Highlights

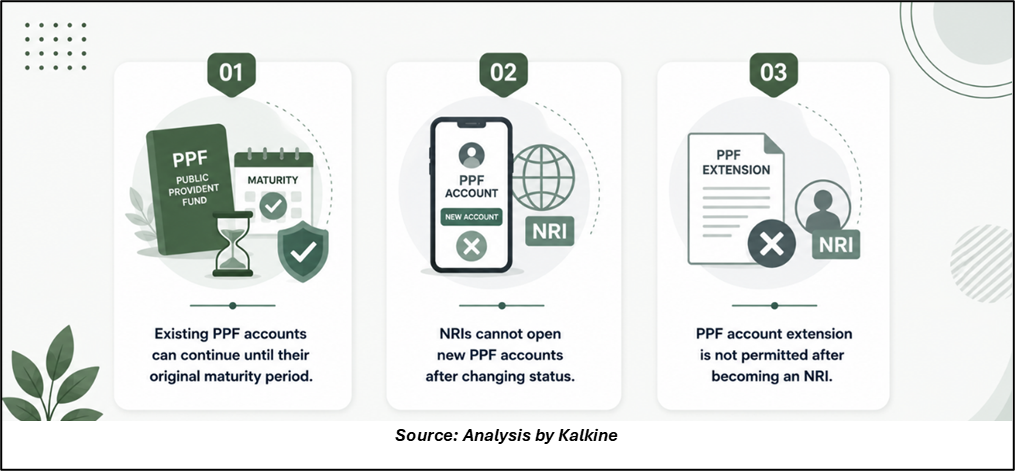

- Existing PPF accounts can continue until their original maturity date.

- NRIs cannot open new PPF accounts after changing residential status.

- PPF accounts cannot be extended beyond maturity once you become an NRI.

For many Indians moving overseas for work, education, or long-term settlement, managing existing financial investments becomes an important part of the transition. One common concern relates to the Public Provident Fund (PPF), a long-term savings scheme widely used for retirement and wealth accumulation.

Becoming a Non-Resident Indian (NRI) does not automatically require closure of an existing PPF account. However, the rules governing the account change once an individual's residential status shifts from resident to non-resident under applicable regulations. Understanding these rules can help avoid compliance issues and ensure smooth management of the investment.

Can NRIs Open A New PPF Account?

New Accounts Are Not Permitted- Once an individual becomes an NRI, opening a fresh PPF account is not allowed. The scheme is available only to resident Indians for new account openings. Therefore, individuals planning to move abroad cannot open a new PPF account after their residential status changes.

This restriction applies regardless of the country of residence or the duration of overseas stay.

What Happens To An Existing PPF Account?

Existing Accounts Can Continue - If a PPF account was opened while the individual was a resident Indian, the account can continue until its original maturity period of 15 years even after the account holder becomes an NRI. Contributions can continue during this period, subject to the existing annual investment limits and scheme rules.

This provision allows account holders to continue earning the applicable PPF interest rate until maturity without disrupting long-term financial plans.

Inform The Bank About Status Change - Financial experts advise account holders to notify the bank or post office about the change in residential status after becoming an NRI. The associated savings account may need to be converted into an appropriate NRI account category in accordance with foreign exchange regulations.

Keeping account records updated can help avoid administrative issues later, particularly when the account reaches maturity.

Can NRIs Continue Making Contributions?

Contributions Remain Permitted - NRIs can continue depositing funds into an existing PPF account that was opened before they acquired NRI status. The annual contribution rules remain unchanged and continue to apply until maturity.

However, investors should ensure that contributions are made through permissible banking channels and that account records accurately reflect their current residential status.

What Happens At Maturity?

Extension Is Not Allowed - One of the most important changes after becoming an NRI relates to account extension. Resident account holders have the option to extend a PPF account in blocks of five years after the initial maturity period. However, NRIs are not eligible for this extension facility. Once the original 15-year tenure ends, the account must be closed and the proceeds withdrawn.

This restriction often surprises account holders who assume that extension rules remain unchanged after moving abroad.

Maturity Proceeds

Upon maturity, the accumulated corpus is generally credited to the account holder's designated NRO account. The proceeds are then subject to the applicable rules governing NRO account balances and fund remittances.

Investors should coordinate with their bank well before maturity to ensure a smooth transfer process.

Tax And Repatriation Considerations

Understand Local Tax Rules

While PPF enjoys tax advantages under Indian regulations, NRIs should also consider the tax treatment of investment income in their country of residence. Some jurisdictions may treat PPF earnings differently for taxation purposes.

Tax obligations vary across countries, making it important to evaluate local regulations when planning overseas finances.

Repatriation Rules Matter

Although maturity proceeds are credited to an NRO account, subsequent overseas remittance is governed by RBI and FEMA regulations applicable to NRO balances. Investors should understand the documentation and compliance requirements before planning transfers abroad.

Planning Ahead Before Relocating

Individuals preparing to move overseas should review all existing financial products, including PPF accounts, bank accounts, insurance policies, and investments. Updating residential status, nomination details, and contact information can help avoid complications later.

For PPF investors, the key takeaway is that an existing account remains operational until maturity, but certain benefits available to resident Indians, particularly account extension, are no longer available after becoming an NRI.

Key Risks

- Failure to update NRI status may create compliance issues.

- PPF account extension is unavailable after becoming an NRI.

- Overseas tax rules may affect overall returns.

- Maturity proceeds require compliance with NRO account regulations.

Summary

Moving abroad does not require closure of an existing PPF account. Individuals who opened a PPF account while residents can continue contributing and earning interest until the original 15-year maturity period. However, NRIs cannot open new PPF accounts and are not allowed to extend existing accounts after maturity. Understanding contribution, maturity, and repatriation rules can help ensure smooth management of PPF investments after relocation abroad.

FAQs

Q: Can I keep my existing PPF account after becoming an NRI?

A: Yes, an existing PPF account can continue until its original maturity date after becoming an NRI.

Q: Can NRIs open a new PPF account after moving abroad?

A: No, NRIs are not permitted to open fresh PPF accounts under current regulations.

Q: Can an NRI extend a PPF account after the initial 15-year maturity period?

A: No, extension beyond the original maturity period is not available to NRIs.