Highlights

- The spread component can influence the effective cost of a home loan.

- Changes in benchmark rates may not be the only factor affecting EMIs.

- Borrowers should review loan documents beyond the advertised interest rate.

When comparing home loans, most borrowers focus on the headline interest rate and monthly EMI. However, there is another number embedded in loan agreements that can significantly affect borrowing costs over time—the spread.

While benchmark-linked lending has improved transparency in home loan pricing, understanding the spread remains important for borrowers evaluating existing or new loans.

Source: Analysis by Kalkine

What Is the Spread in a Home Loan?

A home loan interest rate generally consists of two components:

- An external benchmark rate.

- A spread added by the lender.

The benchmark may be linked to rates such as the Reserve Bank of India's repo rate. The spread is an additional percentage determined by the lender based on factors including borrower profile, credit assessment and lending policies. The final interest rate charged to a borrower is typically the combination of these two components.

Why the Spread Matters

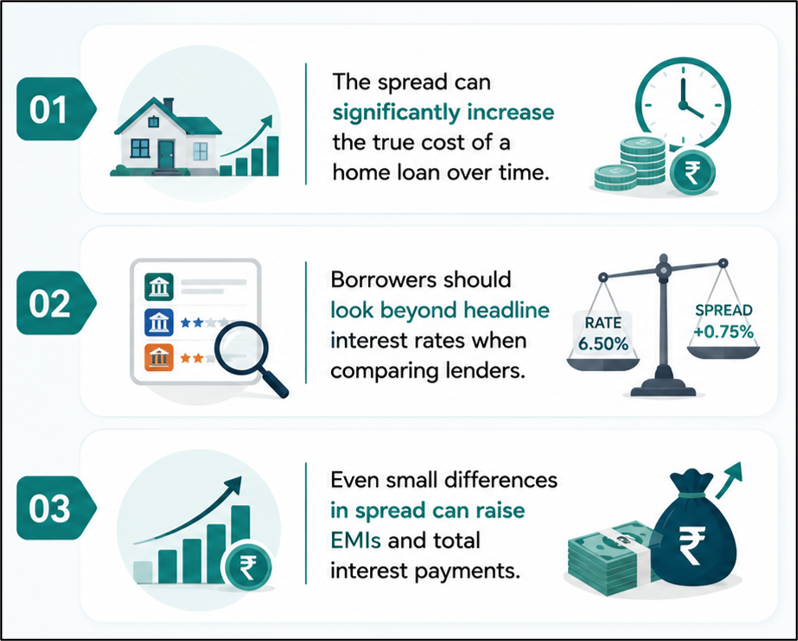

Many borrowers closely track movements in benchmark rates, expecting loan costs to fall whenever policy rates decline. However, the spread can also affect the final rate payable on a home loan.

Even when two borrowers receive loans linked to the same benchmark, differences in spread can result in different effective interest rates and EMIs. A relatively small variation in spread can influence total interest payments over the life of a long-term home loan.

Impact on Monthly EMIs

Home loans generally run for 15 to 30 years. Because of this long tenure, even minor differences in interest rates can affect monthly outgo and overall repayment obligations.

For example, a borrower paying a higher spread may face:

- Higher monthly EMIs.

- Greater total interest payments.

- Increased overall borrowing costs over the loan tenure.

As a result, understanding all pricing components becomes as important as comparing headline interest rates.

Factors That Influence the Spread

Lenders may determine spreads based on several considerations, including:

- Credit score and repayment history.

- Loan amount.

- Loan-to-value ratio.

- Employment profile.

- Internal lending policies.

Since lending institutions can use different assessment criteria, borrowers with similar incomes may still receive different loan pricing.

What Existing Borrowers Should Review

Existing home loan customers may benefit from reviewing their sanction letters and loan statements to understand:

- The benchmark linked to the loan.

- The spread applied by the lender.

- Whether the spread has remained unchanged.

- The effective interest rate currently being charged.

Understanding these details can help borrowers assess whether their loan pricing remains aligned with prevailing market conditions.

Questions to Ask Before Taking a Home Loan

Before finalising a home loan, borrowers may consider asking lenders:

- What benchmark is used for rate determination?

- What spread is being applied?

- Under what circumstances can the spread change?

- How frequently are interest rates reset?

- What would be the EMI impact of benchmark rate changes?

These questions can provide a clearer picture of future repayment obligations.

Why Transparency Matters

Benchmark-linked lending has increased transparency compared with earlier lending structures. However, borrowers still need to understand all components that contribute to the final interest rate.

A focus solely on the advertised lending rate may overlook factors that influence long-term borrowing costs. Reviewing both the benchmark and the spread can help borrowers make more informed financing decisions.

Key Risks to Watch

- Higher spreads can increase total loan repayment costs.

- Ignoring loan pricing details may lead to higher EMIs.

- Benchmark changes may not fully reflect in effective rates.

- Long loan tenures magnify small interest rate differences.

Summary

The spread is a lesser-known but important component of home loan pricing. Added to the benchmark rate, it helps determine the final interest rate and EMI paid by borrowers. Since even small differences can affect long-term borrowing costs, borrowers should review both benchmark rates and spreads when evaluating or managing a home loan. Understanding these details can provide a clearer picture of the true cost of borrowing.

FAQs

Q: What is the spread in a home loan?

A: The spread is the additional rate charged by a lender over the benchmark interest rate.

Q: Can two borrowers have different spreads?

A: Yes. Lenders may assign different spreads based on credit profile and lending criteria.

Q: Why is the spread important for EMIs?

A: A higher spread increases the effective interest rate, which can raise monthly EMIs and total repayment costs.