between an FCNR(B), NRE, and NRO account is not merely about earning higher returns. The decision depends on several factors including currency risk, taxation, repatriation flexibility, source of income, and future financial goals.

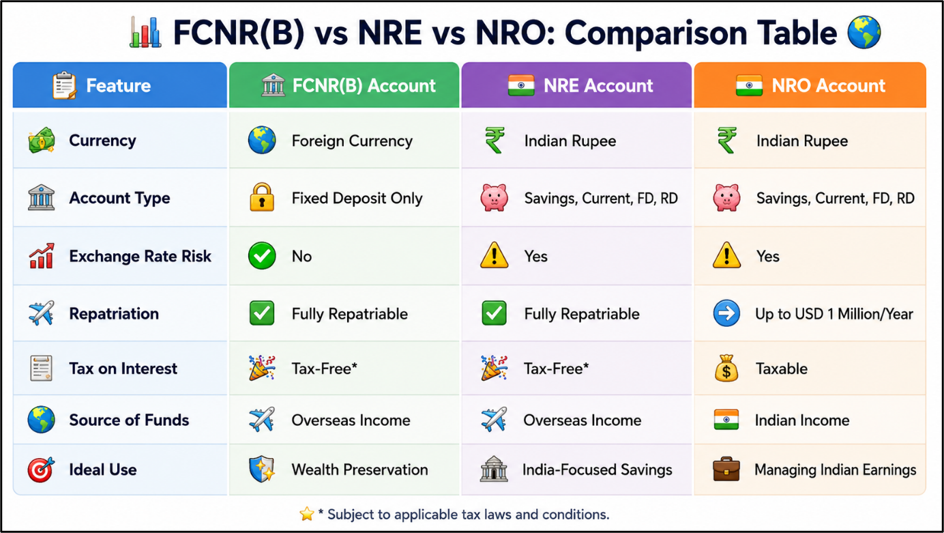

Understanding the Three NRI Account Types

- FCNR(B) Account

An FCNR(B) account is a fixed deposit account maintained in foreign currency such as USD, GBP, EUR, CAD, AUD, or JPY. Since the deposit remains in foreign currency, the depositor is protected from fluctuations in the Indian rupee.

Key Features

- Maintained in foreign currency

- Available only as a term deposit

- No currency conversion risk

- Principal and interest are fully repatriable

- Interest income is tax-free in India for eligible NRIs

- Tenure generally ranges from 1 to 5 years

Best Suited For

- NRIs earning and spending in foreign currencies

- Investors expecting rupee depreciation

- Individuals saving for overseas education, retirement, or property purchases abroad

- NRIs seeking currency protection and stable returns

- NRE (Non-Resident External) Account

An NRE account allows NRIs to park overseas earnings in Indian rupees. These accounts can be opened as savings, current, recurring, or fixed deposit accounts.

Key Features

- Maintained in Indian rupees

- Fully repatriable

- Interest income is tax-free in India

- Can hold foreign income remitted to India

- Greater liquidity compared to FCNR(B) deposits

Best Suited For

- NRIs who regularly transfer money to India

- Individuals planning future spending in India

- Investors seeking higher rupee-denominated deposit rates

- NRIs managing family expenses in India

- NRO (Non-Resident Ordinary) Account

An NRO account is designed for managing income earned in India, such as rent, dividends, pension, interest income, or property sale proceeds.

Key Features

- Maintained in Indian rupees

- Used for Indian-source income

- Repatriation capped at USD 1 million per financial year (subject to regulations)

- Interest is taxable in India

- Suitable for domestic financial transactions

Best Suited For

- NRIs receiving rental income from Indian properties

- Individuals receiving pension payments in India

- Investors earning dividends or interest from Indian assets

- NRIs managing local financial commitments

Why FCNR(B) Deposits Are Back in Focus

The RBI recently introduced measures to encourage foreign currency inflows, including bearing hedging costs on certain FCNR(B) deposits. This has prompted banks to raise FCNR(B) rates significantly. Experts expect banks to aggressively attract NRI funds through competitive FCNR(B) offerings.

Additionally, some banks have raised FCNR(B) rates to around 6% for longer tenures, making these deposits more attractive than before.

However, experts caution that excessive dependence on FCNR(B) deposits could create refinancing challenges when large deposits mature simultaneously.

Which Account Should You Choose?

Choose FCNR(B) If:

- You earn and spend primarily in foreign currency

- You want protection from rupee depreciation

- You are saving for overseas goals

- You prefer fixed returns with lower currency risk

Choose NRE If:

- You regularly send money to India

- You plan future spending or investments in India

- You need a flexible savings account

- You want full repatriation benefits

Choose NRO If:

- You earn rental income in India

- You receive pension, dividends, or interest in India

- You need to manage Indian financial obligations

- You own property or investments in India

For Most NRIs

Financial planners often recommend maintaining a combination of all three accounts:

- NRE Account for overseas earnings transferred to India

- NRO Account for income generated within India

- FCNR(B) Deposits for foreign-currency savings and diversification

This approach provides liquidity, tax efficiency, and currency diversification.

Frequently Asked Questions (FAQs)

- What is the main difference between FCNR(B), NRE and NRO accounts?

FCNR(B) accounts are maintained in foreign currency, while NRE and NRO accounts are maintained in Indian rupees. NRO accounts are specifically meant for managing income earned in India.

- Which NRI account protects against rupee depreciation?

FCNR(B) accounts provide protection against rupee depreciation because deposits are maintained in foreign currencies.

- Is interest earned on FCNR(B) deposits taxable?

Interest earned on FCNR(B) deposits is generally exempt from Indian income tax for eligible NRIs and RNORs.

- Can NRIs hold all three accounts simultaneously?

Yes. NRIs can maintain FCNR(B), NRE, and NRO accounts at the same time based on their financial requirements.

- Which account is best for rental income from India?

An NRO account is the most suitable option for managing rental income, dividends, pension receipts, and other India-sourced earnings.

- Are FCNR(B) deposits fully repatriable?

Yes. Both principal and interest in FCNR(B) deposits are fully repatriable without restrictions.

- Why are FCNR(B) deposits gaining popularity in 2026?

Higher interest rates, RBI support measures, and protection from currency volatility have increased the attractiveness of FCNR(B) deposits among NRIs.