Highlights

- A higher down payment can reduce borrowing costs but affect liquidity.

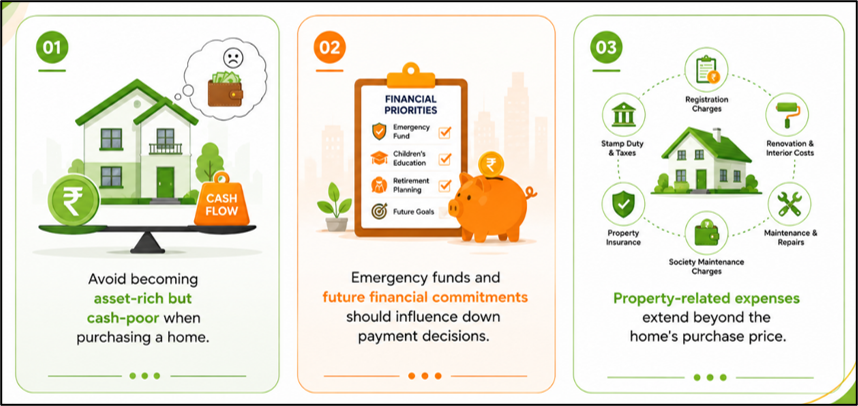

- Homebuyers should balance property ownership goals with emergency savings needs.

- Using all available savings for a down payment can create financial stress.

A down payment is the portion of a property's purchase price that a homebuyer pays upfront from personal funds, while the remaining amount is financed through a home loan. In India, lenders typically finance a percentage of the property's value, requiring buyers to contribute the balance themselves.

While making a larger down payment can reduce the size of the loan, financial planners often caution against committing all available savings to a property purchase. Maintaining adequate liquidity remains an important part of overall financial planning.

Source: Analysis by Kalkine

Why A Bigger Down Payment Is Not Always Better

Many homebuyers aim to maximize their down payment to lower their loan burden. A larger upfront contribution can reduce monthly EMIs, decrease interest costs over the loan tenure, and improve the loan-to-value ratio.

However, allocating most of one's savings toward a property purchase can create liquidity challenges. Once funds are invested in real estate, accessing them quickly may not be easy. Property is generally considered a relatively illiquid asset compared with cash, fixed deposits, or other financial investments.

The Risk Of Becoming Asset-Rich But Cash-Poor

A common concern among financial planners is the possibility of becoming "asset-rich but cash-poor." This occurs when a significant portion of an individual's wealth is tied up in assets such as real estate while readily available cash remains limited.

In such situations, unexpected expenses including medical emergencies, job loss, education costs, or major repairs can place financial pressure on households. Without adequate liquid reserves, individuals may need to borrow again or sell investments at unfavorable times.

Striking The Right Balance

Preserve Emergency Savings

Before deciding on a down payment amount, buyers may consider setting aside an emergency fund capable of covering several months of essential expenses. This reserve can help manage unforeseen events without disrupting long-term financial plans.

Account For Additional Property Costs

The purchase price is not the only expense associated with buying a home. Registration charges, stamp duty, legal fees, furnishing expenses, maintenance deposits, and moving costs can significantly increase the total financial commitment.

Buyers should ensure that sufficient funds remain available after accounting for these additional expenses.

Consider Future Financial Goals

A home purchase should not completely derail other financial objectives. Retirement planning, children's education, insurance requirements, and investment goals may continue even after a property purchase.

Maintaining a balance between home ownership and other financial priorities can support long-term financial stability.

Evaluating The Loan Burden

The ideal down payment often depends on individual financial circumstances rather than a fixed percentage.

A larger down payment may reduce EMI obligations and overall interest costs. On the other hand, retaining some savings can provide flexibility and financial security. Buyers should assess income stability, future cash flow requirements, existing liabilities, and risk tolerance before deciding on the amount to contribute upfront.

Factors That Can Influence The Decision

Income Stability

Individuals with stable income sources may be more comfortable maintaining moderate liquidity while servicing a home loan. Those with variable income may prefer larger cash reserves.

Existing Investments

The composition of an investor's portfolio can influence the decision. If a significant portion of wealth is already concentrated in real estate, maintaining liquidity elsewhere may become even more important.

Interest Rate Environment

Home loan interest rates affect the long-term cost of borrowing. Changes in borrowing costs may influence how buyers balance loan amounts and upfront contributions.

A Practical Approach To Home Buying

Rather than targeting the largest possible down payment, many financial experts suggest focusing on affordability and liquidity together. The objective is not only to qualify for a home loan but also to maintain financial flexibility after purchasing the property.

A sustainable home-buying strategy generally considers EMI affordability, emergency preparedness, future goals, and the ability to manage unexpected financial situations.

Key Risks To Consider

- Using all savings may leave inadequate emergency reserves.

- Additional property costs can strain household finances.

- Income disruptions may affect EMI repayment capacity.

- Excessive real estate exposure can reduce portfolio diversification.

Summary

An ideal home loan down payment is one that balances borrowing costs with financial flexibility. While a larger down payment can reduce EMIs and interest expenses, using most available savings may create liquidity challenges. Homebuyers should preserve emergency funds, account for transaction-related expenses, and consider future financial goals before deciding how much to contribute upfront. The right amount ultimately depends on income stability, financial commitments, and long-term planning needs.

FAQs

Q: Does a larger down payment always make financial sense?

A: Not necessarily. While it reduces loan size, it may also reduce liquidity needed for emergencies and future goals.

Q: Why is maintaining liquidity important after buying a home?

A: Adequate liquidity helps manage emergencies, unexpected expenses, and financial disruptions without taking additional debt.

Q: What factors should determine the ideal down payment amount?

A: Income stability, emergency savings, future goals, existing liabilities, and overall financial flexibility should guide the decision.