Highlights

- Credit utilisation can influence your credit profile even with timely repayments.

- Consistently high card usage may signal greater dependence on borrowed funds.

- Managing spending patterns is often more important than having a higher limit.

Many credit card users believe that maintaining timely repayments is enough to build a healthy credit profile. While payment discipline remains important, lenders often look beyond whether bills are paid on time.

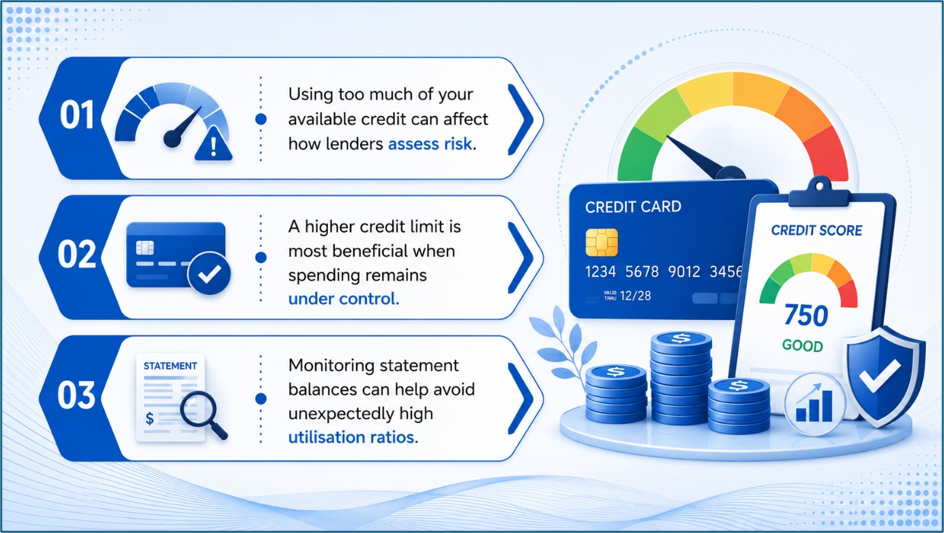

One factor that receives significant attention is how much of the available credit limit is being used. A person with a large credit limit may still weaken their credit profile if they consistently operate close to that limit. Conversely, an individual with a smaller limit may appear financially disciplined if spending remains well within available credit.

Source: Analysis by Kalkine

Understanding Credit Utilisation

Credit utilisation refers to the percentage of available credit being used at a given time.

For example, if a cardholder has a credit limit of Rs 1 lakh and an outstanding balance of Rs 25,000, the utilisation ratio is 25 percent. Financial institutions often view lower utilisation levels more favourably because they indicate that the borrower is not heavily dependent on credit for day-to-day expenses.

This means two individuals with identical incomes and repayment records may be assessed differently based on how much of their credit limit they regularly use.

Why Spending Behaviour Sends Important Signals

Lenders evaluate borrowing behaviour to understand financial habits and repayment capacity.

A customer who routinely uses a large proportion of available credit may appear more financially stretched than someone who uses only a small portion of their limit. High utilisation can indicate greater reliance on borrowed money, even when payments are made on schedule.

As a result, spending behaviour often becomes a more meaningful indicator than the size of the credit limit itself.

A Higher Limit Does Not Mean Higher Spending Capacity

Receiving a credit-limit increase is often viewed positively by cardholders. However, a larger limit should not automatically lead to increased spending.

Credit experts frequently note that higher limits can improve flexibility and reduce utilisation ratios when spending remains unchanged. Problems arise when individuals interpret the increased limit as permission to spend more. In such cases, debt levels can rise without any corresponding improvement in financial health.

The key benefit of a higher limit lies in maintaining lower utilisation rather than encouraging additional purchases.

The Statement Date Factor

Many cardholders focus only on the payment due date and overlook the statement generation date.

Credit card issuers typically report balances based on statement-cycle information. This means a person may pay the entire bill on time but still show high utilisation if the reported balance was large when the statement was generated.

Monitoring spending throughout the billing cycle can therefore be just as important as ensuring timely repayments.

Small Habits Can Create Long-Term Impact

Financial behaviour is often shaped by routine spending decisions.

Treating the credit limit as available income, making only minimum payments, or assuming future income will cover current expenses can gradually increase financial stress. These habits may contribute to rising debt levels and reduce financial flexibility over time.

In contrast, maintaining spending within budget, paying balances in full, and monitoring utilisation regularly can support healthier financial management.

Building a Better Credit Profile

Improving a credit profile is not always about increasing limits or opening additional accounts.

In many cases, better spending discipline can have a greater impact. Responsible card usage demonstrates financial control and may support future borrowing applications for products such as home loans, vehicle loans, or personal credit facilities.

The focus should remain on sustainable spending patterns rather than maximising available borrowing capacity.

Key Risks to Consider

- High utilisation may negatively affect borrowing assessments.

- Overspending can increase dependence on unsecured debt.

- Minimum payments may lead to higher interest costs.

- Rising balances can reduce financial flexibility.

Summary

Credit card limits often attract attention, but spending behaviour may have a greater influence on overall financial health. Regularly using a large portion of available credit can affect how lenders assess risk, even when payments are made on time. By focusing on responsible spending, monitoring utilisation, and avoiding unnecessary debt accumulation, individuals can strengthen their financial position and improve their long-term borrowing profile.

FAQs

Q: What is credit utilisation?

A: Credit utilisation measures the percentage of available credit currently being used by a cardholder.

Q: Does a higher credit limit automatically improve financial health?

A: No, financial health depends on spending discipline and repayment behaviour rather than the size of the limit.

Q: Why do lenders monitor spending habits?

A: Spending patterns help lenders assess borrowing behaviour, financial discipline, and potential repayment risk.