Highlights

- Filing income tax returns early can help taxpayers receive refunds sooner.

- Timely filing reduces exposure to penalties, interest, and compliance issues.

- Updated tax records support loan applications and financial planning activities.

The annual income tax return (ITR) filing process is a key financial responsibility for millions of taxpayers. While the filing deadline for most individual taxpayers is July 31, 2026, many people postpone the task until the final days. However, completing the process early can provide several practical advantages beyond simply meeting a regulatory requirement.

Early filing allows taxpayers to organize their finances more effectively, avoid last-minute complications, and ensure that tax-related records remain up to date. It can also make future financial transactions smoother and reduce the likelihood of filing errors.

Source: Analysis by Kalkine

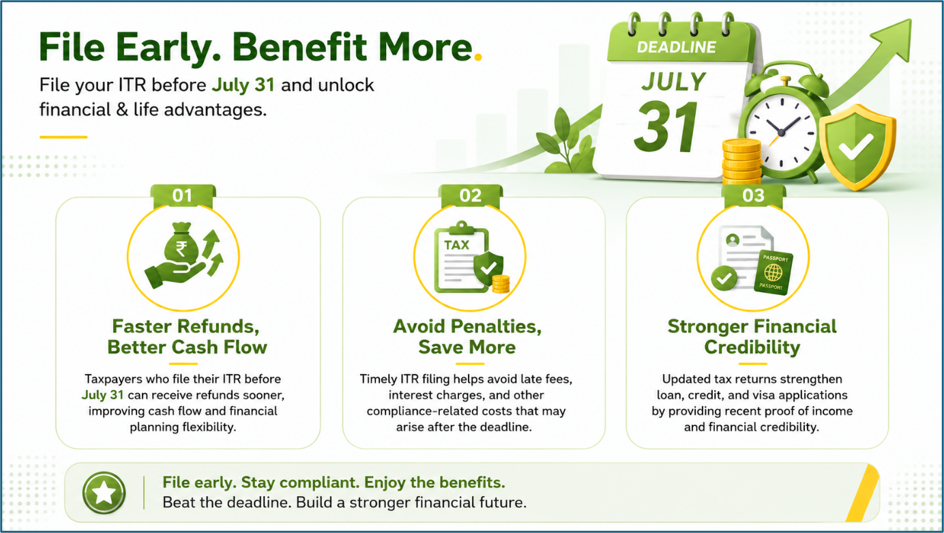

Early Refunds Can Improve Cash Flow

Taxpayers eligible for refunds often benefit from filing returns as soon as they have all necessary documents in place. Earlier submission generally allows tax authorities to begin processing the return sooner, which may lead to faster refund disbursement.

For individuals relying on refunds for investments, savings, or planned expenses, receiving the amount earlier can improve cash flow management and reduce uncertainty.

Avoid Additional Charges and Compliance Costs

Missing the prescribed filing deadline can result in financial consequences. Depending on the circumstances, taxpayers may face late filing fees and interest charges on unpaid tax liabilities.

Submitting the return before the due date helps eliminate these additional costs. It also ensures that taxpayers remain compliant with tax regulations and avoid complications associated with delayed filings.

Better Preparation for Financial Requirements

Income tax returns are frequently used as proof of income when applying for loans, credit facilities, or visas. Financial institutions often review tax records to assess an applicant's financial profile.

Having the latest return filed and available can simplify documentation requirements and reduce delays during application processes. Updated tax records also contribute to greater financial transparency.

More Time to Review and Correct Information

Rushing through the filing process at the last moment increases the possibility of mistakes. Errors in income reporting, deduction claims, tax credits, or personal information can lead to future compliance issues.

Taxpayers who file early have more time to verify information, reconcile documents, and address discrepancies before the deadline. This reduces the chances of receiving notices related to avoidable mistakes.

Improved Financial Organization

Preparing an income tax return requires reviewing income sources, investments, deductions, and tax payments. This exercise often provides a clearer understanding of an individual's financial position.

Completing the process early allows taxpayers to organize records efficiently and begin planning for the next financial year. It also helps maintain a structured record of financial activities that may be useful in future transactions.

Avoid Last-Minute Filing Stress

As filing deadlines approach, online tax portals often experience increased traffic due to a surge in submissions. Taxpayers who wait until the final days may face technical challenges, slower system response times, or document-related issues.

Early filing minimizes these risks and provides flexibility if additional information or corrections are required. It also reduces the pressure associated with completing important financial tasks under tight timelines.

Timely Filing Supports Long-Term Compliance

Regular and timely tax filing contributes to a consistent compliance history. Maintaining accurate and up-to-date tax records can be beneficial when responding to future tax-related queries or documentation requirements.

For taxpayers seeking a smooth filing experience, completing returns before the July 31 deadline remains a practical approach that combines compliance with better financial management.

Key Risks of Delaying ITR Filing

- Late fees can increase the overall tax burden.

- Interest may accrue on unpaid tax liabilities.

- Refund receipt could be delayed considerably.

- Last-minute technical issues may disrupt filing.

Summary

Filing an income tax return before July 31, 2026, offers several advantages, including faster refund processing, avoidance of penalties, improved documentation, and better financial organization. Early filing also provides sufficient time to identify and correct errors while reducing dependence on deadline-day submissions. For many taxpayers, completing the process in advance can simplify compliance and support more effective financial planning throughout the year.

FAQs

Q: What is the primary benefit of filing an ITR early?

A: Early filing may lead to quicker refund processing and provides more time to address filing issues.

Q: Can delayed filing result in additional costs?

A: Yes, taxpayers may face late fees and interest charges if applicable deadlines are missed.

Q: Why are income tax returns important for financial applications?

A: Lenders and institutions often use ITR records to evaluate income history and financial credibility.