Highlights

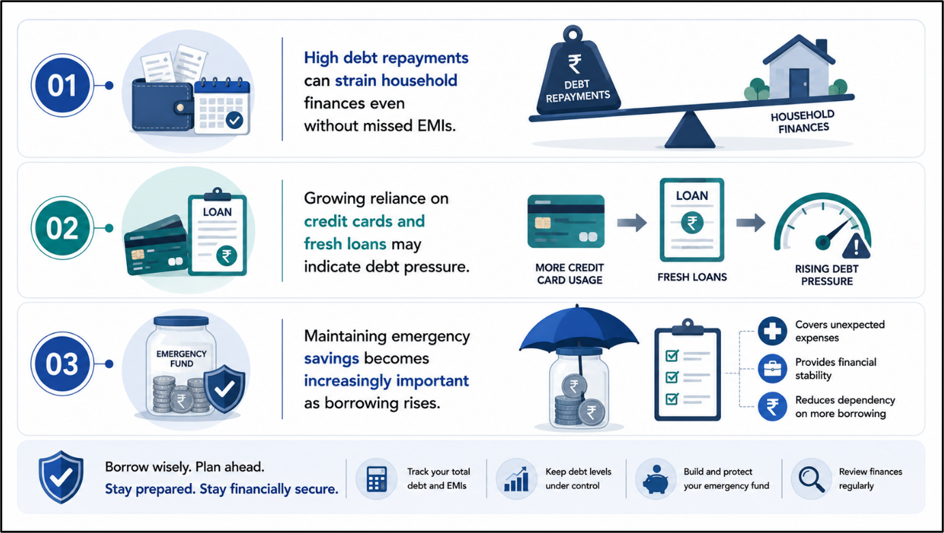

- Multiple EMIs can strain monthly finances if income growth does not keep pace.

- A rising debt burden may reduce flexibility to handle emergencies.

- Monitoring repayment ratios can help identify financial stress early.

Loans have become a common part of personal finance, helping individuals fund homes, vehicles, education and other major expenses. However, managing several Equated Monthly Instalments (EMIs) at the same time can gradually increase financial pressure.

While having multiple loans does not automatically indicate a problem, the situation can become concerning when debt obligations start consuming a large share of monthly income.

Recognising the warning signs early can help borrowers take corrective measures before financial stress escalates.

Source: Analysis by Kalkine

Understanding Your Debt Burden

One of the most important indicators of financial health is the proportion of income allocated toward debt repayment.

Financial planners often assess debt levels by comparing total monthly EMI obligations with monthly income. As this ratio rises, a borrower's ability to manage other expenses and savings goals may decline.

A high repayment burden can also make it difficult to absorb unexpected financial shocks.

A Simple Debt Assessment Formula

Borrowers can evaluate debt pressure using the debt-to-income concept.

Although the above formula illustrates long-term growth through compounding, the same principle highlights why debt obligations can grow costly over time if balances are not managed effectively.

When monthly repayments consume a significant portion of earnings, financial flexibility may begin to narrow.

Warning Signs That Debt May Be Getting Out of Hand

Several indicators may suggest that debt levels are becoming difficult to manage:

- Struggling to pay EMIs on time.

- Using new loans to repay existing debt.

- Frequently relying on credit cards for essential expenses.

- Reduced ability to save or invest.

- Dependence on emergency borrowing.

These signs may indicate that debt obligations are starting to exceed comfortable repayment capacity.

Impact on Financial Goals

Excessive debt can affect more than just monthly cash flow. It may also delay important financial objectives such as:

- Building an emergency fund.

- Saving for retirement.

- Funding children's education.

- Purchasing a home.

- Creating long-term investments.

When a large share of income is directed toward repayments, less money remains available for wealth creation and future planning.

Why Emergency Funds Matter

Individuals carrying multiple EMIs may face greater challenges during periods of income disruption. Job loss, medical emergencies or unexpected expenses can quickly create repayment difficulties if adequate savings are unavailable.

Maintaining an emergency fund can help borrowers continue meeting obligations without resorting to additional borrowing.

This financial cushion becomes increasingly important as debt commitments increase.

Steps to Regain Control

Borrowers concerned about rising debt may consider:

- Reviewing all outstanding loans.

- Prioritising high-cost debt repayment.

- Avoiding unnecessary new borrowing.

- Creating a structured monthly budget.

- Increasing emergency savings where possible.

Regular monitoring of debt obligations can help identify problems before they become severe.

Balancing Borrowing and Financial Stability

Credit can be a useful financial tool when used responsibly. The objective is not necessarily to avoid borrowing altogether but to ensure that repayment obligations remain manageable relative to income.

Maintaining a balance between debt repayment, savings and regular expenses can support long-term financial stability and reduce the risk of future financial strain.

Key Risks to Watch

- EMIs consuming a large share of monthly income.

- Dependence on new borrowing to repay existing loans.

- Reduced savings due to increasing debt obligations.

- Missed repayments affecting credit history.

Summary

Multiple EMIs do not automatically indicate financial trouble, but rising debt obligations can create pressure if they consume a significant portion of income. Warning signs such as missed payments, reliance on credit for routine expenses and declining savings may indicate growing financial stress. Regularly reviewing debt levels, maintaining emergency savings and avoiding unnecessary borrowing can help borrowers keep their finances on a sustainable path.

FAQs

Q: How can I know if my debt level is too high?

A: If loan repayments consume a large share of income and limit savings or essential spending, debt may be becoming excessive.

Q: Are multiple EMIs always a problem?

A: No. Multiple EMIs can be manageable if repayments remain affordable and do not affect financial stability.

Q: What is a common warning sign of debt stress?

A: Borrowing additional money to repay existing loans is often considered a sign of increasing financial pressure.