Highlights

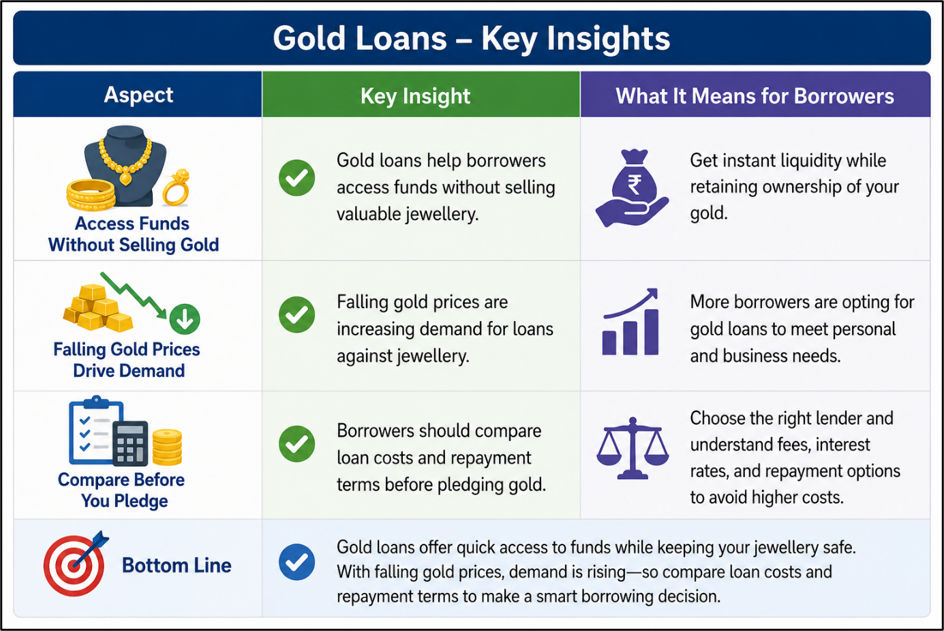

- Households are increasingly pledging old jewellery instead of selling it amid lower gold prices.

- Gold loan demand has risen as borrowers seek liquidity while retaining ownership of their gold.

- Experts expect gold prices to remain range-bound in the near term despite recent corrections.

Gold prices have retreated sharply from their record highs earlier this year, prompting many Indian households to reconsider how they monetise their jewellery. Instead of selling old gold, an increasing number of consumers are opting for gold loans, allowing them to access funds while retaining ownership of their ornaments. The trend reflects changing consumer behaviour as families anticipate that gold prices could recover over time and prefer to keep their long-term holdings intact.

Source: Analysis by Kalkine

Why Are More Households Choosing Gold Loans?

With gold prices correcting by more than 20% from their peak levels, many households believe selling jewellery now could mean missing out if prices rebound in the future. As a result, borrowers are increasingly using their jewellery as collateral to obtain short-term financing instead of liquidating their holdings. Industry data indicates that demand for gold loans has risen significantly compared with the previous year, reflecting consumers' preference to preserve ownership of family assets while meeting immediate cash requirements.

How Gold Loans Work

A gold loan allows borrowers to pledge gold jewellery with a bank or non-banking financial company (NBFC) in exchange for a loan. Once the borrower repays the principal and applicable interest, the pledged jewellery is returned. Since the loan is backed by physical gold, lenders generally process these loans relatively quickly compared with unsecured personal loans. This makes gold loans a common option for individuals seeking short-term liquidity without permanently parting with their jewellery.

Why Are People Avoiding Gold Sales?

Gold has traditionally been viewed as both an investment and a family asset in India. Selling jewellery often becomes a last resort because many ornaments carry emotional or cultural value. The recent decline in prices has encouraged households to hold on to their gold in the expectation that prices may stabilise or recover. By borrowing against jewellery instead of selling it, families retain ownership while meeting financial needs during periods of temporary cash shortages.

What Could Influence Gold Prices Ahead?

Market participants continue to monitor global economic developments, central bank policies, inflation trends, and geopolitical events, all of which influence gold prices. Analysts expect prices to remain within a trading range in the near term, although future movements will depend on international market conditions. Borrowers considering gold loans should remember that lenders periodically reassess collateral values based on prevailing gold prices, which may affect loan-to-value ratios for fresh borrowing.

Should You Borrow or Sell Gold?

The decision depends on individual financial circumstances and repayment capacity. Borrowing against gold may be appropriate for those requiring temporary liquidity and expecting to repay the loan within the agreed tenure. However, borrowers should compare interest rates, processing charges, repayment options, and loan conditions before pledging jewellery. Selling gold may still be considered when repayment is uncertain or when the asset is no longer required, but consumers should evaluate prevailing market prices before making that decision.

Risks to Watch

- Gold price declines may reduce eligible loan amounts.

- Delayed repayments can increase total borrowing costs.

- Loan defaults may result in auction of pledged jewellery.

- Processing charges vary across lending institutions.

Summary

The recent correction in gold prices has encouraged many Indian households to choose gold loans instead of selling old jewellery. Borrowers are using their gold as collateral to access short-term funds while retaining ownership of valuable assets. As gold prices remain volatile, consumers should carefully compare loan terms, repayment obligations, and interest costs before pledging jewellery for financing.

FAQs

Q: Why are households choosing gold loans instead of selling jewellery?

A: Many borrowers expect gold prices to recover and prefer retaining ownership while accessing short-term funds through secured loans.

Q: How does a gold loan work?

A: Borrowers pledge gold jewellery as collateral, receive a loan, and recover their jewellery after repaying the loan and applicable interest.

Q: What should borrowers compare before taking a gold loan?

A: Compare interest rates, loan tenure, processing charges, repayment flexibility, loan-to-value ratio, and lender terms before borrowing.