Highlights

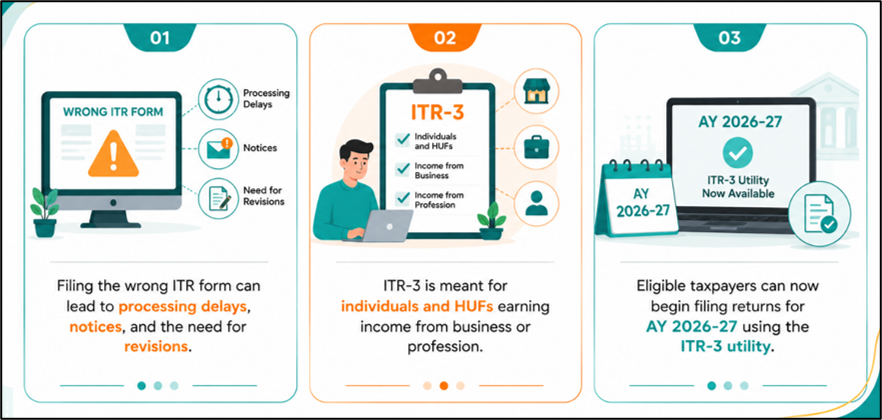

- The Income Tax Department has enabled ITR-3 filing for AY 2026-27.

- ITR-3 applies to individuals and HUFs with business or professional income.

- Non-audit taxpayers filing ITR-3 may have a deadline of August 31, 2026.

The Income Tax Department has made the ITR-3 utility available for Assessment Year (AY) 2026-27, allowing eligible taxpayers to begin preparing and filing their income tax returns. The form is designed for individuals and Hindu Undivided Families (HUFs) that earn income from business or profession and are not eligible to file simpler return forms such as ITR-1, ITR-2, or ITR-4.

The availability of the utility is an important development for professionals, business owners, traders, and other taxpayers with more complex income structures.

Source: Analysis by Kalkine

Who Is Eligible To File ITR-3?

ITR-3 is applicable to individuals and HUFs earning income under the head "Profits and Gains of Business or Profession." This includes taxpayers operating proprietary businesses and those engaged in professional activities.

The form may also be relevant for taxpayers with additional income streams alongside business or professional income, including capital gains, house property income, and other taxable receipts, provided they fall within the eligibility framework prescribed by the Income Tax Department.

Business Owners

Individuals running proprietary businesses generally use ITR-3 to disclose business income, expenses, profits, and tax liabilities.

Professionals

Doctors, lawyers, architects, consultants, chartered accountants, and other professionals earning income from their practice may be required to file ITR-3 depending on their tax status and income structure.

Share And Derivatives Traders

Individuals reporting income from trading activities, including futures and options transactions treated as business income, often file returns using ITR-3.

Important Filing Details

With the utility now available, eligible taxpayers can begin compiling financial information and preparing returns for FY 2025-26 corresponding to AY 2026-27. The utility supports return preparation through the Income Tax Department's filing system.

Taxpayers subject to audit requirements must ensure that audit reports are filed within the prescribed timelines before completing the return filing process.

For AY 2026-27, the due date for non-audit taxpayers filing ITR-3 is reported as August 31, 2026, while audit cases may have a later deadline. Taxpayers should verify applicable deadlines based on their category and compliance requirements.

Documents Taxpayers Should Keep Ready

Before filing ITR-3, taxpayers may consider gathering the following information: Business accounts, profit and loss statements, balance sheets, and relevant accounting records.

Tax Documents

TDS certificates, advance tax payment details, self-assessment tax records, and Form 26AS information.

Investment And Asset Details

Information relating to capital gains, investments, securities transactions, and other reportable assets where applicable.

Bank And Income Information

Bank account details, interest income records, rental income information, and other relevant income statements.

Accurate documentation can help reduce reporting errors and simplify the filing process.

Why Choosing The Correct ITR Form Matters

Selecting the appropriate return form is important because filing an incorrect form may lead to processing issues, notices, or the need to submit a revised return. Taxpayers should assess their income sources carefully before choosing an ITR category.

Individuals with business or professional income generally cannot use ITR-1 or ITR-2 and may need to file ITR-3 or another applicable form depending on their circumstances.

Key Risks To Consider

- Filing the wrong ITR form may trigger processing complications.

- Incomplete income disclosure can result in tax notices.

- Missing audit requirements may delay return processing.

- Incorrect financial data may require return revision later.

Summary

The Income Tax Department has enabled the ITR-3 utility for AY 2026-27, allowing eligible taxpayers to begin filing returns for FY 2025-26. The form is primarily meant for individuals and HUFs earning business or professional income, including proprietors, professionals, and certain traders. Taxpayers should review eligibility criteria carefully, maintain supporting documents, and ensure compliance with filing and audit requirements before submitting their returns.

FAQs

Q: Who should file ITR-3 for AY 2026-27?

A: Individuals and HUFs earning income from business or profession generally need to file ITR-3.

Q: Can salaried individuals file ITR-3?

A: Yes, if they also have eligible business or professional income requiring ITR-3 filing.

Q: Is ITR-3 available for AY 2026-27?

A: Yes. The Income Tax Department has enabled the ITR-3 utility for eligible taxpayers.