Highlights

- Starting SIP investments earlier can significantly reduce monthly contribution requirements.

- Delayed investing often requires substantially higher monthly investments to reach the same goal.

- Compounding works best when investments are given more time to grow.

Many investors focus on selecting the right mutual fund or investment product, but often overlook one of the most important factors in wealth creation: time. The difference between starting a Systematic Investment Plan (SIP) at age 30 versus age 45 can translate into a substantial increase in the monthly investment needed to achieve the same financial goal.

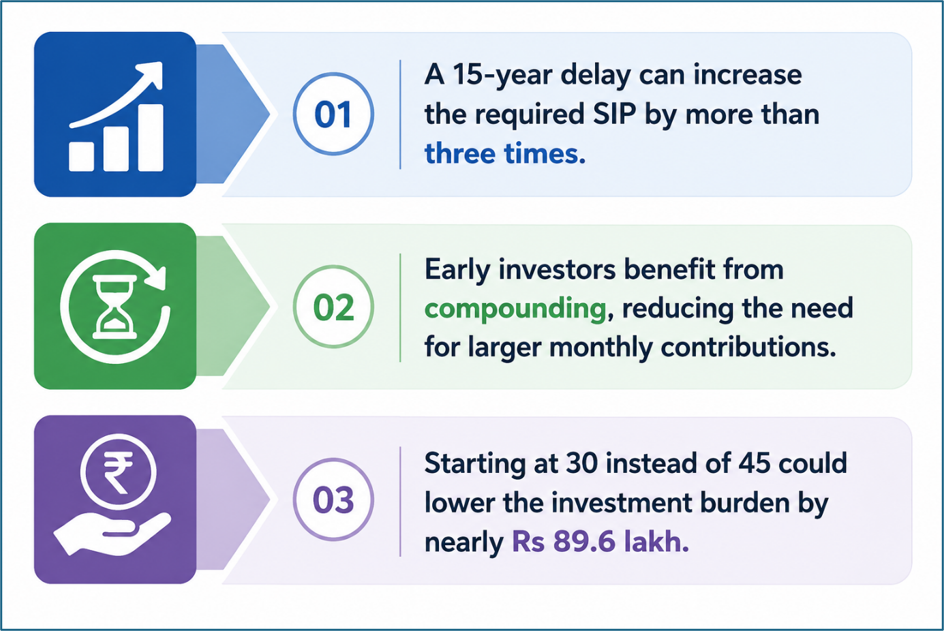

A simple illustration shows how delaying investments by 15 years can make wealth creation considerably more expensive, even when investment returns remain unchanged.

Source: Analysis by Kalkine

Why Time Matters More Than Investment Size

Compounding allows investment returns to generate additional returns over time. The longer money remains invested, the greater the potential impact of compounding.

Consider an investor aiming to build a corpus of Rs 5 crore by retirement at age 60. Assuming an annual return of 12%, the required SIP amount varies significantly depending on when the investment journey begins.

An investor who starts at age 30 has a 30-year investment horizon. However, an investor who waits until age 45 has only 15 years to reach the same target. The shorter time frame reduces the benefit of compounding and increases the burden on monthly contributions.

SIP Requirement: Age 30 Versus Age 45

For illustration purposes, assume both investors target a corpus of Rs 5 crore at age 60 and earn an average annual return of 12%.

The investor starting at age 30 may need to invest around Rs 20,000 per month. In contrast, the investor beginning at age 45 may need to invest approximately Rs 74,600 per month to achieve the same goal.

The difference in monthly investment works out to nearly Rs 54,600.

Over time, this gap can result in an additional investment burden of roughly Rs 89.6 lakh for the late starter.

Compounding Rewards Early Action

The advantage enjoyed by early investors comes primarily from the additional years available for compounding.

During the initial years, portfolio growth may appear modest. However, as returns accumulate and begin generating their own returns, the growth trajectory can accelerate.

This means investors who start early often contribute less capital overall while still achieving similar long-term outcomes.

In contrast, delayed investors may need to commit larger monthly sums, which can put pressure on household budgets and financial planning.

Small Delays Can Have Big Consequences

Many individuals postpone investing because of competing priorities such as home purchases, family expenses, education costs, or lifestyle spending.

While these commitments are important, delaying long-term investments can increase future savings requirements substantially.

Even a delay of a few years can affect the amount needed each month to achieve retirement or wealth-creation goals.

Starting with a smaller SIP and gradually increasing contributions may prove more manageable than waiting until a larger investment amount becomes necessary.

Factors That Influence SIP Outcomes

While the illustration assumes a fixed annual return and retirement age, actual outcomes can vary due to several factors.

Investment returns may fluctuate over time, inflation can affect purchasing power, and individual financial goals may change. Nevertheless, the underlying principle remains consistent: longer investment horizons generally provide greater flexibility and allow compounding to work more effectively.

Investors should periodically review their financial plans and adjust SIP contributions based on income growth, risk tolerance, and changing objectives.

Key Risks to Consider

- Market returns may differ from assumed long-term projections.

- Inflation can reduce the future purchasing power of accumulated corpus.

- Interruptions in SIP contributions may affect target achievement.

- Changes in financial goals can alter required investment amounts.

Summary

Building long-term wealth depends not only on investment returns but also on when investing begins. An investor targeting Rs 5 crore may need a much smaller monthly SIP when starting at age 30 compared with age 45. The additional years allow compounding to generate a larger portion of the final corpus, reducing the monthly contribution requirement and overall investment burden.

FAQs

Q: Why does starting an SIP early matter?

A: Early investing provides more time for compounding, potentially reducing monthly investment requirements for long-term goals.

Q: Can a late investor still build a large retirement corpus?

A: Yes, but achieving similar goals may require substantially higher monthly contributions and disciplined investing.

Q: What is the biggest advantage of a longer investment horizon?

A: A longer horizon allows investment returns to compound over time, helping wealth grow more efficiently.