Rate Pause Signals Stability, But FD Investors May Need to Reassess Return Expectations

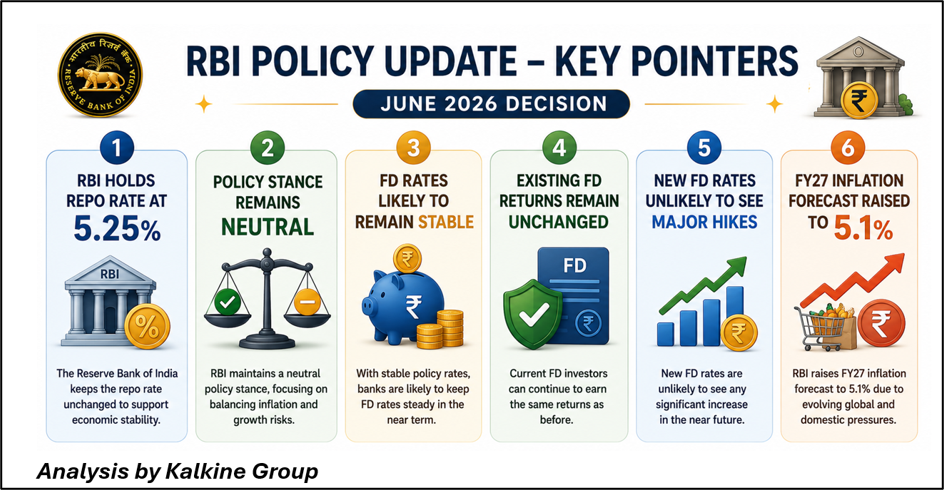

The Reserve Bank of India (RBI) has once again maintained the benchmark repo rate at 5.25%, opting for policy continuity amid rising geopolitical risks, inflation concerns, and global economic uncertainty. While the decision provides stability for borrowers and financial markets, it carries important implications for millions of fixed deposit (FD) investors across the country.

For savers, the message is relatively straightforward: fixed deposit rates are likely to remain broadly stable in the near term, with limited scope for meaningful upward revisions unless inflationary pressures intensify further or the RBI shifts toward a tighter monetary stance.

RBI's Status Quo Keeps Deposit Rate Outlook Steady

The Monetary Policy Committee (MPC) unanimously retained the repo rate at 5.25% while maintaining a neutral stance. At the same time, the RBI raised its inflation forecast and highlighted risks arising from higher crude oil prices, geopolitical tensions, and currency volatility.

Because deposit rates are closely linked to the broader interest-rate cycle, the latest decision suggests that banks are unlikely to aggressively increase FD rates in the immediate future.

What Existing FD Investors Should Know

One of the biggest advantages of fixed deposits is certainty.

Investors who have already locked money into an FD will continue earning the contracted interest rate regardless of future policy changes. The rate agreed upon at the time of investment remains unchanged throughout the tenure of the deposit.

This means:

- Existing FDs remain protected from future rate fluctuations.

- Returns continue as originally contracted.

- Investors do not face reinvestment risk until maturity.

For investors who secured deposits during higher-rate periods, this remains a favorable position.

New FD Investors May Face Limited Upside

For fresh deposits, the outlook appears more balanced.

Since the RBI has neither cut nor raised rates, banks are expected to maintain current deposit pricing structures. While some institutions may offer promotional schemes or selective tenure-based adjustments, a broad-based rise in FD rates appears unlikely at present.

However, investors should also note that the RBI's revised inflation projection of 5.1% for FY27 could reduce real returns if deposit rates fail to keep pace with rising prices.

Are FDs Still Attractive in FY27?

Fixed deposits continue to remain one of the safest investment avenues for conservative investors seeking:

- Capital protection

- Predictable income

- Low volatility

- Portfolio stability

However, the investment landscape is evolving.

With inflation expected to rise and interest rates stabilizing, investors may increasingly evaluate alternative fixed-income instruments that offer potentially better risk-adjusted returns.

Alternative Fixed-Income Options Investors May Consider

- Government Securities (G-Secs)- Government bonds offer sovereign backing and may benefit if bond market participation increases following recent policy initiatives aimed at attracting foreign investment.

- Debt Mutual Funds- Short-duration and corporate bond funds may offer opportunities for investors seeking potentially higher post-tax returns and greater flexibility.

- RBI Floating Rate Savings Bonds- These instruments provide periodic interest-rate resets and may help investors navigate uncertain rate cycles.

- High-Quality Corporate Bonds- For investors willing to assume modest credit risk, select investment-grade bonds may offer yields above traditional bank deposits.

Investment Perspective

The RBI's latest policy decision indicates that policymakers are prioritizing stability while closely monitoring inflation risks arising from global developments. Although immediate changes in FD rates appear unlikely, the inflation outlook suggests investors should focus not only on nominal returns but also on preserving purchasing power.

A diversified fixed-income strategy combining bank deposits, government securities, and professionally managed debt products may help investors navigate a period of moderate inflation and stable interest rates.

Conclusion

The RBI's decision to keep the repo rate unchanged at 5.25% provides near-term certainty for fixed deposit investors. Existing deposit holders can continue enjoying locked-in returns, while new investors are likely to encounter a stable interest-rate environment.

However, with inflation forecast to rise to 5.1% in FY27 and FD rates expected to remain largely unchanged, investors may need to look beyond traditional deposits to optimize real returns. In the current environment, balancing safety, liquidity, and inflation protection will be critical to building an effective income-oriented portfolio.

Frequently Asked Questions (FAQs)

- Will FD interest rates increase after the RBI policy?

The RBI's decision to keep the repo rate unchanged suggests FD rates are likely to remain broadly stable in the near term.

- Will existing FDs be affected by the RBI decision?

No. Existing fixed deposits continue to earn the contracted interest rate until maturity.

- Is this a good time to invest in FDs?

FDs remain suitable for conservative investors seeking capital protection and predictable returns, although inflation may affect real returns.

- What alternatives can investors consider besides FDs?

Government securities, debt mutual funds, RBI savings bonds, and high-quality corporate bonds may provide additional diversification opportunities.

- Why is inflation important for FD investors?

Inflation determines the real return earned after accounting for rising prices. Higher inflation can reduce the purchasing power of fixed-income investments.

- What should investors watch next?

Key factors include inflation trends, crude oil prices, RBI policy guidance, bond yields, and future interest-rate expectations.