Highlights

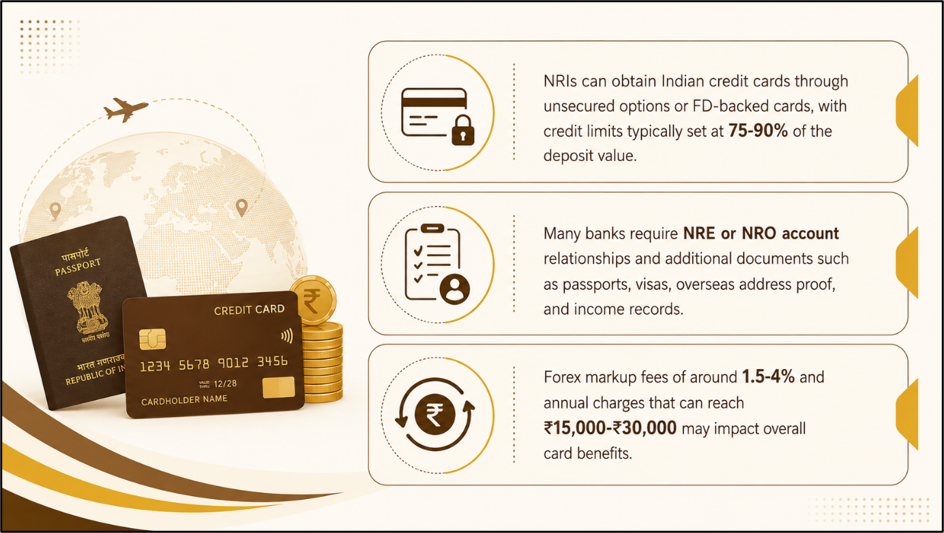

- NRIs can obtain Indian credit cards through unsecured or FD-backed options.

- Banks often require NRE or NRO relationships and additional documentation.

- Forex charges and annual fees can affect overall card benefits.

For many Non-Resident Indians (NRIs), maintaining financial connections with India remains important for family expenses, subscriptions, travel, and everyday transactions. One common question among overseas Indians is whether they can obtain an Indian credit card. The answer is yes, but the process differs from that followed by resident Indians.

Several Indian banks now offer credit cards specifically designed for NRIs. However, eligibility requirements, documentation standards, and approval procedures can vary significantly across lenders. Applicants may also face additional compliance requirements related to residency status and banking relationships.

Source: Analysis by Kalkine

Understanding NRI Credit Card Eligibility

Indian banks generally offer two routes through which NRIs can obtain credit cards.

The first option is an unsecured credit card, where approval depends on factors such as the applicant's banking relationship, overseas income, account balances, and overall financial profile. Some banks evaluate the Total Relationship Value (TRV), which includes balances maintained across NRE accounts, NRO accounts, and fixed deposits.

Banks may also request overseas income proof, foreign bank statements, passport details, visa documents, and proof of overseas residence before considering an application.

The Role of NRE and NRO Accounts

Many lenders prefer applicants to maintain NRE or NRO accounts with the bank issuing the card. These accounts help banks assess the customer's financial standing and facilitate billing and repayment processes.

A banking relationship may improve eligibility for certain premium card categories, particularly where minimum relationship balances are required. However, requirements vary among institutions, and applicants should verify specific conditions before applying.

FD-Backed Credit Cards: An Alternative Route

For NRIs who may not meet unsecured card eligibility requirements, fixed deposit-backed credit cards provide an alternative.

Under this structure, the applicant opens a fixed deposit linked to an NRE or NRO account. The credit limit is generally set at approximately 75% to 90% of the deposit value, depending on the bank's policies.

Because the fixed deposit serves as collateral, banks may not require extensive income verification. The deposit also continues earning interest while remaining pledged against the credit card. Approval rates for such cards are often higher compared to unsecured products.

Documentation and Verification Requirements

The documentation process for NRIs typically includes:

- Valid passport

- Visa or residence permit

- Overseas address proof

- Income documents, where applicable

- Bank statements

- KYC verification documents

Many banks continue to require completion of Know Your Customer (KYC) procedures before issuing a card. Depending on the institution, verification may involve biometric authentication, video KYC, or physical verification. Some applicants may need to complete parts of the process while visiting India.

Fees and Overseas Usage Considerations

Before selecting an Indian credit card, NRIs should evaluate both annual fees and foreign transaction costs.

Premium cards can carry annual fees ranging from INR 15,000 to INR 30,000, excluding applicable taxes. In addition, overseas transactions may attract forex markup charges that can range from approximately 1.5% to 4%.

These costs can reduce the effective value of reward points, cashback benefits, or travel-related perks. As a result, applicants should compare reward structures against forex charges when evaluating card suitability.

Family Usage and Add-On Cards

Indian credit cards can also help NRIs manage family expenses within India. Many banks permit primary NRI cardholders to issue add-on cards to eligible family members.

This feature can provide a convenient way to manage recurring household expenses while maintaining spending oversight from abroad. However, add-on card rules differ among banks and should be reviewed before application.

Key Risks

- Forex charges can reduce the value of rewards on overseas spending.

- Premium annual fees may outweigh benefits for low-spending users.

- Physical KYC requirements can delay card issuance.

- Approval criteria vary significantly across banks and card categories.

Summary

NRIs can obtain Indian credit cards through unsecured products or fixed deposit-backed options. Banks generally evaluate account relationships, documentation, income details, and KYC compliance before approval. While these cards can help manage expenses in India and abroad, applicants should assess annual fees, forex charges, and eligibility conditions carefully before selecting a suitable credit card.

FAQs

Q: Can NRIs apply for Indian credit cards while living abroad?

A: Yes, many Indian banks allow NRIs to apply, subject to documentation, banking relationship, and KYC requirements.

Q: What is an FD-backed credit card for NRIs?

A: It is a credit card issued against a fixed deposit, with limits linked to deposit value.

Q: Do NRIs need an NRE or NRO account for credit cards?

A: Many banks prefer or require NRE or NRO accounts for processing, billing, and repayment purposes.