Highlights

- Tax benefits can increase the effective value of EPF returns.

- EPF combines disciplined retirement savings with annual compounding benefits.

- Post-tax returns may compare favourably with several traditional investments.

The Employees' Provident Fund (EPF) is often viewed as a retirement savings tool rather than a wealth-building investment. However, the scheme's combination of annual interest accrual, tax advantages, and mandatory savings contributions can make it a significant component of long-term financial planning for salaried individuals.

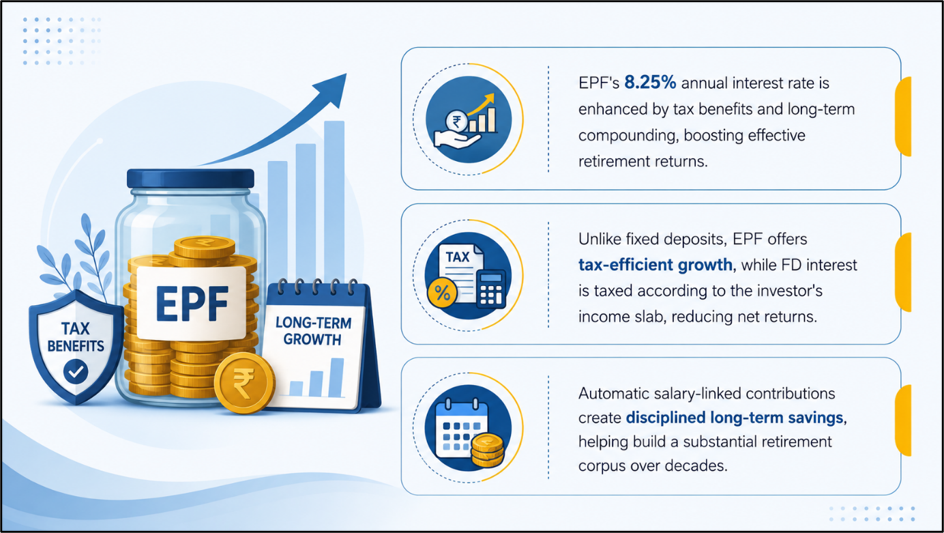

Although an annual interest rate of 8.25% may not appear exceptional when compared with certain market-linked investments, the overall benefits associated with EPF can change the return profile considerably. Understanding how taxation, compounding, and investment discipline interact helps explain why EPF remains relevant for retirement planning.

Source: Analysis by Kalkine

Source: Analysis by Kalkine

Looking Beyond the Headline Interest Rate

Many investors focus only on the declared EPF interest rate when evaluating returns. However, the actual value generated by the scheme depends on more than the annual percentage credited to the account.

EPF contributions are made regularly throughout an employee's working life, allowing savings to grow steadily over time. Since interest is credited on the accumulated balance, each year's earnings contribute to future growth. This creates a compounding effect that becomes increasingly meaningful over longer periods.

The result is that even a seemingly moderate annual return can lead to substantial corpus creation when contributions continue consistently over several decades.

Tax Efficiency Changes the Equation

One of the most important features of EPF is its tax treatment under applicable regulations.

Eligible contributions may qualify for tax deductions, while accumulated savings can continue growing without the annual tax burden commonly associated with many fixed-income investments. In addition, withdrawals that satisfy prescribed conditions may also receive favourable tax treatment.

Because taxation has a direct impact on net returns, investors should compare products on an after-tax basis rather than simply examining advertised rates. An investment generating taxable income may produce lower real gains than a tax-efficient alternative offering a similar nominal return.

Why Fixed Deposits May Deliver Lower Net Returns

Fixed deposits remain one of the most popular savings options for conservative investors. They provide predictable income and are relatively easy to understand.

However, FD interest is generally taxable according to the investor's income slab. For individuals in higher tax brackets, this can reduce the amount ultimately retained from the stated interest rate.

For example, two investments may offer similar headline returns, but the one with a lower tax burden could generate superior net outcomes over time. As years pass, the difference created by after-tax compounding may become increasingly noticeable.

This does not mean fixed deposits lack value. They continue to serve investors seeking liquidity, certainty, and shorter investment horizons. However, retirement-focused investors often evaluate them differently from EPF due to their tax treatment.

How EPF Compares with Mutual Funds

Comparisons between EPF and mutual funds are common, but the two products serve different purposes.

Equity mutual funds seek long-term capital appreciation through exposure to stock markets. Their returns can be substantially higher during favourable market conditions, but they can also experience periods of volatility and declines.

EPF follows a different path. The objective is retirement savings with relatively stable annual returns. Rather than pursuing aggressive growth, the scheme focuses on preserving and steadily expanding retirement wealth.

For investors seeking long-term growth, mutual funds may remain an important part of a diversified portfolio. However, EPF offers an element of predictability that market-linked investments cannot guarantee.

The Advantage of Automatic Saving

Another often-overlooked feature of EPF is its structured contribution mechanism.

Because contributions are deducted directly from salary, employees accumulate savings without needing to make repeated investment decisions. This reduces the likelihood of skipping investments during periods of market uncertainty or personal financial stress.

Over time, consistent investing can have a significant impact on wealth creation. The discipline built into EPF helps ensure that retirement savings continue growing throughout an employee's career.

Factors Investors Should Keep in Mind

While EPF offers several benefits, it should not be viewed as the sole solution for every financial goal.

Liquidity restrictions may limit access to funds before retirement, except under specified circumstances. Interest rates can also change based on future decisions by authorities. Additionally, inflation can influence the real purchasing power of accumulated savings over long periods.

Investors should therefore consider EPF as one component of a broader financial strategy that may include equity investments, debt products, and other savings instruments.

Key Risks

- Future EPF interest rates may differ from current levels.

- Inflation can reduce real purchasing power over time.

- Withdrawal restrictions may affect short-term liquidity needs.

- Overdependence on one retirement product may reduce diversification.

Summary

EPF offers more than its stated 8.25% annual return. Tax advantages, compounding benefits, and automatic salary-linked contributions can enhance long-term wealth creation. While fixed deposits and mutual funds serve different investment objectives, EPF's combination of stability and tax efficiency makes it an important retirement planning tool for salaried employees seeking disciplined long-term savings.

FAQs

Q: Why is EPF often considered more than just an 8.25% investment?

A: Tax advantages and long-term compounding can increase the overall value generated by EPF savings.

Q: Can EPF provide better post-tax outcomes than fixed deposits?

A: Depending on tax status and investment horizon, EPF may generate higher effective returns after taxes.

Q: Should EPF replace mutual funds in a portfolio?

A: No. EPF and mutual funds serve different objectives and can complement each other within a diversified strategy.