Highlights

- Holding period determines whether gains are taxed as short or long term.

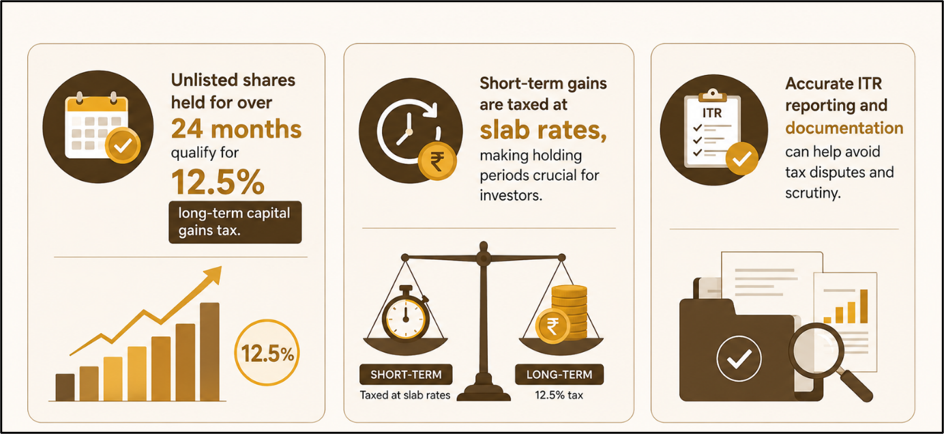

- Long-term gains on unlisted shares attract 12.5% tax after 24 months.

- Incorrect reporting of unlisted share transactions can trigger tax scrutiny.

Interest in unlisted shares has increased as investors seek opportunities in startups, private companies, and businesses that may eventually pursue public listings. While the potential for capital appreciation attracts investors, taxation remains an important factor that can influence actual returns.

Unlike listed shares traded on stock exchanges, unlisted shares are subject to a different tax framework. Understanding holding periods, applicable tax rates, reporting requirements, and common filing mistakes can help investors avoid compliance issues and unexpected tax liabilities.

Source: Analysis by Kalkine

What Are Unlisted Shares?

Unlisted shares represent ownership in companies that are not traded on recognised stock exchanges. These shares are generally held by promoters, early investors, employees through stock options, venture capital firms, private equity investors, and select shareholders.

Many investors acquire such shares in the hope of benefiting from future growth before a company reaches public markets. However, unlike listed securities, unlisted shares typically have lower liquidity and fewer trading avenues.

Understanding Capital Gains Classification

The tax treatment of unlisted shares depends largely on the holding period.

For taxation purposes, unlisted shares held for more than 24 months qualify as long-term capital assets. If sold within 24 months of acquisition, any profit is treated as a short-term capital gain.

This distinction is important because the applicable tax rates differ significantly between short-term and long-term transactions. Investors often mistakenly apply the holding period applicable to listed shares, which can result in incorrect tax calculations.

Tax on Short-Term Capital Gains

When unlisted shares are sold within 24 months, the resulting gains are classified as Short-Term Capital Gains (STCG).

Such gains are added to the investor's taxable income and taxed according to the applicable income tax slab rate. Therefore, the final tax liability depends on the individual's income bracket and overall taxable income for the financial year.

Tax on Long-Term Capital Gains

Profits arising from the sale of unlisted shares held for more than 24 months are treated as Long-Term Capital Gains (LTCG).

Under the current capital gains framework, LTCG on unlisted shares is taxed at 12.5% without indexation benefits. Unlike listed equity shares, unlisted shares do not receive a separate annual LTCG exemption threshold. Consequently, the entire taxable gain may be subject to the applicable long-term capital gains tax rate.

Reporting Requirements in Income Tax Returns

Investors must disclose gains from unlisted shares in the capital gains section of the applicable income tax return.

Depending on the nature of income, taxpayers generally report these transactions through ITR-2 or ITR-3. In addition, resident taxpayers holding unlisted equity shares are required to furnish details such as opening balance, acquisitions, transfers, and closing shareholding positions during the financial year.

Proper record-keeping becomes particularly important because tax authorities may compare disclosures with information available from corporate filings and other reporting systems.

Common Errors Investors Make

Tax professionals frequently identify several recurring mistakes in unlisted share reporting.

Some investors incorrectly classify gains using the 12-month holding period applicable to listed shares instead of the 24-month threshold applicable to unlisted shares. Others fail to disclose unlisted shareholdings altogether despite mandatory reporting requirements.

Errors in determining acquisition cost are also common, especially in transactions involving employee stock options, bonus shares, gifted shares, mergers, demergers, rights issues, and share swaps. Inadequate documentation can further complicate tax assessments.

Why Documentation Matters

Maintaining comprehensive records can help support tax filings and reduce the likelihood of disputes.

Investors should preserve transaction records, valuation reports, shareholder agreements, transfer documents, and other supporting evidence related to the acquisition and sale of unlisted shares.

Accurate documentation can become particularly important when authorities review the nature of a transaction or verify the computation of gains.

Key Risks

- Incorrect holding-period classification may lead to tax miscalculations.

- Failure to disclose holdings can attract regulatory scrutiny.

- Cost calculation errors may increase tax liabilities.

- Poor documentation can complicate assessments and disputes.

Summary

Unlisted shares offer investors exposure to private companies and potential pre-listing growth opportunities, but their tax treatment differs from listed equities. Gains are classified based on a 24-month holding period, with short-term gains taxed at slab rates and long-term gains taxed at 12.5% without indexation. Proper reporting, accurate cost calculations, and comprehensive documentation remain important for tax compliance and efficient return filing.

FAQs

Q: What qualifies an unlisted share as a long-term capital asset?

A: Unlisted shares become long-term capital assets when held for more than 24 months.

Q: How are short-term gains from unlisted shares taxed?

A: Short-term gains are added to income and taxed according to applicable slab rates.

Q: Are investors required to disclose unlisted shareholdings in ITR?

A: Yes, resident taxpayers generally must provide prescribed details of unlisted equity holdings.