Highlights

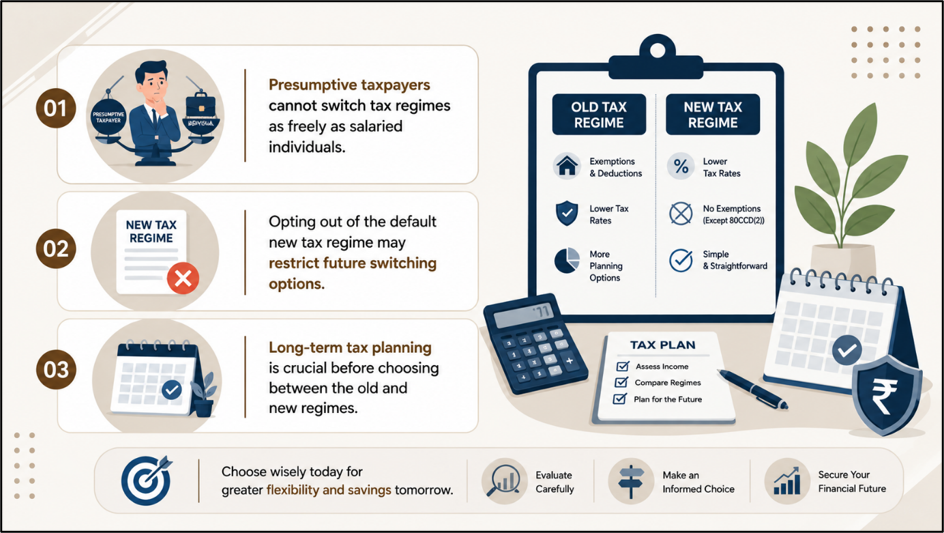

- Presumptive taxpayers face stricter tax regime switching rules than salaried individuals.

- Opting out of the new tax regime can limit future switching flexibility.

- Business and professional income taxpayers should evaluate long-term tax implications carefully.

The choice between the old and new tax regimes has become an important decision for taxpayers filing returns under the presumptive taxation scheme. While salaried individuals generally enjoy greater flexibility in choosing between the two systems, taxpayers reporting business or professional income under presumptive taxation are subject to different rules.

As the new tax regime remains the default option, many small businesses and professionals are assessing whether they can move between the two regimes every year and what restrictions may apply.

Source: Analysis by Kalkine

Who Qualifies as a Presumptive Taxpayer?

Presumptive taxation is available to eligible small businesses and professionals under provisions such as Sections 44AD, 44ADA and 44AE of the Income Tax Act.

The scheme allows taxpayers to declare income at prescribed rates without maintaining detailed books of accounts, reducing compliance requirements for eligible taxpayers.

Can Presumptive Taxpayers Switch Every Year?

The rules for switching tax regimes differ depending on the nature of income. Taxpayers with only salary or non-business income can generally choose between the old and new tax regimes every financial year. However, taxpayers earning business or professional income, including those using presumptive taxation provisions, do not have the same flexibility.

For taxpayers with business or professional income, opting out of the new tax regime and shifting to the old regime triggers specific restrictions on future regime changes. As a result, the decision should be made after considering long-term tax planning requirements.

Why the Restriction Exists

The government introduced these provisions to prevent frequent switching between tax regimes based solely on annual tax advantages.

Since business taxpayers often claim deductions, depreciation and other tax benefits that can influence taxable income significantly, the law imposes tighter rules on regime changes compared with salaried taxpayers.

Consequently, a taxpayer filing under presumptive taxation should assess future income levels, investment plans and eligible deductions before making a regime selection.

Factors to Consider Before Switching

Before deciding whether to remain in the default new tax regime or opt for the old regime, presumptive taxpayers may consider:

- Availability of deductions and exemptions.

- Expected business income in future years.

- Investment and tax-saving plans.

- Long-term compliance requirements.

- Impact on overall tax liability.

A decision based only on one year's tax outcome may not always be beneficial if future switching options become restricted.

Filing Requirements

Taxpayers reporting presumptive income generally use ITR-4, subject to eligibility conditions. Recent compliance changes have also increased disclosure requirements for certain presumptive taxpayers, making accurate reporting increasingly important.

Where taxpayers intend to opt out of the default tax regime, they may need to complete the prescribed procedural requirements before filing their returns.

Planning for the Long Term

For presumptive taxpayers, choosing between the old and new tax regimes is more than an annual filing decision. Since future switching flexibility may be limited, taxpayers should evaluate both immediate tax savings and long-term implications before making a selection.

A careful comparison of expected deductions, income trends and future tax obligations can help determine the more suitable regime.

Key Risks to Watch

- Switching without long-term planning may reduce future flexibility.

- Ignoring deduction eligibility can increase tax liability.

- Incorrect regime selection may require additional compliance steps.

- Failure to meet filing requirements can create reporting issues.

Summary

Presumptive taxpayers do not enjoy the same annual switching flexibility available to salaried individuals. Taxpayers with business or professional income who choose to move away from the default new tax regime may face restrictions on future regime changes. Therefore, selecting between the old and new tax systems requires a long-term assessment of income patterns, deductions, and compliance requirements rather than focusing solely on immediate tax savings.

FAQs

Q: Can presumptive taxpayers switch between tax regimes every year?

A: Generally, taxpayers with business or professional income face restrictions that do not apply to salaried taxpayers.

Q: Is the new tax regime the default option?

A: Yes, the new tax regime is currently the default regime for eligible taxpayers.

Q: Does presumptive taxation work under both tax regimes?

A: Yes, presumptive taxation provisions are available under both the old and new tax regimes.