Highlights

- Consistent repayment behaviour can support a healthier credit profile.

- Lower credit card utilisation may improve lender perception of risk.

- Reviewing credit reports regularly can help identify potential inaccuracies.

For many borrowers, a loan application begins long before approaching a bank or financial institution. Lenders typically evaluate an applicant's credit profile to assess repayment capacity and borrowing behaviour. As a result, maintaining healthy credit habits can play an important role in improving loan eligibility and access to competitive borrowing terms.

While credit scores are influenced by multiple factors, certain financial practices can help borrowers strengthen their overall credit profile over time. Experts note that improvements usually occur gradually and require consistency rather than quick fixes.

Source: Analysis by Kalkine

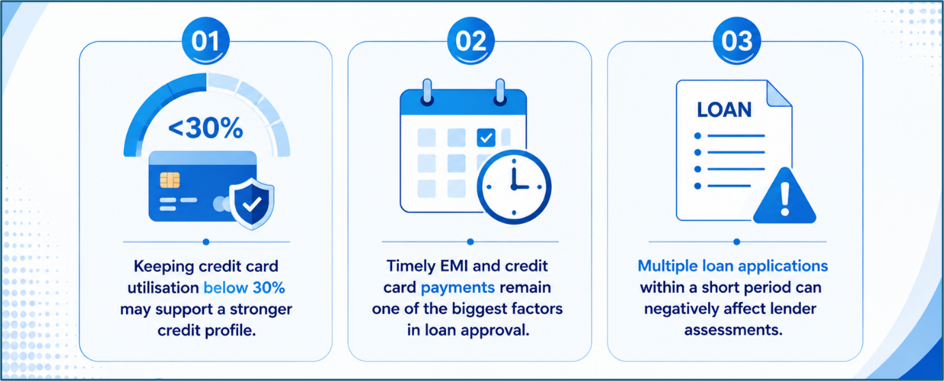

- Prioritise Timely Payments

Repayment history is among the most closely monitored aspects of a credit profile. Delayed EMI payments or missed credit card dues can remain visible in credit records and may influence future lending decisions.

Setting up auto-debit facilities, reminders, or standing instructions can help borrowers avoid missed deadlines. Consistent on-time payments demonstrate responsible credit management and may contribute positively to creditworthiness over time.

- Keep Credit Card Usage Under Control

Credit utilisation refers to the percentage of available credit currently being used. High utilisation levels may indicate greater reliance on borrowed funds and can affect credit assessments.

Many financial experts recommend maintaining utilisation levels below 30% of the available credit limit. Lower utilisation can signal prudent financial management and may support a stronger credit profile.

- Review Credit Reports Periodically

Errors in credit reports can sometimes affect credit scores and loan approvals. Incorrect loan statuses, duplicate accounts, or inaccurately reported payment delays can create unnecessary challenges for borrowers.

Regularly reviewing credit reports allows individuals to identify discrepancies and initiate corrections where necessary. Addressing reporting errors may help ensure that lenders evaluate an accurate financial record.

- Limit Frequent Credit Applications

Every formal application for a loan or credit card can generate a hard enquiry on a credit report. Multiple enquiries within a short period may raise concerns regarding borrowing behaviour.

Instead of applying to several lenders simultaneously, borrowers may benefit from researching eligibility criteria beforehand and applying selectively. This approach can help minimise unnecessary enquiries.

- Maintain a Stable Credit History

The age of credit accounts can also influence a borrower's profile. Older accounts provide lenders with a longer record of financial behaviour, helping them assess repayment consistency over time.

Closing long-standing credit accounts without a specific reason may shorten credit history and affect certain scoring models. Maintaining well-managed accounts can contribute to a more established credit record.

Why Credit Preparation Matters Before a Loan Application

A credit score is not the only factor considered during loan approval. Lenders may also review income stability, existing obligations, repayment patterns, and overall debt levels.

However, borrowers with healthier credit profiles often have a better chance of qualifying for loans and may receive more favourable borrowing terms. Preparing several months before a planned loan application can provide time for positive financial behaviour to be reflected in credit records.

Key Risks

- Missed EMI payments can negatively affect credit records.

- High credit utilisation may weaken borrowing eligibility.

- Frequent credit enquiries can impact lender assessments.

- Unresolved reporting errors may affect loan approvals.

Summary

Borrowers seeking loans can benefit from maintaining healthy credit habits well before submitting an application. Timely repayments, lower credit utilisation, periodic credit report reviews, limited loan enquiries, and a stable credit history are among the factors that contribute to a stronger credit profile. Consistency remains the most important element in building long-term creditworthiness.

FAQs

Q: How important is repayment history for loan approval?

A: Repayment history is a major factor lenders review when assessing a borrower's creditworthiness and financial discipline.

Q: What is considered a healthy credit utilisation ratio?

A: Many experts recommend keeping credit utilisation below 30% of the available credit limit.

Q: Can checking my own credit report reduce my credit score?

A: No, reviewing your own credit report generally does not affect your credit score.