Highlights

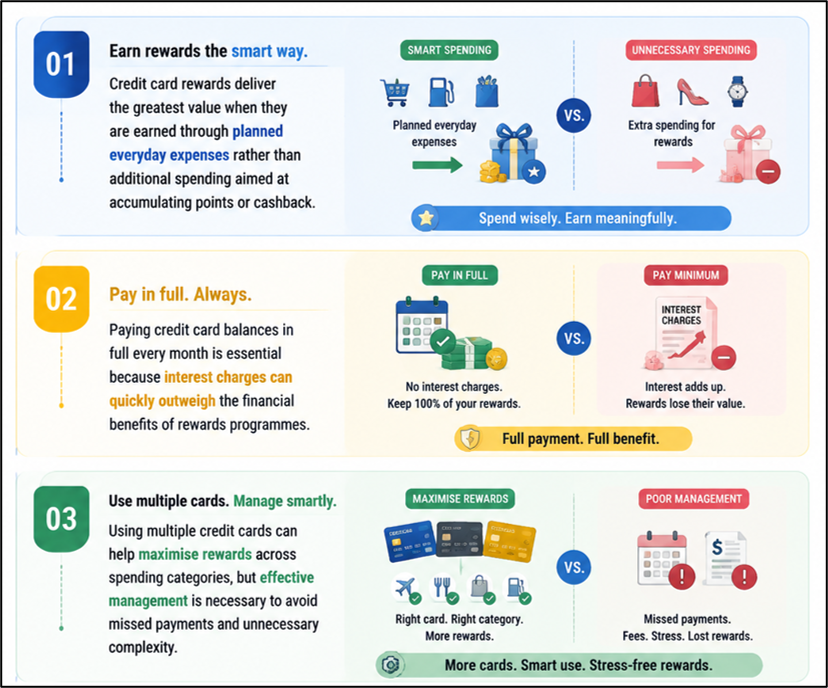

- Reward programmes work best when linked to planned everyday expenses.

- Paying credit card bills in full helps preserve the value of rewards.

- Spending solely for points can reduce overall financial benefits.

Credit cards have become a common part of household finances, offering consumers access to cashback, reward points, travel benefits and shopping discounts. While these incentives can provide additional value, many cardholders fail to make the most of them because they focus on accumulating rewards rather than managing spending effectively.

In many cases, the pursuit of rewards can even encourage unnecessary purchases, reducing the overall financial advantage. Understanding how reward programmes work and using them strategically can help consumers benefit without increasing their expenses.

Source: Analysis by Kalkine

Choose a Card That Matches Spending Habits

Getting the most from a credit card starts with selecting one that aligns with regular spending patterns. Different cards reward different categories such as groceries, fuel, dining, travel or online shopping. A rewards programme is most useful when it complements existing expenses rather than encouraging new ones. Reviewing monthly spending habits before selecting a card can help consumers identify which rewards structure is likely to deliver the greatest value.

Let Everyday Expenses Generate Rewards

Credit card rewards tend to be most effective when earned through purchases that are already part of a household budget. Routine expenses such as utility bills, groceries, fuel costs, insurance premiums and recurring subscriptions can generate rewards without increasing overall spending. Treating rewards as a by-product of planned expenditure rather than a reason to spend more can help cardholders gain benefits while maintaining financial discipline.

Avoid Spending More to Earn More

Many reward programmes include promotional offers, bonus categories and spending milestones that promise additional points or cashback. While these incentives may appear attractive, they can sometimes encourage consumers to make purchases they had not originally planned. Spending additional money simply to unlock a reward can reduce or eliminate any financial gain. The value of rewards should always be weighed against the actual cost of the purchase.

Full Repayment Is Essential

One of the most important aspects of using reward credit cards effectively is paying the outstanding balance in full every month. Credit card interest rates are often significantly higher than the value generated through rewards. If balances are carried forward, interest charges can quickly exceed the benefits earned from cashback or reward points. Maintaining a habit of timely and complete repayment helps ensure that rewards remain a genuine financial advantage.

Understand How Rewards Are Earned

Not all transactions generate rewards at the same rate. Some cards offer accelerated earnings in specific spending categories, while others may place limits on the amount of rewards that can be accumulated. Cardholders who understand these rules are better positioned to maximise benefits. Reviewing programme terms periodically can help users take advantage of available opportunities without altering their spending behaviour.

Keep Track of Reward Validity

Reward points do not always retain their value indefinitely. Some programmes include expiry periods, while others may adjust redemption rates over time. Allowing points to accumulate without a redemption plan can result in missed opportunities. Monitoring reward balances and redeeming benefits when appropriate can help cardholders obtain greater value from their accumulated rewards.

Simplicity Can Be More Effective

While some consumers use multiple credit cards to maximise rewards across different categories, managing numerous accounts can become complicated. Different payment due dates, reward structures and redemption conditions may increase the risk of missed payments or overlooked benefits. A simpler approach involving a limited number of well-chosen cards may be easier to manage and still provide meaningful rewards.

Monitor Spending Regularly

Reward programmes can sometimes create the impression that spending is being offset by future benefits. However, the actual value of points or cashback is often only a small percentage of total expenditure. Regularly reviewing credit card statements and maintaining a budget can help consumers remain focused on overall spending rather than the rewards attached to individual purchases.

Rewards Should Support Financial Goals

The primary purpose of a credit card should be convenience, payment flexibility and financial management. Rewards are an additional benefit, not the main objective. Consumers who use cards within their budgets, repay balances promptly and avoid unnecessary purchases are generally more likely to derive lasting value from reward programmes. A disciplined approach can help ensure that rewards contribute positively to personal finances rather than encouraging excessive spending.

Key Risks

- Overspending to earn rewards can weaken budgeting discipline.

- Interest charges may outweigh cashback and reward benefits.

- Expired points can reduce the value of accumulated rewards.

- Managing multiple cards increases the risk of missed payments.

Summary

Credit card rewards can provide useful financial benefits when earned through planned and necessary spending. Choosing a card that aligns with everyday expenses, paying balances in full and avoiding purchases motivated solely by rewards are important principles for maximising value. Consumers who focus on spending discipline rather than reward accumulation are more likely to benefit from credit card programmes without increasing their financial obligations.

FAQs

Q: What is the simplest way to maximise credit card rewards?

A: Use the card for regular expenses and pay the full balance every month.

Q: Can reward programmes encourage unnecessary spending?

A: Yes, chasing points or cashback can sometimes lead to purchases that were not planned.

Q: Why is full repayment important for reward card users?

A: Interest charges can quickly exceed the financial value of earned rewards.